Analysis

November 14, 2013

NAFTA Vehicle Production for October

Written by Peter Wright

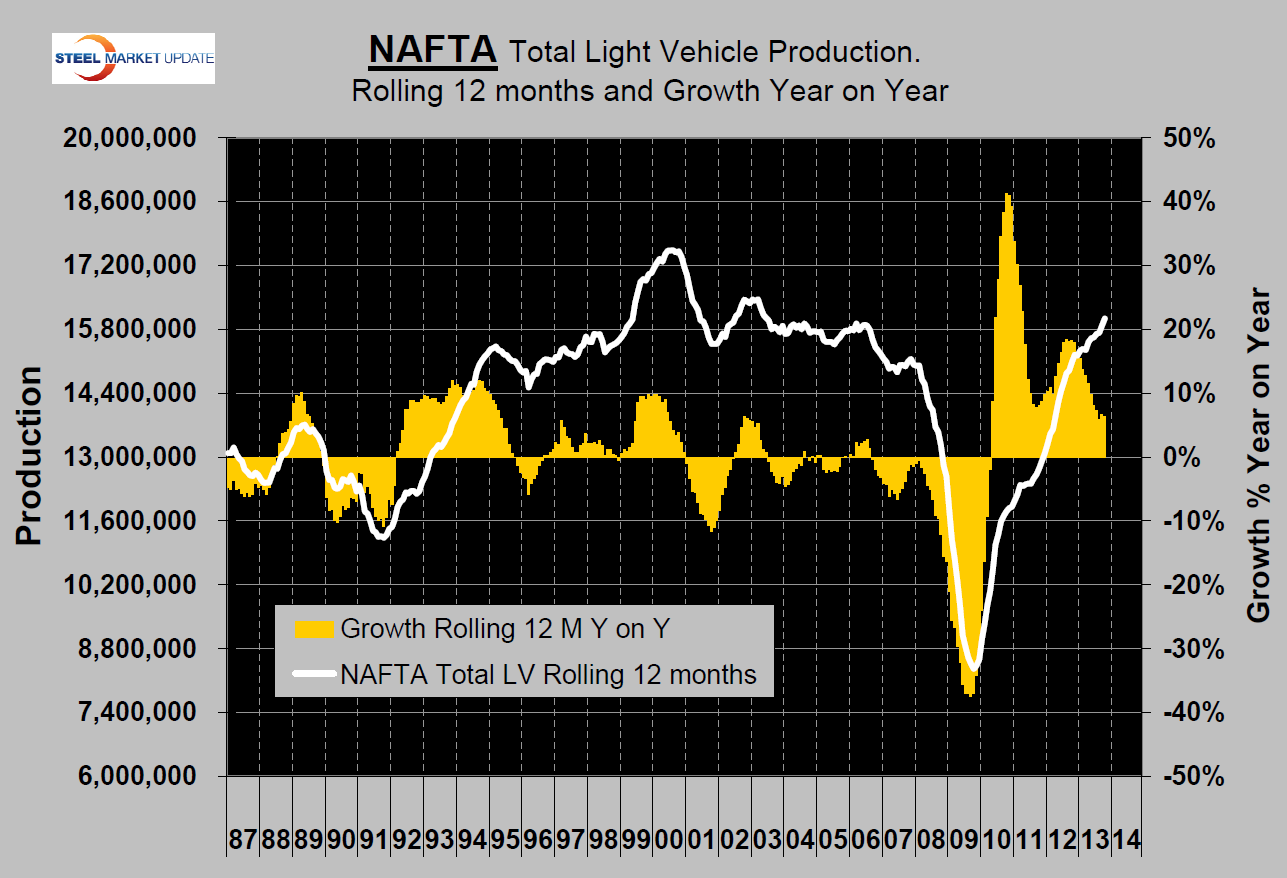

Light vehicle (autos + light trucks) production surged in October, up 13.5 percent, the rolling 3 months production was up by 13.1 percent. Year over year production was up by 8.3 percent in total and the Detroit 3 made up some ground being up 10.1 percent. Light vehicle production has now exceeded the pre-recession level (Figure 1).

