Final thoughts

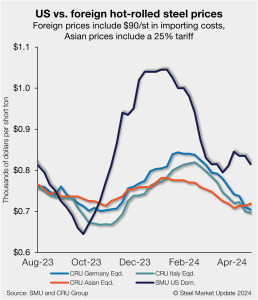

What a difference a month makes. In late March, it seemed like the US hot-rolled (HR) coil market was poised to cycle upward. Large buyers had re-entered the market and placed big orders earlier in the month. Several outages were underway or upcoming. And expectations were that lead times would continue to extend. Cliffs said […]