Prices

January 6, 2014

Steel Buyers Basics: Iron Ore

Written by John Packard

In the United States approximately 60 percent of the steel produced is through electric arc furnaces (EAF) used by so-called “mini-mills.” Electric arc furnaces use primarily scrap along with pig iron or DRI (direct reduced iron) to charge the furnaces. All of the long products (rebar, bar, angles, beams) are produced through EAF technology and a portion of the flat rolled products (plate, carbon sheet and coil) are produced this way. The balance is produced by fully integrated steel mills using blast furnaces and basic oxygen furnaces (BOF) where pig iron is produced the old fashion way using iron ore, coking coal and limestone in the blast furnace and then is coupled with scrap in the BOF to produce steel. Almost all of the exposed automotive sheet steel is produced by fully integrated mills (blast/BOF) in the United States.

The growth of the mini-mills in the United States is due to the abundance of available scrap since the North American economies have been large consumers of steel for many years and the life span of the products is such that we collect and recycle vast quantities of the scrap. The U.S. is a net exporter of scrap.

In China the economy is not as mature and the available pool of recyclable scrap is quite small compared to the country’s need for steel. Therefore, the vast majority of China’s 800 million metric ton steel industry is produced by fully integrated mills. Thus the country’s huge appetite for iron ore.

China uses 58 percent of the iron ore produced by the world each year for its integrated steel mills. Even more impressive is China uses 67 percent of the seaborne iron ore sold in the world with Australia and Brazil being the two major exporting countries of iron ore to Asia and elsewhere. These two countries represent 75 percent of the world seaborne trade.

There are three major iron ore mining companies who dominate the iron ore markets controlling 60 percent of the seaborne trade. Those companies are: Vale (Brazil), Rio Tinto (Australia) and BHP (Australia).

Up until 2009/2010 iron ore was sold on an annual contract basis. In 2009/2010 the ore companies switched to an index based system which ties ore prices to the spot market with adjustments which can be monthly or on a quarterly basis.

With China acting as both the marginal producer of domestic ore as well as the marginal buyer of searborne ore, global benchmarks are driven by the spot prices in China. Both Platts and The Steel Index spot iron ore prices are FOB Chinese ports.

Iron ore is not a homogenous product and therefore it is necessary to specify several factors so one cargo can be compared to another. The most important factor is the amount of iron or Fe% that can be found in the ore. The higher the ore content the more valuable the ore. The two most common ore types referenced are 58% Fe and 62% Fe. However, there are cargos of ore which exceed 62% as well as those well below 58%.

Prices referenced in the spot market are usually in the “fines” form. Fines are defined by Platts and TSI as the granular size of the particles in the ore is below 10mm for at least 90 percent of the cargo.

Iron ores contain a certain amount of moisture which add weight to the cargo. The Steel Index specifies 8 percent moisture content as the standard for 62% Fe fines and 10 percent as the maximum.

When sold iron ore prices are based on a “dry” (dry metric ton or dmt) basis. An adjustment needs to be made between the “wet” production numbers which are reported and the dry sales figures.

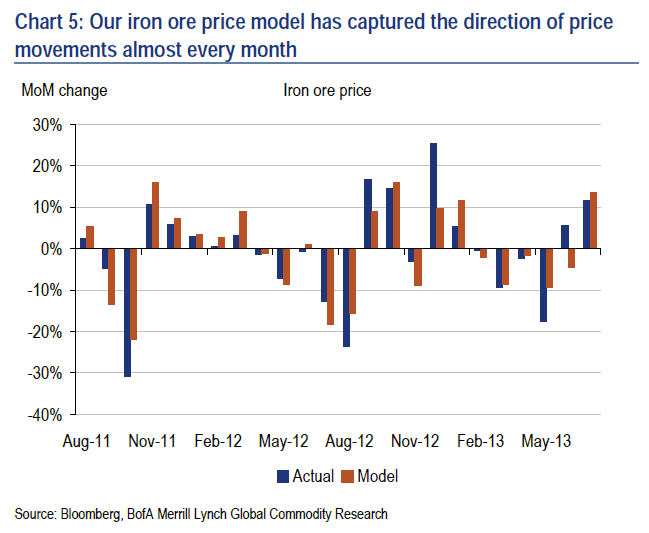

When looking at China and trying to forecast iron ore prices, Bank of America Merrill Lynch iron ore analyst Daniel Lian believes the following three components are important indicators of future price movements of iron ore:

1) China’s rebar prices

2) Iron ore stocks at mills as measured in weeks

3) Steel stocks at mills as measured in weeks

The Bank of America model has Chinese rebar prices as the most statistically important indicator for iron ore quotations, followed by iron ore stocks at the steel mills and then steel stocks being held on the floors of the steel mills.

According to the BoA analyst their model has consistently captured turning points in iron ore prices over the past few years (see below):

The Bank of America analyst went on to say that, “…a rally in iron ore prices was always preceded by sharp declines in rebar quotations. Meanwhile, iron ore stocks at steel mills usually stood at more than 20 weeks just ahead of major declines in iron ore quotations.”

As Steel Market Update continues to build our Premium Level products this is one area where we will begin to keep more data and prepare our own models to track iron ore spot pricing.

For our Executive Level members we will continue to monitor and report on iron ore price moves on an as needed basis.

For those who want to learn more about how iron ore, scrap, DRI and other products are used in the steelmaking process (both electric arc furnace and blast/BOF) you may be interested in attending our next Steel 101 workshop which will be held in Mobile, Alabama on February 4th and 5th. You can learn more on our website: www.SteelMarketUpdate.com