NLMK USA raising HR, CR $50/ton, coated at $150 above HR base

NLMK USA is aiming to increase base prices on all products, effective immediately.

NLMK USA is aiming to increase base prices on all products, effective immediately.

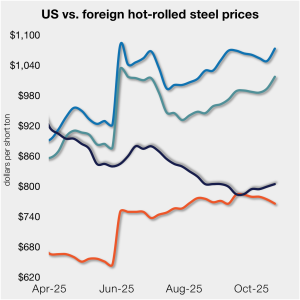

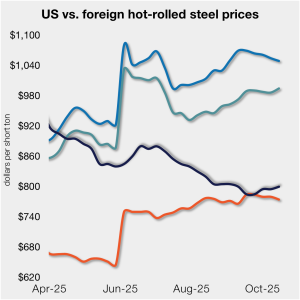

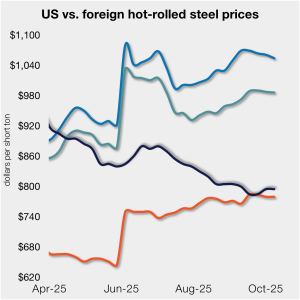

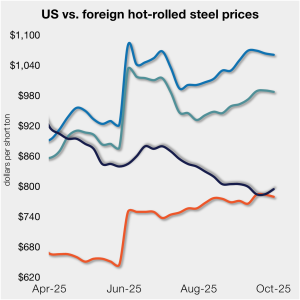

The price spread between HRC and prime scrap has widened for a second month, based on SMU’s most recent pricing data.

Nucor increased its weekly hot-rolled coil spot list price by $5 per short ton on Monday, Nov. 10.

Most sheet prices inched up again this week following mill efforts to set a floor under tags and to increase them from there.

Nucor increases HR spot price by $5/ton

Most steel buyers think that steel prices will continue to rise into the 2026. But they don’t see the kinds of big gains that have characterized past market upturns, according to the results of SMU’s latest steel market survey.

SMU’s hot-rolled coil price increased for a third consecutive week. And the gains were more pronounced this time following a price hike initiated on Friday by NLMK USA.

Sheet steel indices increased across the board this week, while plate prices held steady. All five of SMU’s price indices are higher than they were two weeks ago, and all but one are above levels recorded four weeks ago.

NLMK USA plans to increase prices for hot-rolled and cold-rolled coil by at least $50 per short ton (st). The move is effective immediately for all spot orders, the steelmaker said in a letter to customers on Friday.

SMU’s average price for domestic HR coil moved $5 higher this week, while price movements in offshore markets varied. This dynamic...

Our average HR coil price increased $5/short ton from last week, marking a second consecutive week of modest gains. Market participants generally attributed the increase to...

Steel Dynamics Inc.’s third-quarter profits jumped year over year as the company saw “record” quarterly steel shipments

Nucor kept its consumer spot price (CSP) for hot-rolled coil at $875 per short ton (st) for the ninth straight week.

After marginally rising in August and September, the premium galvanized coil carries over hot-rolled coil (HRC) coil has narrowed again in recent weeks. As of Sept. 16, the spread between these two products has shrunk to a two-and-a-half-year low of $125 per short ton (st).

Genuine demand, they stated, will return when the market feels stable again.

US domestic sheet prices have remained rangebound in recent weeks as supply tightness met weak demand. Demand for steel produced in the US increased among some Mexican industrial buyers....

SMU’s average price for domestic hot-rolled (HR) coil was $800 per short ton (st) this week, up $5/st week on week (w/w). In offshore markets last week, prices were varied.

US scrap prices fell on busheling and shredded in October, while HMS remained flat, market sources told SMU.

Mills are more willing to negotiate spot prices for both sheet and plate products, according to our latest market survey results.

Nucor has left its consumer spot price for hot-rolled coil at $875 per short ton for the eighth straight week.

SMU’s average price for domestic hot-rolled (HR) coil was $795 per short ton (st) this week, sideways week on week (w/w). The move was different in offshore markets last week, as prices eased marginally.

The US hot-rolled coil (HRC) market feels steadier as the 4th quarter begins - not strong, but no longer slipping either.

Tariffs are ultimately to blame for stagnant demand in the hot-rolled coil market, domestic market sources tell SMU.

The American Iron and Steel Institute reported a decline in the monthly shipments of US mills from July to August.

Participants in the hot-rolled sheet market expressed frustration with the continuing lack of demand this week.

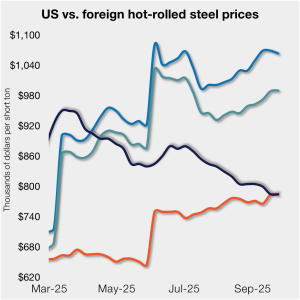

The price gap between stateside hot band and landed offshore product narrowed this week. Still, with the 50% Section 232 tariff, most imports remain much more expensive than domestic material.

Sheet and plate lead times saw minor shifts this week, according to SMU’s latest market survey. Sheet times have inched up over the last month but remain within days of multi-year lows, as they have since May. Plate lead times have bobbed within a tight range for months, hovering roughly a week longer than this time last year.

Steel buyers say mills remain slightly more willing to negotiate spot prices for sheet and plate products than in mid-September, according to our latest market survey.

Nucor is keeping hot-rolled (HR) coil prices unchanged again this week, according to its latest consumer spot price (CSP) notice issued on Monday, Sept. 29.

SMU’s average price for domestic hot-rolled (HR) coil held at $785 per short ton (st) this week, unchanged week on week (w/w). A similar dynamic was seen in offshore markets last week as well.