Nucor lowers HRC list price to $890/ton

Nucor’s weekly consumer spot price (CSP) for hot-rolled (HR) coil was adjusted $10 per short ton (st) lower this week after holding steady last week.

Nucor’s weekly consumer spot price (CSP) for hot-rolled (HR) coil was adjusted $10 per short ton (st) lower this week after holding steady last week.

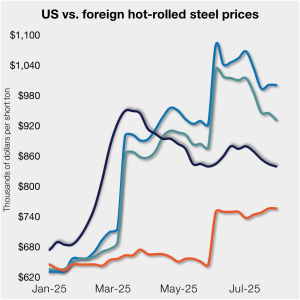

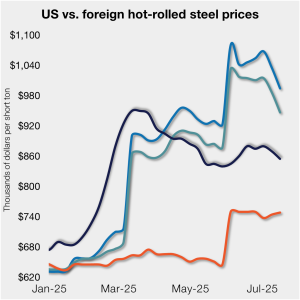

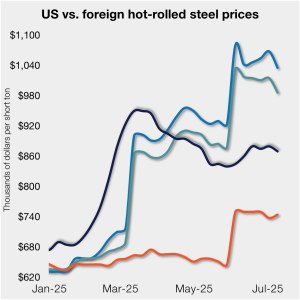

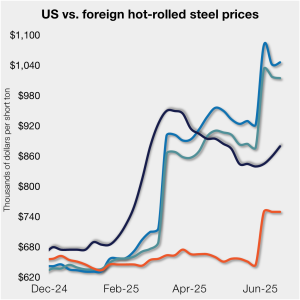

Hot-rolled (HR) coil prices in the US edged lower again this week, while offshore price were little changed. Stateside prices continue to trail imports from Europe, supported by Section 232 steel tariffs.

Sheet prices slipped again this week amid discounting from certain mills and ongoing concerns about demand.

Steel mill lead times on sheet products contracted across the board this week compared to early July, while plate production times moderately extended, according to steel buyers responding to this week’s market survey.

After a period of backwardation driven by headlines and CRU index anchoring, the CME HRC curve structure has undergone a notable shift.

Steel prices continued to decline this week across all of the sheet and plate products tracked by SMU, pressured by short lead times and the typical summer slowdown.

Nucor is lowering its list price for spot hot-rolled coil for the first time since May 27.

Stateside prices continue to trail imports from Europe, supported by Section 232 steel tariffs that were doubled in early June.

US sheet and plate prices were flat or lower as reduced import volumes were offset by so-so demand.

Nucor is holding its list price for spot hot-rolled coil at $910 per short ton (st), unchanged since June 30.

The price spread between prime scrap and hot-rolled coil widened marginally again in July.

Mill lead times for sheet products were steady to slightly longer this week compared to our late June market check, while plate lead times contracted, according to steel buyers responding to this week’s market survey.

Hot-rolled (HR) coil prices in the US ticked down this week but have fluctuated little over the past month. Stateside tags continue to trail imports from Europe, supported by Section 232 steel tariffs that were doubled in early June.

Domestic mills are more open to talk price on new orders than they were in June, according to most steel buyers responding to our market survey this week. Negotiation rates have recovered from the early-June lull and are now just a few percentage points shy of the high levels seen late last year.

Sheet and plate prices slipped this week on so-so demand, sideways scrap prices, and chatter that certain mills were making unsolicited calls looking for tons.

Nucor is keeping its list price for spot hot-rolled coil unchanged after last week’s shortened holiday week.

I’m not sure how many different ways I can write that it’s been a quiet market ahead of Independence Day. There are variations on that theme. I’ve heard everything from the ominous “eerily quiet” to "getting better" and even the occasional “blissfully unaware” (because I’m enjoying my vacation).

We can interpret that managed money still has expectations of price strength while physical participants are running closer to a balance on a net basis.

Steel sheet buyers report feeling bogged down by the ongoing stresses of stagnant demand, news fatigue, tariff negotiations or implementation timelines, and persistent macroeconomic uncertainty.

Cliffs has idled facilities in Riverdale, Ill., and Conshohocken and Steelton, Pa.

Nucor has raised its weekly spot price on hot-rolled coil by $10 per short ton after holding it steady last week.

Following the uptick seen two weeks ago, lead times eased this week for all four sheet products tracked by SMU, while plate lead times held steady, according to this week’s market survey.

Steel market participants contend that buyers will remain in “wait-and-see" mode until some market stability is restored.

The majority of steel buyers responding to our latest market survey say domestic mills are more willing to talk price on sheet and plate products than they were earlier this month. Sheet negotiation rates rebounded across the board compared to early June, while our plate negotiation rate hit a full 100%.

As of June 24, the premium galvanized coil carries over hot-rolled coil is just $5 per short ton (st) above the lowest level recorded in almost two years.

Prices for steel sheet slipped this week despite Section 232 tariffs remaining at 50% and a US strike on nuclear facilities in Iran over the weekend.

Nucor maintained its weekly list price for hot-rolled (HR) coil this week, following two consecutive increases.

Not many people in the North American steel market had direct US involvement in another Middle East conflict on their bingo card. Prices weren't expected to shoot higher unless something unexpected happened. That unexpected something has now happened. And there is talk of oil at $100 per barrel. What does that mean for steel?

Several steel market sources say they were blindsided when mills increased spot prices for hot-rolled coils this week.

US hot-rolled coil prices crept up again this week but still trail imports from Europe.