Market Data

March 28, 2024

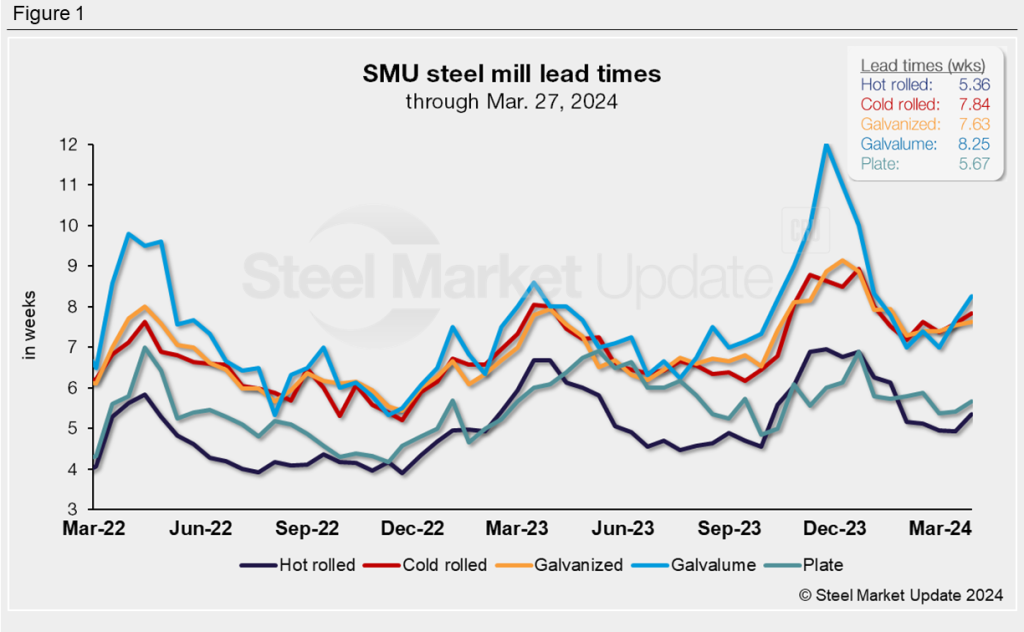

SMU survey: Steel mill lead times begin to extend

Written by Laura Miller

After stabilizing in our last check of the market, production times for flat-rolled steel have begun to push out further, according to steel buyers responding to SMU’s market survey this week.

The changes from our March 13 market check differed by product, but all moved higher. Average lead times extended by 9% for hot rolled (HR), 8% for Galvalume, 5% for plate, 3% for cold rolled (CR), and 1% for galvanized sheet. This week’s gains have pushed production times out the furthest since January, and expectations are for lead times to continue extending in the coming weeks.

Lead times by product

Hot-rolled coil: 4.93 weeks

In our latest market check, steel buyers reported HR lead times ranging from three to nine weeks. After flattening out in our March 13 market check at 4.93 weeks, lead times for HR extended by 0.43 weeks to an average of 5.36 weeks as of March 27. This is the longest average HR lead time since late January.

HR price: $780-840/st

Cold-rolled coil: 7.84 weeks

Steel buyers reported CR lead times between six and 12 weeks. The average production time is now 7.84 weeks, an extension of 0.26 weeks from the market check two weeks earlier. This week’s average is the longest CR lead time since the 8.00-week production time recorded at the start of the year.

CR price: $1,050-1,180/st

Galvanized coil: 7.63 weeks

Lead times for galvanized sheet were reported by buyers this week to be between six and 11 weeks. The average of 7.63 weeks was just slightly longer than the 7.55-week average production time seen two weeks ago. Galvanized lead times have been edging out further since hitting a recent low of 7.29 weeks during the week of Feb. 1.

Galvanized price: $1,070-1,170/st

Galvalume coil: 8.25 weeks

Buyers reported Galvalume lead times between six and 12 weeks, with this week’s average jumping by 0.58 weeks from two weeks ago to 8.25 weeks. This is the first time lead times for Galvalume have risen above the eight-week mark since early January.

Galvalume price: $1,120-1,180/st

Plate: 5.67 weeks

Buyers reported lead times for plate ranging from four to seven weeks, with the average of 5.67 weeks – extending by 0.25 weeks from two weeks prior. Plate lead times have been inching out from the recent low of 5.38 weeks at the end of February.