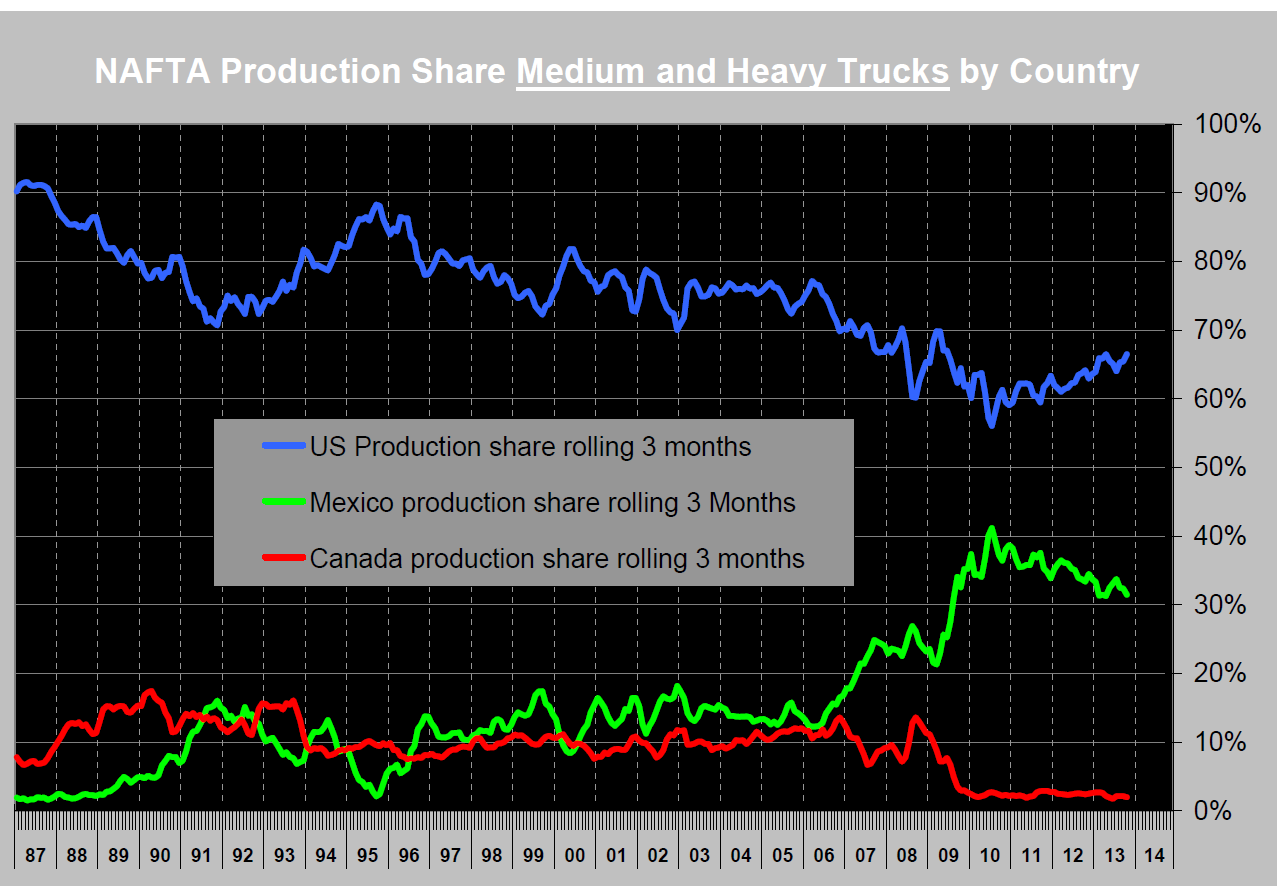

The corresponding figures for medium and heavy trucks were October/September up 15.3 percent, rolling 3 months up 4.3 percent and year over year down 0.2 percent.

