Market Data

March 3, 2014

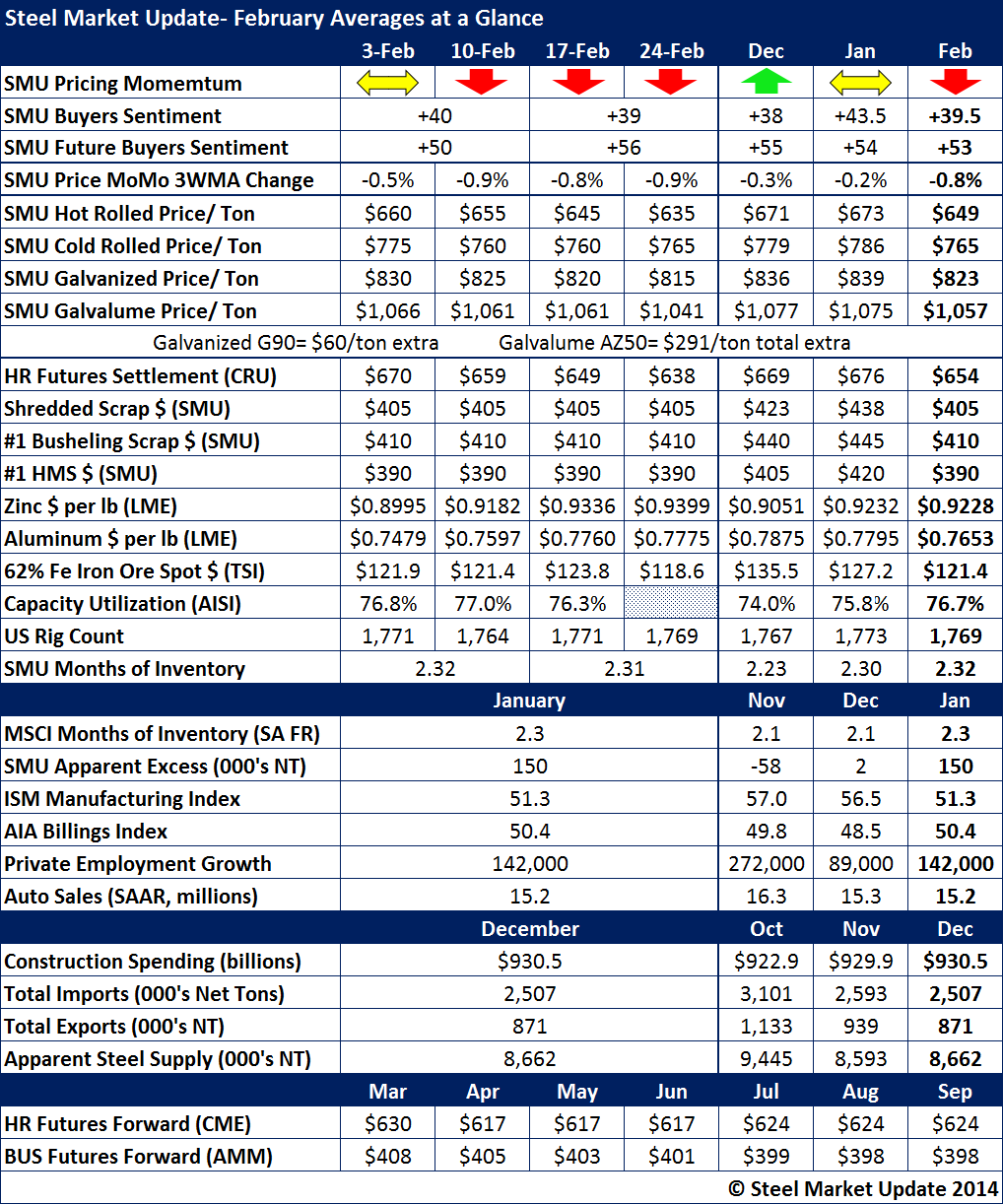

February Numbers at a Glance

Written by John Packard

Steel Market Update (SMU) Steel Buyers Sentiment Index averaged +39.5 which was down from the +43.5 reported during the month of January. Our SMU Price Momentum Indicator went from Neutral to Lower as we adjusted our indicator to reflect the dropping steel prices which we expect to continue over the next 30 days.

Benchmark hot rolled prices averaged $649 per ton for the month (last week HRC prices were reported by SMU at $635 per ton). This was $5 per ton lower than the $654 average reported by CRU.

Compared to the end of January numbers, hot rolled dropped $30 per ton during the course of the month of February. The lower end of the range dropped $20 while the upper end of the range was reduced by $40 per ton. Cold rolled declined by $25 per ton with the lower end of the range dropping $10 while the upper end of the range slipped $40 per ton. Galvanized averages dropped $15 per ton with $10 coming from the low end and $20 from the upper end of the range. Lastly, Galvalume dropped $25 per ton with $20 from the low end and another $30 sliding off the top end of the range. We produce a table with these numbers for our Monthly readers each and every month.

Key steelmaking commodity prices also dropped during the month of February. Scrap prices were down approximately $30 per gross ton (or more) on the Midwest items analyzed by SMU. Iron ore spot prices (China) also dropped to an average of $121.4/dmt for 62% Fe. At the end of the month iron ore spot was below $120/dmt at $118.6 according to TSI data.

SMU Apparent Excess rose to 150,000 tons. If you would like to learn more about Apparent Excess/Deficit you can read about it on our website. This is one of the Premium Level products produced by Steel Market Update.