Prices

October 6, 2013

Survey: When Will Prices Fall?

Written by John Packard

During the past few surveys, Steel Market Update has been asking if the additional tonnage being brought on-stream by U.S. Steel (Lake Erie), ThyssenKrupp Steel USA (building back slab inventory) and AK Steel would cause an imbalance in supply-demand ratios. Almost everyone within the industry has been of the opinion that the extra supply would create a situation where there is too much steel available and flat rolled steel prices will retreat.

However, with the price increase announcements we thought it would be interesting to review what our respondents are telling us this past week compared to early September results.

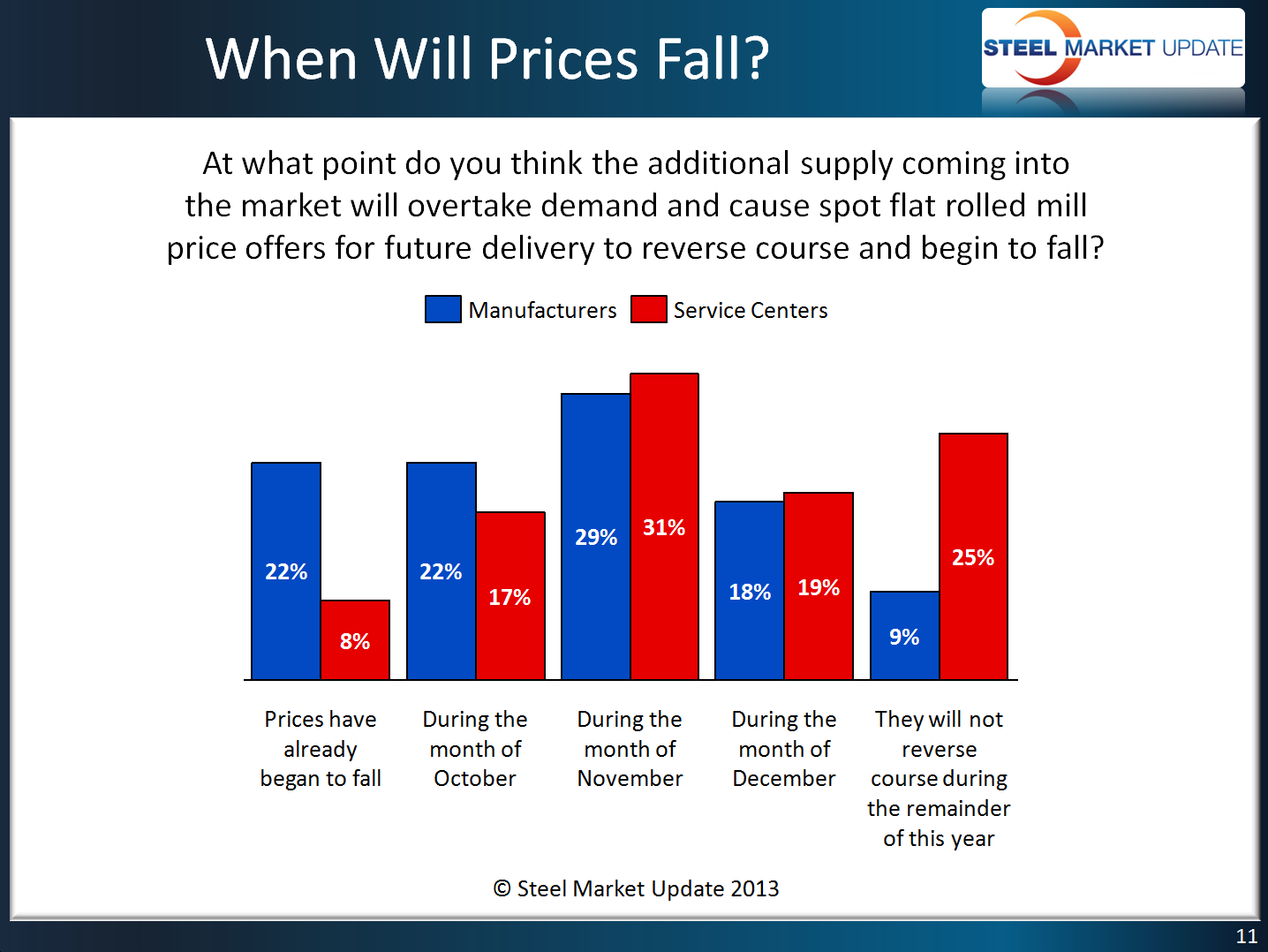

In our most recent survey we found interesting spikes at both ends of the spectrum from different industry groups. It appears a larger percentage of end users believe prices have already begun to fall as 22 percent of manufacturing companies responded that way while only 8 percent of service centers agreed. At the other end of the spectrum 25 percent of the service centers believe prices will not reverse course and move lower during the balance of 2013. Only 9 percent of manufacturing companies agreed.

In our most recent survey we found interesting spikes at both ends of the spectrum from different industry groups. It appears a larger percentage of end users believe prices have already begun to fall as 22 percent of manufacturing companies responded that way while only 8 percent of service centers agreed. At the other end of the spectrum 25 percent of the service centers believe prices will not reverse course and move lower during the balance of 2013. Only 9 percent of manufacturing companies agreed.

