Big River Steel updates galvanized coating extras

Big River Steel (BRS) made upward revisions to most of its galvanized coating extras this week, with new extras going into effect July 6.

Big River Steel (BRS) made upward revisions to most of its galvanized coating extras this week, with new extras going into effect July 6.

Tenaris is blaming unfairly traded OCTG imports flooding the US market for its decision to lay off approximately 170 employees.

Domestic raw steel production continued to ramp up through last week, now up to a six-week high according to the latest release by the American Iron and Steel Institute (AISI).

The CRU US Midwest hot-rolled (HR) coil index is a dominant and established price benchmark in the US. Many steel-buying contracts are linked to ‘the CRU,’ as it’s commonly called. But how does it work?

Drilling activity ticked up in the US but declined in Canada during the week ended May 17, according to the latest release from Baker Hughes.

American Heavy Plates is planning an expansion of its processing operations in Ohio.

The spread between hot-rolled coil (HRC) and prime scrap prices narrowed this month, according to SMU’s most recent pricing data.

Earlier this month, steelmakers entered the scrap market at mixed pricing. The prevailing price for obsolescent grades fell $20 per gross ton (gt). However, some notable districts decided to only drop $10/gt.

Mexican steelmaker Talleres y Aceros (TYASA) broke ground this month on the construction of a new special bar quality (SBQ) rolling mill in the state of Veracruz.

Domestic scrap prices this month are flat for prime material, but down for HMS and shredded, scrap sources told SMU.

The Biden administration announced a series of actions on Tuesday targeting China’s "unfair" trade policies. These actions will, among other things, make imports of steel and aluminum from the Asian nation even more prohibitive.

Steel prices were overall mixed this week, according to our latest check on the market. Sheet prices were flat to down, while plate prices inched up. SMU indices on hot rolled, cold rolled, and galvanized are now down to the lowest levels seen since November.

Wolfe Research Managing Director Timna Tanners cautioned clients about the darkening clouds of a brewing steel sheet storm in the company's Basic Materials Weekly Webcast on Monday. “This one we’ve been talking about for a while, and we feel like the theme is coalescing here,” she said.

Nucor chose to hold its consumer spot price (CSP) for hot-rolled (HR) coil steady this week after stunning the market last week with a significant price decline. The steelmaker said in a letter to customers on Monday morning that its $760-per-short-ton (st) CSP base price for HR coil is effective immediately. The price is unchanged from the CSP announced on May 6 but down $65/st from $825/st April 29.

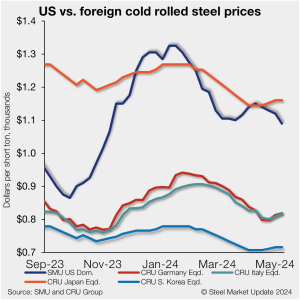

Offshore cold-rolled (CR) coil prices remain much less expensive than domestic product, even as domestic prices have slipped to a six-month low, according to SMU’s latest check of the market.

Triple-S Steel Holdings has acquired Houston-based plate distributor Griffin Trade Group.

Hot rolled, cold rolled, and plate buyers said mills are more willing to talk price on spot orders this week, while the overall negotiation rate for products SMU surveys remained level, according to our most recent survey data.

Most steel products tracked by SMU saw lead times contract this week from two weeks earlier, according to SMU’s most recent survey data.

After a considerable wait, the market for ferrous scrap for May shipment has started to form.

Sheet prices fell across the board this week – largely in response to Nucor’s $65-per-short-ton price cut for hot-rolled (HR) coil on Monday morning. SMU’s HR coil price is $780/st on average, a $35/st decrease week over week (w/w). Our average cold-rolled coil price is $1,090/st (down $30/st w/w). Our galvanized base price is $1,100/st […]

Turkish scrap import prices were stable last week. CRU’s assessment for HMS1/2 80:20 and shredded was unchanged at $384 per metric ton (mt) CFR and $408/mt, respectively.

March 2024 represents the third highest monthly steel import rate seen over the prior year.

Drilling activity declined in the US but increased in Canada, according to the latest data from Baker Hughes.

As we approach “buy week,” a term industry veterans use to refer to steel mill scrap buying time and an excuse to remain in the office, we have seen a variety of slants on the May market.

US steel mill shipments dropped in March on-year but were up from February, according to the most recent figures from the American Iron and Steel Institute (AISI).

Northwest Pipe’s profits more than doubled in the first quarter on-year, as the company expects a strong remainder of the year in both its steel pressure pipe and precast segments.

Ryerson swung to a loss in the first quarter of 2024, but the company’s chief executive sees less volatility in the sheet steel market.

Latest AA extrusion shipment report shows persistently weak demand The US Aluminum Association released its latest shipment report for extruded products. According to the report, shipments in March 2024 totaled 383.2 million pounds, representing a drop of 10.6% y/y but a rise of 4.5% m/m. For the YTD period through March, total shipments are now […]

Nucor Corp. announced that its plate mill group would cut prices for as-rolled, discrete, and normalized plate with the opening of its June order book. The Charlotte, N.C.-based steelmaker said in a letter to customers on Monday, April 29, that tags would be lowered by $90 per short ton (st). That would bring its base price to roughly $1,200/st.

The number of active rigs in the US is now at the lowest level seen in over two years, while Canadian rigs have fallen to a four-month low.