Asian HR theoretically cheaper than US HR - even with S232 at 50%

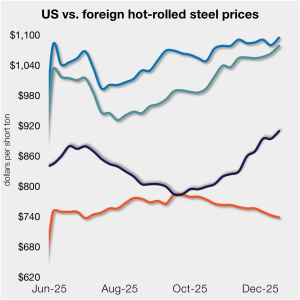

The price gap between stateside hot band and landed offshore product continues to narrow, inching closer toward parity. The premium is now, on average, at its lowest level since July.

The price gap between stateside hot band and landed offshore product continues to narrow, inching closer toward parity. The premium is now, on average, at its lowest level since July.

Worthington Steel executives emphasized on an earnings conference call on Thursday that the company’s standout fiscal Q2 performance came from capturing new automotive business, with direct automotive shipments rising 26% year over year.

Architecture firms across the United States continued to grapple with weak billings in November, amid uncertain economic conditions, according to the AIA.

Steel Dynamics Inc. expects its fourth-quarter earnings to be weaker than in the previous quarter, albeit still higher than last year. Longer-than-expected mill outages impacted flat-rolled steel volumes in the quarter.

Posco has confirmed a 20% stake in a joint EAF mill in Louisiana with fellow South Korean firm Hyundai, an investment valued at $582 million.

Nucor has guided to lower earnings sequentially in the fourth quarter but higher on-year.

Apparent steel supply rose to 8.64 million short tons in September, driven primarily by higher domestic mill shipments despite a sharp drop in finished imports.

In this Premium analysis we examine North American oil and natural gas prices, drill rig activity, and crude oil stock levels through December

Following last week’s pause, SMU’s price indices were overall steady to higher this week, holding at or near multi-month highs.

The European Commission is aiming to have Section 232 tariffs eased on steel and aluminum, with a special eye towards derivative products as well, as it negotiates with the Trump administration, according to a report in Politico on Dec. 15.

Two bids remain for Italy’s shuttered ILVA steelworks, with one belonging to a company headed by steel veteran Alan Kestenbaum, according to a report in Bloomberg.

Martin Baker is joining Hybar as its strategic metallics manager, responsible for further developing the metallics procurement and global strategic initiatives for the Osceola, Ark.-based steelmaker.

US shipments of heating and cooling equipment fell 11% in October from September to the lowest monthly rate of the year, and an eight-year low, according to AHRI.

SMU and AMU are pleased to announce that Wells Fargo Managing Director Timna Tanners will be joining us for a Community Chat webinar on Wednesday, Dec. 17, at 11 am ET.

Following August’s modest 4% uptick, the volume of steel shipped outside of the country slipped 8% in September to 594,000 short tons, according to recently released data from the US Department of Commerce.

SSAB has tapped Tom Cox to lead its Americas division. Currently GM of SSAB Iowa, he'll assume the position of Head of SSAB Americas as of Feb. 1, 2026.

The volume of raw steel produced by US mills ticked higher last week, according to the latest figures published by the American Iron and Steel Institute (AISI).

Business activity in New York state retreated in December, according to the Empire State Manufacturing Survey conducted by the Federal Reserve Bank of New York.

US Congressmen Mike Kelly (R-Pa.) and Chris Deluzio (D-Pa.) have introduced the Strengthening Trade Enforcement and Evasion Limitations Act (STEEL Act) into the House of Representatives. The bipartisan bill aims to curb unfairly traded imports and strengthen US trade enforcement.

Flat rolled = 50.6 shipping days of supply Plate = 52.8 shipping days of supply Flat rolled US service centers’ flat-rolled steel supply declined for the fourth straight month, reaching 50.6 shipping days of supply on an adjusted basis at the end of November, according to SMU data. Flat roll supply is at its lowest […]

Nucor increased its weekly hot-rolled coil spot list price by $10 per short ton (st) again on Monday, Dec. 15. This was its eighth increase in as many weeks, moving up $65/st over that span.

According to recently finalized US Commerce Department data, US steel imports tumbled to a near five-year low in September

US plate market participants hope the new year will bring favorable market conditions. But they remain leery of making big purchases because of lingering uncertainty.

The latest SMU’s Steel Buyers’ Sentiment Indices showed mixed results.

The US rig count edged down this week while the Canadian count inched up, according to the latest Baker Hughes data released on Friday, Dec. 12.

Steel mill lead times held relatively steady this week on both sheet and plate products, according to responses from SMU’s latest market survey.

Participants in the domestic coil market hope producer price increases indicate strong market conditions entering the new year.

Less than half of the steel buyers who responded to our market survey this week reported that domestic mills are willing to talk price on new spot orders

Plans are in the works to save 500 steelworker jobs at Algoma Steel and to construct two new mills – a plate mill and a beam mill, according to various local media reports.

Members of Mexico’s lower house have approved a plan to impose levies of between 5% and 50% on imports of 1,463 categories of goods from countries lacking a trade agreement with Mexico.