Prices

January 18, 2024

HRC futures: Navigating HRC market depth

Written by Logan Davis

Much discussion has centered on HRC futures and option liquidity. The perceived lack of liquidity is often used as a reason for not engaging in risk management, a profound folly in our opinion.

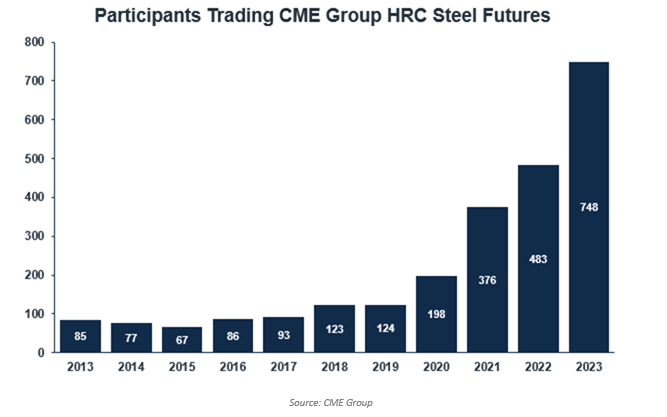

In its early years, the CME HRC futures market faced challenges in establishing liquidity and attracting participants. However, as industries increasingly recognized the importance of managing price risk, trading volumes began to rise. The exchange implemented measures to enhance market structure, such as introducing standardized contracts and improving clearing processes.

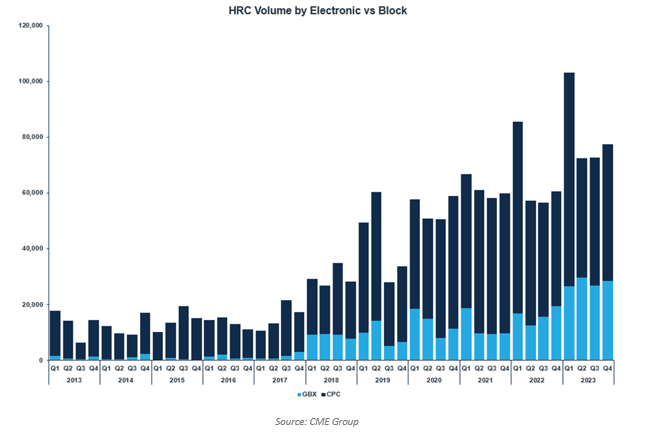

Looking back over the last decade, the futures market has seen increased volume. The HRC futures volume in 2023 was 617% of 2013 numbers:

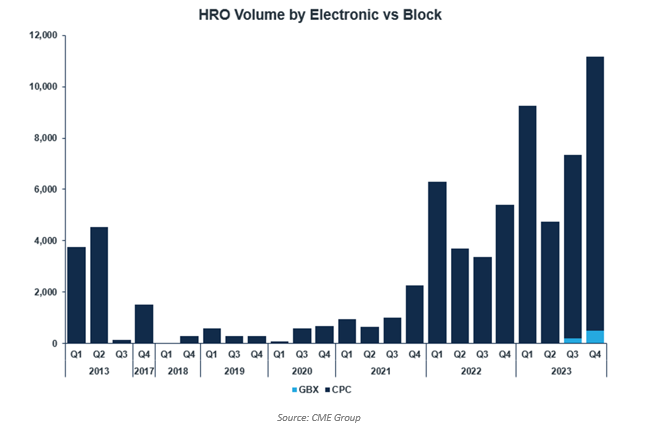

The options market has seen similar growth (283% of 2013 average), albeit delayed versus the futures timeline:

Liquidity is a fundamental concept in financial markets, representing the ease with which assets can be bought or sold without significantly impacting their prices. It is a critical factor that influences the efficiency, stability, and overall functioning of financial markets. There are reasons why liquidity is important to both futures and options markets. Understanding this nuance in the HRC market is essential to effectively using the tools available. It is also necessary to increase the pool of market participants and the aggregate liquidity in the HRC exchange markets.