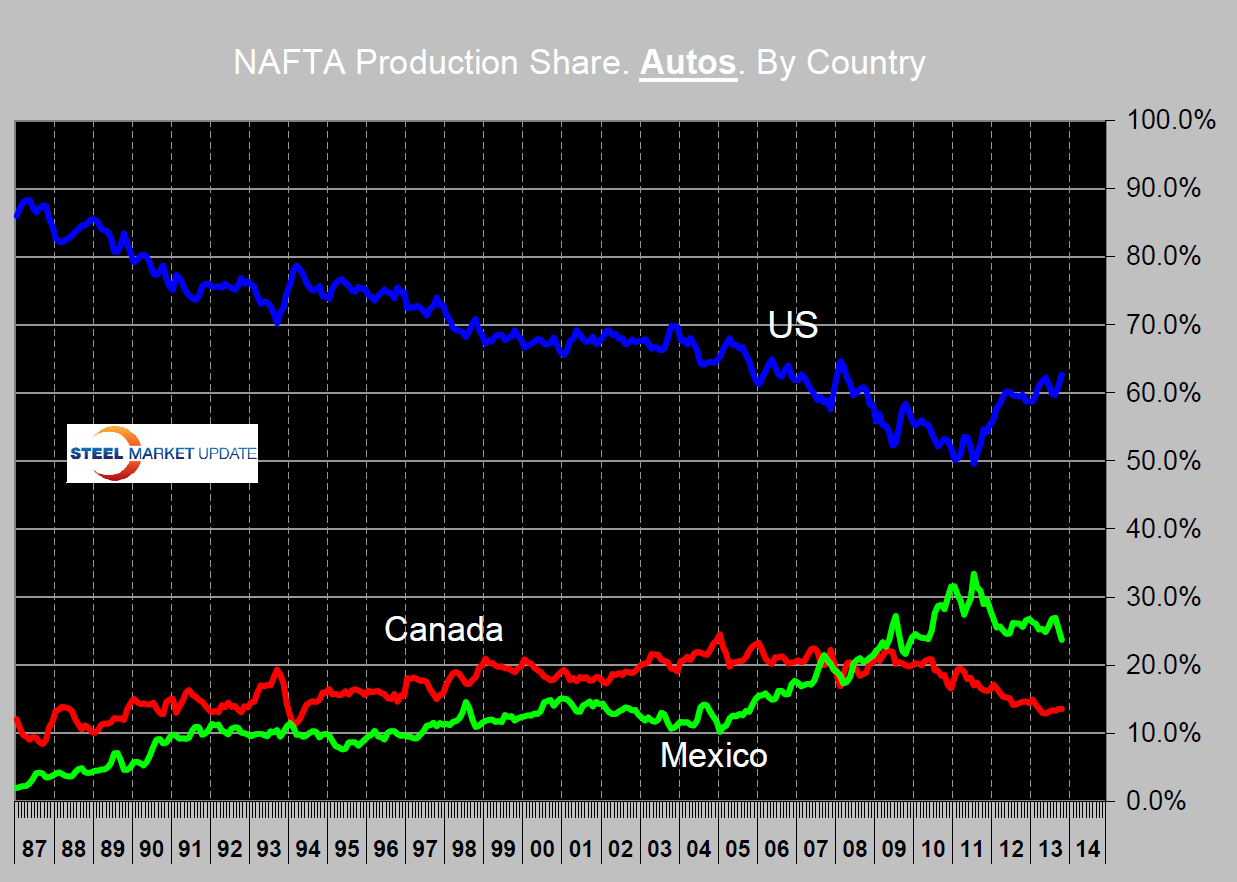

The dramatic change in the production share of autos within NAFTA continues. The US has been taking share from Mexico since mid 2011 and Canada’s share continues to languish (Figure 2). The production share of light trucks hasn’t changed much in the last four years with the US currently holding 71.6 percent. The trend in production share of medium and heavy trucks has been just as dramatic as for autos with the US surging at Mexico’s expense. Canada is almost out of this race (Figure 3).

Medium and heavy truck production has historically been a good leading indicator of recessions with about an 18 month time horizon. This product peaked in January 2013 but has since been staggering along with little direction. This is probably another symptom of uncertainty in the general economy as Washington procrastinates.

US vehicle sales declined slightly in October at 15.2 million units (annualized) with an equal split between autos and light trucks. This was weaker than expected as the government shutdown weighed on sales during the first half of the month with no rebound in the second half. The October decline was in autos, light truck sales picked up slightly as demand for pickups remained strong. Total vehicle sales were 15.3 million in September and 16.1 million in August. (Source Wards Automotive)

{kind=link}

{kind=link}

{kind=link}