Plate price: $1,220-1,300/st

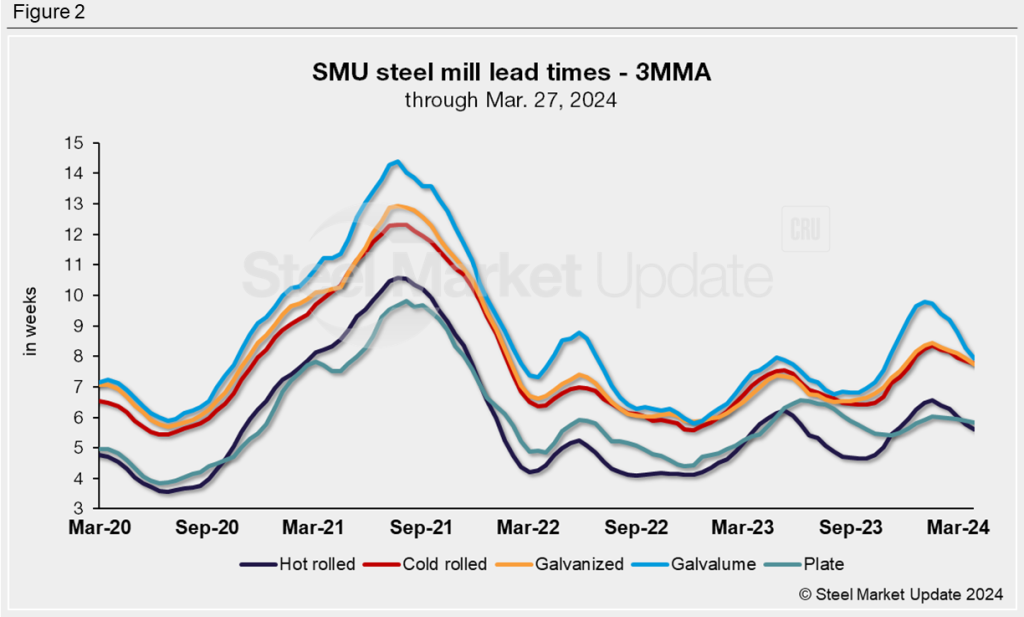

3MMA lead times

Looking at the three-month moving averages (3MMA) of lead times can smooth out the volatility seen in our biweekly readings. On a 3MMA basis, lead times for all products fell back once again, a trend they’ve been following for at least six weeks now.

From the March 13 market check, the 3MMAs fell back slightly, to 5.60 weeks for hot rolled, 7.76 weeks for cold rolled, 7.75 weeks for galvanized, 7.93 weeks for Galvalume, and 5.82 weeks for plate.

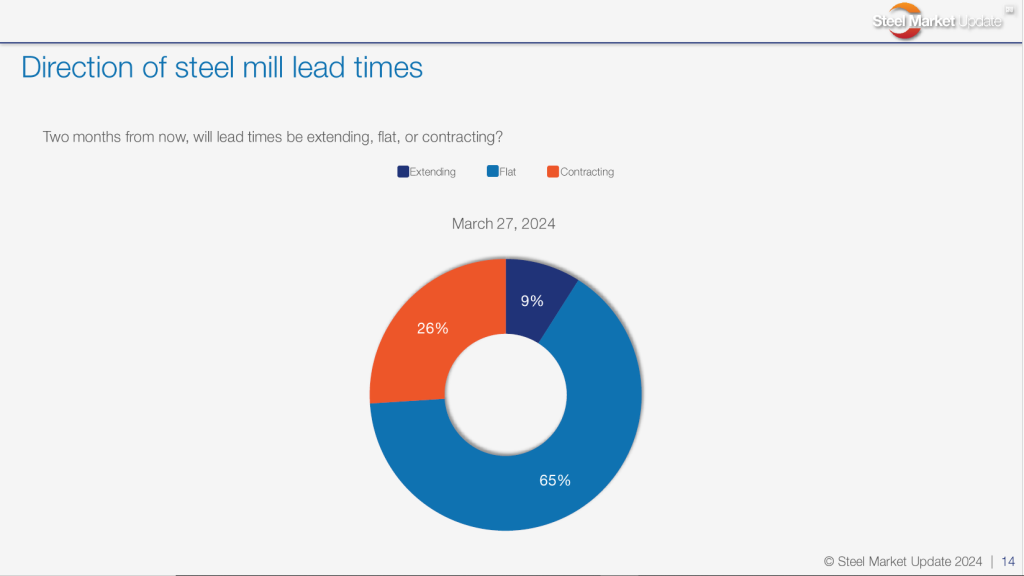

SMU’s survey says…

In this week’s survey, SMU asked steel buyers if they think lead times two months from now will be extending, flat, or contracting. Here are the results and responses to that question:

Flat – 65%:

“New normal.”

“We could be at an inflection point in May or June after restocking.”

“[Lead times] are already expanding, will continue to expand in the next 4-6 weeks, and then will be flat from there.”

“New economy with steelmageddon volumes will keep lead times flat, yet the mills should be able to demand higher prices.”

Contracting – 26%:

“Spring outages will be done; imports will still be a factor. We expect to see real ‘summer doldrums’ this year.”

“I think the summer slowdown will put pressure on lead times.”

“July is always a dip down.”

“Summer slowdown.”

“Mills will be countering excess inventory being traded among service centers.”

Extending – 9%:

“Heading into higher demand.”

“In keeping with last year’s trend, lead times will increase as the mills fulfill the large deals made in March. This should buoy lead times through Q2.”

Look for SMU’s next lead time update on Thursday, April 11.

Note: These lead times are based on the average from manufacturers and steel service centers participating in this week’s SMU market trends analysis survey. SMU measures lead times as the time it takes from when an order is placed with the mill to when it is processed and ready for shipping, not including delivery time to the buyer. Our lead times do not predict what any individual may get from any specific mill supplier. Look to your mill rep for actual lead times. To see an interactive history of our steel mill lead times data, visit our website. If you’d like to participate in our survey, contact us at info@steelmarketupdate.com.