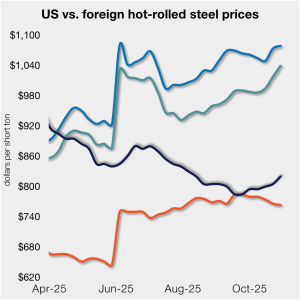

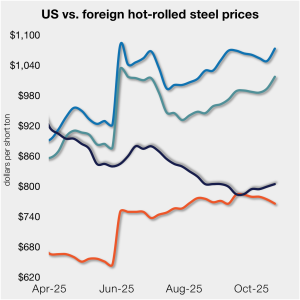

Price gap between US HRC, most imports narrows slightly

In dollar-per-ton terms, US product is on average $141/st less than landed import prices (inclusive of the 50% tariff). That’s down from $148/st last week.

In dollar-per-ton terms, US product is on average $141/st less than landed import prices (inclusive of the 50% tariff). That’s down from $148/st last week.

Participants in the domestic steel plate market said the plate market never accepted mill-issued spot price increases.

Angelo “Ange” Borzillo has passed away at the age of 92. He leaves behind a legacy that will endure as long as the steel he helped develop: Galvalume sheet steel.

Cliffs said it successfully completed a defect-free trial production of exposed steel parts using aluminum-forming equipment in collaboration with an unnamed OEM,

SMU’s hot-rolled coil price increased for a third consecutive week. And the gains were more pronounced this time following a price hike initiated on Friday by NLMK USA.

Sheet steel indices increased across the board this week, while plate prices held steady. All five of SMU’s price indices are higher than they were two weeks ago, and all but one are above levels recorded four weeks ago.

NEMO Industries CEO talks cost and reasoning behind a $3-billion pig iron project in Louisiana.

Domestic sheet market participants say recent spot price hikes from NLMK USA and Nucor will do little to shake-up stagnant market conditions. Price increases in the current market On Friday Oct. 24, NLMK customers learned that the producer’s hot- and cold-rolled prices increased $50 per short ton (st) and its coated products were $100/st higher. […]

Nucor has raised its weekly spot list price on hot-rolled coil by $10 per short ton (st) after keeping it unchanged since Aug. 25.

Atlas Tube, in a leading move, said it aims to increase prices for mechanical tubing, hollow structural sections (HSS), and piling products by at least $50 per short ton (st).

SMU digs into the vault to look back at an old survey, and to tell what exciting things are still to come.

US buyers want to drop pig iron prices to levels commensurate with the decline in prime scrap in their domestic market. Prime price shed $20 per gross ton (gt) in September and another $20/gt in October.

NLMK USA plans to increase prices for hot-rolled and cold-rolled coil by at least $50 per short ton (st). The move is effective immediately for all spot orders, the steelmaker said in a letter to customers on Friday.

The steelmaker released updated extras to customers on Oct. 15, marking the second adjustment in just six weeks following their early September revision

Below are some other issues that should be on your radar. Because while prices have been steady, a lot is going on when it comes to news that could impact them.

What's on steel buyers' minds this week? We asked about market prices, demand, inventories, tariffs, imports, and other evolving market trends. Read on for buyers' comments in their own words...

Demand for plate on the spot market remains soft by comparison to years past. However, this week regional demand variations grew more pronounced.

SMU’s average price for domestic HR coil moved $5 higher this week, while price movements in offshore markets varied. This dynamic...

Want to know the latest on Trump, tariffs, and trade policy - and the impact on both steel and aluminum? Then join SMU, AMU, and leading law firm Wiley for a Community Chat on Thursday, Nov. 13, at 11 am ET.

It's can-kicking at its finest. And it’s been drawn out! Some are getting so good at it, they’re kicking cans and taking names.

Our average HR coil price increased $5/short ton from last week, marking a second consecutive week of modest gains. Market participants generally attributed the increase to...

Domestic mill production rebounded last week, according to the latest production figures released by the American Iron and Steel Institute (AISI). Production had been historically strong over the summer months before softening in early October.

Medium- and heavy-duty trucks (MHDV) and buses imported to the US will start being charged Section 232 tariffs beginning Nov. 1.

Nucor kept its consumer spot price (CSP) for hot-rolled coil at $875 per short ton (st) for the ninth straight week.

We just wrapped up another Steel 101 workshop, easily the most hands-on industry workshop on steelmaking and market fundamentals.

After marginally rising in August and September, the premium galvanized coil carries over hot-rolled coil (HRC) coil has narrowed again in recent weeks. As of Sept. 16, the spread between these two products has shrunk to a two-and-a-half-year low of $125 per short ton (st).

Genuine demand, they stated, will return when the market feels stable again.

FabArc Steel Supply announced this week the completion of two large-scale projects in Georgia and Mississippi.

US domestic sheet prices have remained rangebound in recent weeks as supply tightness met weak demand. Demand for steel produced in the US increased among some Mexican industrial buyers....

SMU’s latest steel buyers market survey results are now available on our website to all premium members.