SMU's Week in Review: June 9-13

More developments with USS-Nippon. A look at whether imports will be needed. The latest prices. And more.

More developments with USS-Nippon. A look at whether imports will be needed. The latest prices. And more.

The US steel industry is edging closer to independence from imports, and it may only take one more mill to tip the scales, according to Timna Tanners, managing director at Wolfe Research.

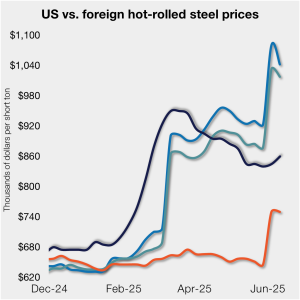

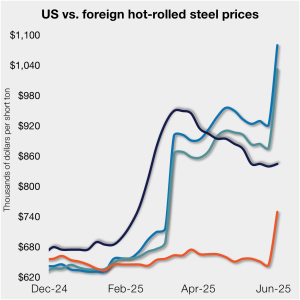

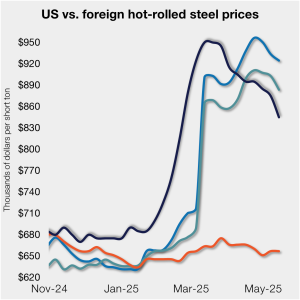

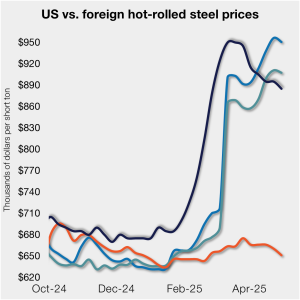

Domestic hot-rolled (HR) coil prices edged up marginally again this week, while offshore prices ticked down.

ArcelorMittal’s (AM) Hamilton location to be shuttered, wire production shifting to Montreal.

The amount of finished steel that entered the US market in April declined 3% from March but remained at elevated levels, according to SMU’s analysis of Department of Commerce and American Iron and Steel Institute (AISI) data.

Subdued demand is causing importers to cancel hot-rolled (HR) coil orders and renegotiate the terms of shipments currently enroute to the US, importers say. An executive for a large overseas mill said customers might find it difficult to justify making imports buys after US President Donald Trump doubled the 25% Section 232 tariff on imported steel […]

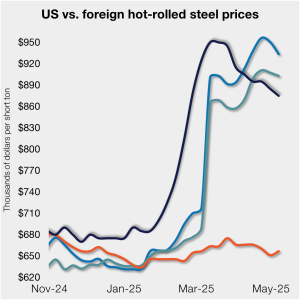

Domestic hot-rolled coil prices edged up marginally this week, while offshore prices ticked down.

Timna Tanners, managing director of equity research for Wolfe Research, will be the featured speaker on the next SMU Community Chat. The webinar will be on Wednesday, June 11, at 11 am ET. It’s free to attend.

April now represents the third-lowest monthly import rate witnessed in nearly two and a half years, with several steel products falling to multi-year lows

On Monday and Tuesday, SMU polled steel buyers for their thoughts on the current market. We received an array of feedback, including prices, demand, inventories, imports, and evolving market events.

Section 232 tariffs of 50% on imported steel will go into effect on Wednesday with few exceptions, according to a top White House official.

Briefing on the stay motion will be completed by June 9. If a stay pending appeal is granted, it will likely remain in effect until the Court of Appeals issues a decision, which could be months in the future. The case is almost certain to be appealed to the Supreme Court.

Timna Tanners, managing director of equity research for Wolfe Research, will be the featured speaker on the next SMU Community Chat. Timna has coined Sheet Storm, Galv Galore, and Rebarmageddon. Her forecasts and insights are always though provoking. And she’s not afraid to speak her mind. So it's no surprise that she's one of our most popular guests!