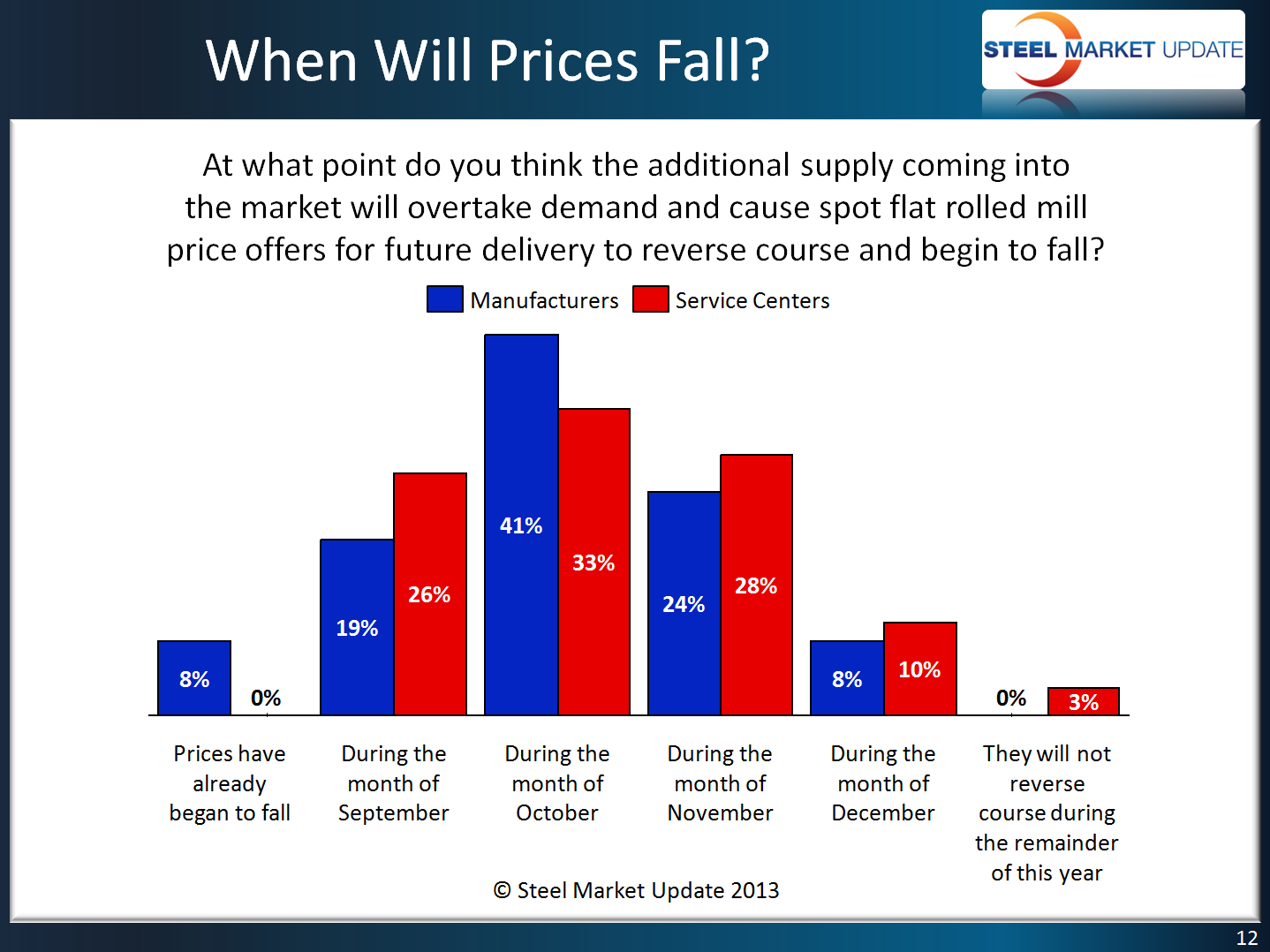

Here is what the respondents to our beginning of September survey (click on thumbnail to expand graphic for easier readability). As you can see one month ago only 3 percent of service centers and zero percent of end users believed prices would not reverse course and move lower prior to the end of the year. At that time 8 percent of the end users reported prices as having already beginning to fall with none of the distributors agreeing with those end users. At that point in time 60 percent of the manufacturers believe prices would drop in September or October with 59 percent of the distributors agreeing.

The most recent survey was taken as price announcements were being made by the domestic flat rolled steel mills and provides an early view of the opinions of both buyers and sellers of steel. We will need to give the mills a few weeks to see if they are able to convince buyers that the new price levels are reasonable and fair in today’s market. SMU will be following the ongoing dialogue between the mills and their customers to see if they will be successful in pushing prices higher in the coming days and weeks.

The most recent survey was taken as price announcements were being made by the domestic flat rolled steel mills and provides an early view of the opinions of both buyers and sellers of steel. We will need to give the mills a few weeks to see if they are able to convince buyers that the new price levels are reasonable and fair in today’s market. SMU will be following the ongoing dialogue between the mills and their customers to see if they will be successful in pushing prices higher in the coming days and weeks.