Algoma finalizes CA$500M loan from Canadian government

Algoma Steel plans to continue its transition to electric-arc furnace (EAF) steelmaking using the CA$500 million in loans from the Ontario provincial and Canadian federal governments.

Algoma Steel plans to continue its transition to electric-arc furnace (EAF) steelmaking using the CA$500 million in loans from the Ontario provincial and Canadian federal governments.

SMU’s Mill Order Index (MOI) surged in October after a notable decline the month prior. The recovery came as service center on order inventory totals picked up, supported by a slight uptick in shipments, according to our latest service center inventories data.

The US scrap market is showing some signs of strength in certain regions shortly after the November settlements finalized without detectable resistance.

US service centers’ flat-rolled steel supply edged lower for the third straight month, reaching 53.3 shipping days of supply on an adjusted basis at the end of October, according to SMU data.

A Tenaris subsidiary, Steel Recycling Services, has acquired the Beaver Falls, Pa., scrap processing yard of SA Recycling.

Nucor has increased its consumer spot price (CSP) for hot-rolled (HR) coil for a fourth consecutive week. Now at $910 per short ton (st), up $15/st from last week.

The latest Baker Hughes rig count report showed oil and gas drilling improved in the US this past week, while Canada saw its rig count decline.

US sheet market participants say demand for hot- and cold-rolled coils has not increased, leaving them confused by mill price increases and average lead times.

Steel mill lead times extended marginally this week on most sheet products but declined for plate, according to responses from SMU’s latest market survey.

Just over half of the steel buyers who responded to our market survey this week reported that domestic mills are willing to talk price on new spot orders. Mills have begun to hold a firmer stance on prices over our last two surveys.

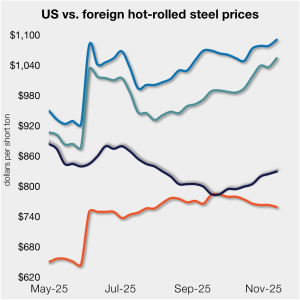

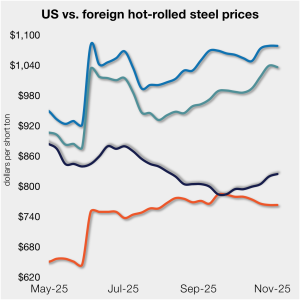

The price gap between stateside hot band and landed offshore product has marginally widened week over week.

The pig iron market is at a standstill since the last sale to the US several weeks ago.

NLMK USA is aiming to increase base prices on all products, effective immediately.

The price spread between HRC and prime scrap has widened for a second month, based on SMU’s most recent pricing data.

US-flagged shipments of iron ore on the Great Lakes are on the decline. Ore shipments in October were the lowest they’ve been for that month in five years.

SMU's sheet and plate steel prices moved higher in unison this week.

JSW Steel USA aims to increase steel plate prices by at least $40/short ton.

Nucor increased its weekly hot-rolled coil spot list price by $5 per short ton on Monday, Nov. 10.

The latest Baker Hughes rig count report showed oil and gas drilling improved in both the US and Canada in the first week of November.

SMU’s November ferrous scrap market survey results are now available on our website to all premium members. After logging in at steelmarketupdate.com, visit the pricing and analysis tab and look under the “survey results” section for “ferrous scrap survey” results. Past scrap survey results are also available under that selection. If you need help accessing the survey […]

Nippon Steel is making good on the big capex promises it made to secure its purchase of United States Steel Corp. This week, the Japanese company and American steelmaker together unveiled various capital investments they plan to make across U.S. Steel’s footprint.

The gap between US hot band prices and imports narrowed slightly. But with the 50% Section 232 tariffs, most imports remain more expensive than domestic material.

ArcelorMittal Dofasco and Stelco joined recent moves by US mills to push sheet prices higher.

Most sheet prices inched up again this week following mill efforts to set a floor under tags and to increase them from there.

SunCoke Energy’s earnings declined in the third quarter as weaker domestic coke sales and contract economics weighed on results.

U.S. Steel has announced a $75-million capital investment to install a new premium thread line at its Fairfield Tubular Operations in Alabama.

Zekelman Industries said Canadians who report the use of foreign steel in active or future public construction projects are eligible for a CAD$1,000.00 (USD$711.62) payment.

Nucor increases HR spot price by $5/ton

The pig iron market in Brazil saw some activity last week that could present some additional options to producers there, but at lower price levels.

With infrastructure demand shifting toward digital capacity, Nucor Corp. is positioning itself as the go-to steel supplier for the data center boom.