SMU Survey: Modest improvement in Sentiment Indices

Both SMU Sentiment Indices continue to show that buyers remain optimistic for their company’s chances of success, though far less confident than they felt earlier in the year.

Both SMU Sentiment Indices continue to show that buyers remain optimistic for their company’s chances of success, though far less confident than they felt earlier in the year.

SMU’s Aug. 8, 2025, steel buyers market survey results are now available on our website to all premium members.

The volume of steel shipped outside of the country in June fell 3% from the prior month to 618,000 short tons (st), according to recently released data from the US Department of Commerce.

What the word "sideways" means can depend on where you sit on the procurement spectrum.

Following January’s pre-tariff surge, imports have remained low since February compared to post-pandemic volumes

Hot rolled spot market participants reported another week of moderate demand and ample supply, with no strong signs that conditions will change next week.

SMU’s Monthly Review provides a summary of our key steel market metrics for the previous month, with the latest data updated through July 31.

Mill production times for sheet products are holding just above multi-year lows, while plate lead times remain elevated.

Most steel buyers continue to report that mills are open to negotiating spot prices. Negotiation rates have remained high for most of the past three months.

Veteran trade attorney Lewis Leibowitz will join SMU for a Community Chat on Wednesday, Aug. 13, at 11 am ET.

Current and future scrap sentiment indices declined this month, according to SMU’s latest ferrous scrap survey data.

SMU’s August ferrous scrap market survey results are now available on our website to all premium members.

Sheet and plate prices were either flat or modestly lower this week on softer demand and increasing domestic capacity.

US plate market participants are not fazed by the constricted nature of the current spot market pricing environment. Right now, they said, mill’s choosing to hold prices from one month to the next makes sense because service centers remain amply supplied and demand is stable. Modest upticks or slips in prices are aligned with most of the participants' expectations right now.

Steel Market Update is proud to celebrate its 17th birthday this month.

Domestic mill output remains historically strong, holding near multi-year highs since early June.

Nucor Plate Group has informed customers that August spot prices will remain flat.

Nucor’s weekly consumer spot price (CSP) for hot-rolled (HR) coil was adjusted $10 per short ton (st) lower this week after holding steady last week.

We’re in the dog days of summer, and the question is whether the market will improve as lead times stretch into September. Your answer to that question might depend on where you are in the supply chain. And producers, it seems to me, are a lot more optimistic than consumers at the moment.

Prices for four of the seven steelmaking raw materials we track were unchanged from late June through the end of July, while two increased and one declined. Collectively, these material prices rose 1% month over month (m/m), but are down 3% compared to three months ago.

US manufacturing activity slowed again in July to a 10-month low

Several EU member states have published a ‘non-paper’ that puts forward proposals for a post-safeguard trade measure.

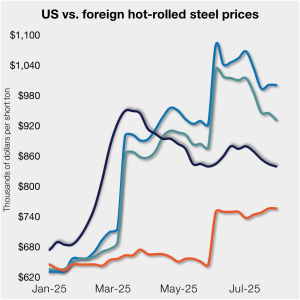

Hot-rolled (HR) coil prices in the US edged lower again this week, while offshore price were little changed. Stateside prices continue to trail imports from Europe, supported by Section 232 steel tariffs.

We're less than a month out from Steel Summit 2025. Have you already signed up?

Earlier this week, SMU polled steel buyers on an array of topics, ranging from market prices, demand, and inventories to tariffs, imports, and evolving market events.

Seasonal steel slowdowns combined with ongoing anxieties about tariffs and mill strategies have dampened sentiment for several hot-rolled steel market participants this week. Buyers are jittery, market stands still The operator of a Midwest-based service center said that steel buyers are scared. “Everyone is afraid to buy steel right now. Unless you’re on a […]

The Steel Demand Index now stands at 42, up from 38.5 in early July, but off from a four-year high of 65.0 in late February.

A scrap trader looks back fondly at blast furnace steelmaking.

Sheet prices slipped again this week amid discounting from certain mills and ongoing concerns about demand.

The Brazilian pig iron community is playing defense ahead of the Aug. 1 deadline for a 50% US tariff on imports from the South American country. The moves indicate the Brazilian producers do expect the tariff to go into effect.