Speculators require opportunity to put their money to work. That means demand for their services. The more industry participants that express a need for hedging tools like futures and options, the more speculators are incentivized to participate and provide liquidity to those industry participants.

Liquidity’s impact on slippage, bid-ask spreads, and strategy selection

Liquidity influences various aspects of trading, particularly in options markets. Liquid markets contribute to the reduction of slippage, or the difference between the expected price and executed price of a trade. This is crucial for accurate hedging, as the option hedge must closely track the movement in the underlying futures.

The narrower bid-ask spread of options contracts is another advantage of a liquid market. This characteristic is especially noteworthy when selecting options strikes. The narrower spreads contribute to better pricing, making it more cost-effective for traders to execute their trades. In markets with deeper liquidity, traders can expect clearer expectations for the cost of a strategy. This clarity empowers traders to select tools that best align with their stated objectives and goals. Conversely, in low liquidity environments, traders may face higher costs to ensure execution, potentially leading them to choose less desirable strategies solely to secure coverage. This scenario, characterized by higher costs, can create dissatisfaction among traders who would have preferred a different strategy. In essence, the combination of reduced slippage, narrower bid-ask spreads, and a deeper options pool provides traders with the tools and transparency needed to make informed and optimal choices when executing their strategies in the options market.

Liquidity’s influence on options strikes and market depth

Liquidity in options markets has a profound impact on both market depth and the availability of specific strike prices. Deeper markets provide traders with the flexibility to execute larger transactions without significantly impacting prices and ensuring smoother trading experiences. Secondly, in contrast to illiquid options markets, where certain strike prices may be limited or entirely absent in terms of trading activity, liquid markets offer a broader range of available strikes. Traders often prefer liquid strikes as they provide the assurance of easy entry or exit without facing challenges related to low trading volumes. A market with shallow depth may compel traders to resort to using round number strikes.

For instance, in a less liquid environment, traders may face constraints such as having to use $1,000 call options instead of a more precise number like $1,025. This lack of flexibility can hinder a trader’s ability to craft a strategy that perfectly aligns with their risk management objectives. The combination of execution efficiency and diversification options provided by liquidity ensures that traders have the tools and flexibility needed to optimize their hedging strategies in response to varying market conditions.

Liquidity’s Role in Risk Management and Dynamic Adjustments

In liquid markets, traders benefit from the ease of entering and adjusting hedge positions in response to changing market conditions. Traders can respond promptly to evolving market dynamics, ensuring that risk is managed efficiently. In illiquid markets, these adjustments can be more difficult. Utilizing open orders and proactively managing positions can avoid problems that accompany a lower liquidity options market.

Moreover, market depth becomes a valuable asset in actively managing option strategies, particularly in markets experiencing significant price swings, exemplified by the HRC market. For instance, in a market with big swings like HRC, traders can capitalize on the premium raising function of sold options before expiration. They have the flexibility to adjust protection or remove liabilities associated with sold options, taking advantage of market fluctuations. This strategic maneuvering enables traders to optimize their positions and, if needed, resell options to capitalize on the market’s oscillations.

In summary, with each cycle we have seen more industry participants transact in both HRC futures and options. While we’ve laid out several nuances related to the current conditions of the market, adoption is underway. Utilizing the HRC futures and options market as a risk management tool is viable today and conditions will continue to improve. That said, advantages will be had for those that choose to participate earlier, gaining familiarity with the risk management tools available to them.

Disclaimer

Options pricing above based on theoretical values. There is a risk of loss in futures trading. Past performance is not indicative of future results. © 2024 Commodity & Ingredient Hedging, LLC. All rights reserved.

About CIH:

CIH is a technology-enabled risk management firm that provides education and customized price risk management services to businesses impacted by volatility in commodities markets. The firm provides a structured, process-driven methodology to help clients filter through the noise, digest what’s pertinent, and evaluate appropriate strategies. A personalized relationship with a CIH consultant provides consistent guidance designed to provide a focused and disciplined approach based on client objectives. We provide structure and education to implement a hedging plan that helps clients achieve their goals in managing profitability in the long term.