HVAC equipment shipments increase in January

Following December’s 11-month low, total heating and cooling equipment shipments rebounded 8% in January, according to the Air-Conditioning, Heating, and Refrigeration Institute.

Following December’s 11-month low, total heating and cooling equipment shipments rebounded 8% in January, according to the Air-Conditioning, Heating, and Refrigeration Institute.

While overall steel demand remains weak in the near term, there are reasons to expect metallurgical coal prices will increase over the course of the year, Ramaco says.

President Trump’s tariffs are aimed in large part at bringing manufacturing back to the United States. In theory, it’s simple enough: Want to avoid a big tariff? Make it in the US!

“The next months are going to be good ones for pig iron producers," according to one source.

The volume of finished steel entering the US market in January climbed to the highest level recorded in two and a half years.

What are steel buyers saying this week about prices, demand, the import market, the evolving tariff situation, and more?

With the tariff craziness showing no signs of abating, we take you on a tour of the current situation.

After over a month of increases, steel prices paused this week for some of the products tracked by SMU. Three of our price indices continued to climb, while two held steady from the prior week.

“CBP expects full compliance from the trade community for accurate reporting and payment of the additional duties. CBP will take enforcement action on non-compliance," the agency said in a March 7 bulletin.

US steel exports recovered to a five-month high in January after having fallen to a two-year low in December. This growth follows four consecutive months of declining exports.

Raw steel mill output rebounded last week after falling to one of the lowest levels of the year, according to the American Iron and Steel Institute (AISI). Production is now at the second-highest weekly rate recorded so far in 2025.

Nucor has increased its weekly HR coil spot price for seven consecutive weeks.

One thing we've learned from our survey here at SMU: When prices are rising, people have a lot to say. You can be assured that with our most recent survey, the comments were coming in fast and furious.

Steel imports ended 2024 on a low note, with November trade falling to a one-year low and December seeing a modest 3% recovery. Then as the new year began, import volumes spiked.

US rig counts remain slightly above multi-year lows, while Canadian activity is experiencing a seasonal decline from a recent seven-year high.

SMU’s Buyers’ Sentiment Indices both declined this week but remain strong. This indicates buyers are still optimistic about their companies' ability for success.

Before we get whipsawed by the current moment, it’s important to reflect on optimism. Whatever happens, consumers are going to need steel.

Buyers responding to our latest market survey reported longer lead times this week on all of the sheet and plate products SMU tracks.

The majority of the steel buyers responding to our latest market survey reported that domestic mills are not open to negotiating prices on new orders this week.

On 4 March, new 25% blanket tariffs across all products exported to the USA from Canada and Mexico are now in effect. The only exception is Canadian energy products, which will be assessed a 10% tariff.

Remember infrastructure week in Trump 1.0? It became a running joke. Because it was almost always derailed by whatever the scandal of the day was. In Trump 2.0, we've got tariff week. And unlike infrastructure week, tariff week is no joke.

Steel prices climbed across the board this week, with every steel product tracked by SMU rising to multi-month highs.

Construction spending edged down slightly in January, slipping for the first time in four months. The US Census Bureau estimated spending at a seasonally adjusted annual rate of $2,196 billion in January, down 0.2% from December’s downward revised rate. The January figure is 3.3% higher than a year ago. January’s result, despite the slight erosion, […]

Steel Manufacturers Association (SMA) President Philip K. Bell stressed a mood of "cautious optimism" for steel on what turned out to be Tariff Eve.

SMU’s Monthly Review provides a summary of key SMU steel market metrics for the previous month, with the latest data updated through February 28th.

Raw steel mill production declined last week to one of the lowest levels seen this year, according to recent figures released by the American Iron and Steel Institute (AISI).

Nucor has increased its list price for hot-rolled (HR) coil to $900 per short ton (st), according to a letter to customers on Monday. The Charlotte, N.C.-based steelmaker’s list price for HR is up $40/st from $860/st last week and up $125/st from $775/st a month ago, according to SMU’s mill price announcement calendar. The […]

US plate prices have moved up at a sharp clip over the past three weeks. The gains come on the heels of a unified mill pricing blitz, bolstered by the threat of looming tariffs and the expectation of sharply higher scrap prices. Prices hit their lowest level in more than four years in late January, […]

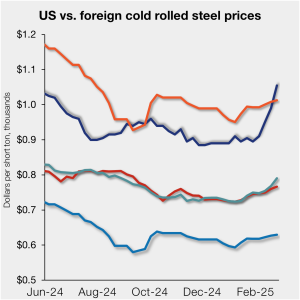

The price spread between stateside-produced CR and imports reached its widest margin in over a year.

That’s not to say Section 232 shouldn’t be tightened up. Or that certain trade practices – even among our traditional allies – weren’t problematic. But when it comes to the reboot of Section 232, I do wonder whether there will be some unintended consequences.