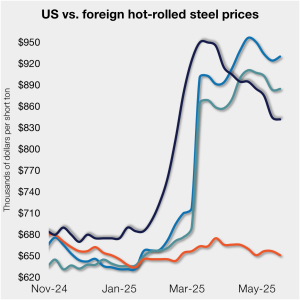

Domestic hot-rolled coil prices moved lower again, maintaining the downward move seen in eight of the last 10 weeks.

Coated sheet imports from Vietnam face steeper anti-dumping duties after Commerce recalculated the rates due to ministerial errors.

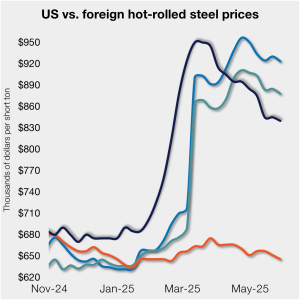

Domestic hot-rolled (HR) coil prices were flat this week after declining seven of the last nine weeks. Offshore prices have also eroded in recent weeks, though not nearly as significantly as in the US.

One cause of this was increased competitiveness from imports that have put pressure on some domestic producers.

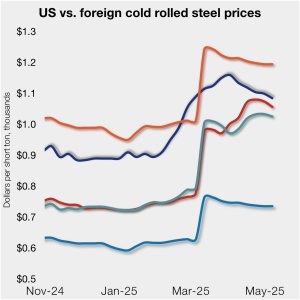

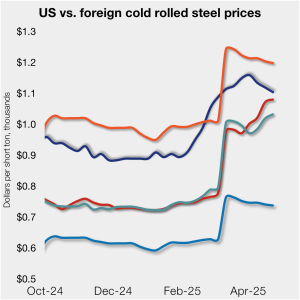

US cold-rolled (CR) coil prices were down again this week, slipping six weeks in a row and seeing the sharpest drop-off since last July.

Domestic hot-rolled (HR) coil prices fell this week, now down seven of the last eight weeks.

The volume of finished steel entering the US market rebounded in March, according to our analysis of US Department of Commerce and American Iron and Steel Institute (AISI) data.

The UK deal may signal relaxation of the heaviest tariffs. The suspension of the reciprocal tariffs greater than 10% - remember, 57 countries were hit with that - ends on July 9. But it could be extended. If more deals like the one with the UK are struck, the suspensions may continue to permit more agreements - relieving global markets of considerable worry.

US cold-rolled (CR) coil prices moved lower again this week, slipping five weeks in a row now. Most offshore markets mirrored the move, ticking down as well.

Cliffs came tantalizing close to buying U.S. Steel in 2023. There were rumors in 2024 that Cliffs might buy NLMK USA before it ultimately purchased Stelco for $2.5 billion in November of last year. Who would have thought that asset sales would have been the focal point of discussion just six months later?

US steel imports rebounded from February to March, rising to the second-highest monthly rate witnessed in the past ten months, according to final data recently released by the US Commerce Department. April license data shows that gain has likely been erased, with trade falling to the lowest rate of the year and several product categories hitting multi-year lows.

Domestic hot-rolled (HR) coil prices moved lower this week, now down six of the last seven weeks. Recent price erosion has been seen in offshore markets, keeping the price gap between imports and domestic products largely flat week on week (w/w).

SMU polled steel buyers on an array of topics earlier this week, including market prices and demand, tariffs and reshoring, inventories and imports, and evolving market trends.

US cold-rolled (CR) coil prices edged lower again this week, slipping four weeks in a row now. Most offshore markets mirrored the move, ticking down marginally as well.

Section 232 returned on March 12, and since then, the price gap between offshore and US hot band has tightened.

United Airlines raised eyebrows earlier this month when it provided two forecasts for 2025 – one assuming a relatively stable economy and another assuming a recession. The reason? Uncertainty around the impact of President Trump’s policy shocks on the broader economy. And it sometimes feels like we’re seeing a battle between those two narratives (stable vs recession) play out within in the pages of this newsletter.

US cold-rolled (CR) coil prices declined again this week, slipping for a third straight week. Most offshore markets did the opposite, moving higher this week.