Miller on scrap: What’s next for February?

The state of the US scrap market is not very well understood, according to the dealer trade. It seems steelmakers in several regions are still looking to buy scrap, several sources told SMU.

The state of the US scrap market is not very well understood, according to the dealer trade. It seems steelmakers in several regions are still looking to buy scrap, several sources told SMU.

The Tampa Steel Conference is just a few days away. Here are some topics I’m looking forward to learning more about during the proceedings on Monday and Tuesday. For starters, we’ll have about a month of 2024 under our belt when we convene on Sunday. How does that compare to what we thought the start of the year would look like? And what’s the outlook for the balance of the year?

The 35th Annual Tampa Steel Conference starts in just a few days. As one of the premier domestic steel conferences, it’s the perfect way to kick off 2024. It’s not too late to register if you haven’t already done so, but make sure to book now!

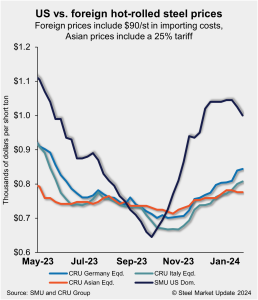

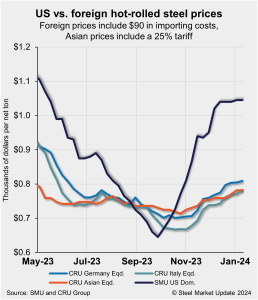

US hot-rolled coil (HRC) prices declined further this week, easing to their lowest level since late November. And while domestic tags remain notably more expensive than offshore product, the premium has declined as imported hot band tags have moved higher.

This earnings season will hit a little different. U.S. Steel has announced that it won’t be hosting an earnings call. While this silence is normal during an acquisition process, it does alter a staple of the earnings landscape.

America is increasing a society run by regulations. Businesses and individuals deal with a host of agencies that control transportation, the environment, labor regulation, securities, competition and, of course, international trade; the list goes on and on. We are also a litigious society, dependent on neutral tribunals to resolve disputes. Who decides who is right […]

CRU forecasts that global demand for steelmaking raw materials will fall month over month (m/m) between mid-January and mid-February. The major downward pressure on raw materials demand will come from China, where steel end-use demand will fall toward the Chinese New Year (CNY) holiday (Feb. 10–17).

When I started in the scrap business many years ago as a rookie trader in Luria’s Cleveland office, I saw an industry composed of family-owned businesses stretching across a great industrial nation.

Much discussion has centered on HRC futures and option liquidity. The perceived lack of liquidity is often used as a reason for not engaging in risk management, a profound folly in our opinion. Looking back over the last decade, the futures market has seen increased volume. The HRC futures volume in 2023 was 617% of 2013 numbers.

US hot-rolled coil (HRC) prices edged down this week while import prices moved higher on average. Domestic hot bands’ premium over cheaper imports declined as a result. But overall, US product remains substantially more expensive than overseas material. All told, US HRC prices are 21.4% more expensive than imports, a premium that is down three […]

There seems to be a growing consensus that the US sheet market has peaked at a high level and could begin losing ground from here. Whether declines happen quickly or whether sheet prices bop around at current levels for a few weeks more is the primary question.

After three months of provocations, the US and Britain retaliated against Houthi rebels in Yemen, bombing several sites in North Yemen that assisted in Houthi attacks on international shipping in the Gulf of Aden and the Red Sea. The Houthi rebels are widely seen as Iranian proxies, launching attacks to provoke the West into attacking Yemen, leading to more attacks on shipping.

The LME three-month price was moving down again on the morning of Jan. 12 and was last seen trading at $2,215 per metric ton (mt). We expect a test of the $2,200/mt support to be imminent. A break would be bearish as it could mean a complete reversal of the gains seen in December, although we still estimate that as being unlikely.

For two consecutive months, the initial scrap prices didn’t attract the amount of scrap that mills needed. A Detroit area mill came in at $460 per gross ton (gt) for busheling, which was down $50 from last month and down $20 on shredded and plate and structurals (P&S). But I guess they did not know at the time another mill in the district bought scrap sideways. Needless to say, that order filled right away. SMU could not find any supplier who sold at down $50.

The Global Steel Climate Council (GSCC) was formed to advance the steel industry's climate strategy. And its intentions are clear: establish standards and advocate for carbon emission reductions by industry members.

It’s been a sloppy start to the year for domestic hot-rolled (HR) coil and ferrous scrap markets. One of the loudest things to happen in HR this year might be something that didn’t happen at all. Namely, Nucor didn’t follow competitor Cleveland-Cliffs higher when Cliffs announced a price hike to start the year.

After a holiday period that saw HR futures volumes somewhat muted in December, the first week of January brought with it increased interest reflected in higher volumes.

Pig iron prices rose month over month (MoM) in all major regions aside from Europe on improved buying. Demand in the US remains robust while market participants report that availability of Brazilian material increased after tightening a month prior. Meanwhile, Ukrainian export capacity increased due to greater access to temporary sea corridors.

US hot-rolled coil (HRC) prices were unchanged this week but remain significantly more expensive than offshore product. While imported hot band tags increased vs. last week, gains were marginal, keeping domestic HRC substantially more expensive than imports. All told, US HRC prices are 24.3% more expensive than imports, a premium that is down only slightly […]

TimkenSteel said on Wednesday it is changing its company name to “Metallus Inc.”

I expected that we’d start off January with prime scrap prices modestly up if for no other reason than industrial activity typically slows down over the holidays. And mills’ appetite for scrap typically increases in anticipation of stronger Q1 order activity.

Domestic steel mill shipments increased in November vs. a year earlier, but fell month over month.

The US Department of Commerce will likely be lowering the antidumping duty (AD) rates on imports of welded steel pipe from the UAE.

Nippon Steel believes it can successfully complete its planned buy of U.S. Steel, according to a report in Reuters.

All good things, including but not limited to the Holiday Season, must come to an end. The corporate independence of U.S. Steel Corporation looks like it’s coming to an end also, despite objections from some politicians and the United Steelworkers union.

The Department of Commerce issued its final determination in the trade case involving tin mill products from a handful of countries.

The new year represents an opportunity to capitalize on America’s leadership position in free market principles, steel industry modernization, and global efforts to create a lower carbon future for the steel industry. Steel Manufacturing Association (SMA) members are poised to lead the way.

The International Trade Commission (ITC) held a hearing on Thursday, Jan. 4, to consider arguments for and against the imposition of antidumping and countervailing duties (AD/CVDs) on tin mill products from a handful of countries. Both sides made compelling arguments.

The LME aluminum 3-month price was moving further down on the morning of Jan. 5 and was last seen trading at $2,287 per metric ton (mt) as of this article’s writing, already down 6% from its recent peak. SHFE cash also concluded the first week of the year on a weaker foot. The cash contract […]

After a brief decline in the price of scrap for the Turkish market, which peaked in December at approximately $424 per metric ton (mt) for HMS 80/20, the market has bottomed at $405/mt on cargoes from Europe.