Market Data

March 9, 2014

Job Growth on Path for Full Recovery by Mid-2014

Written by Peter Wright

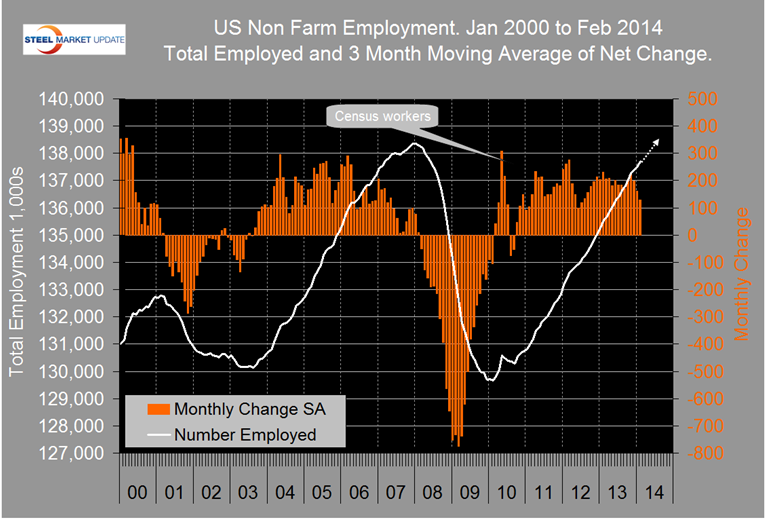

The Bureau of Labor Statistics (BLS) report on non-farm employment beat the consensus expectation of a 150,000 gain in February by showing a net gain of 175,000 jobs. The three month moving average (3MMA) of the net gain has slowed for three consecutive months but the growth trajectory is still on track for a full recovery by the middle of this year (Figure 1).

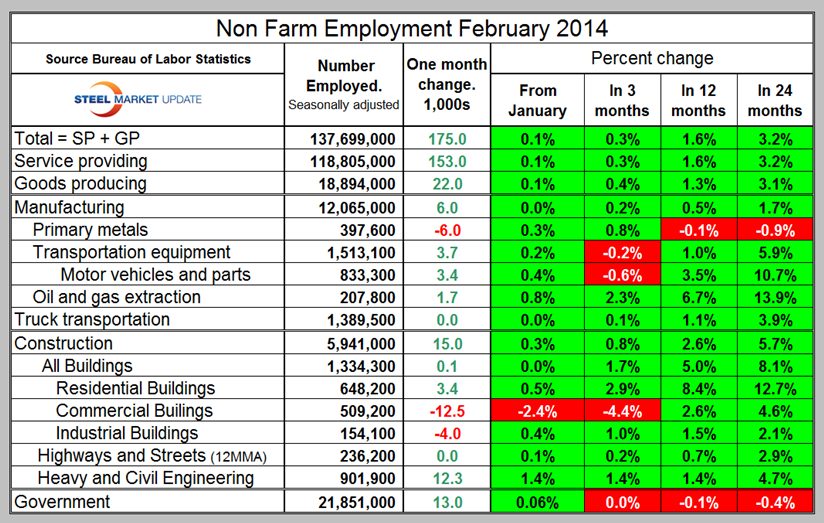

A total of 153,000 jobs were created in service industries and 22,000 in goods producing. The January result for the goods producing sector was revised down by 15,000 all of which was in manufacturing. Of the net new goods producing jobs gained in February, 6,000 were in manufacturing and 15,000 in construction (Table 1). The private sector created 162,000 jobs and government added 13,000 in February.

The BLS monthly employment report released on Friday has been summarized by SMU as follows:

Nonfarm payroll employment rose by 175,000 in February, and the unemployment rate, at 6.7 percent, changed little. Employment increased in professional and business services and in wholesale trade but fell in the information industry. The revisions for December and January increased nonfarm employment by 25,000. Monthly job gains have averaged 129,000 over the past 3 months. In the 12 months prior to February, employment growth averaged 189,000 per month.

Average hourly earnings of all employees on private nonfarm payrolls rose by 9 cents in February. Over the past 12 months, average hourly earnings have risen by 52 cents, or 2.2 percent. From January 2013 to January 2014, the Consumer Price Index for All Urban Consumers (CPI-U) rose by 1.6 percent.

The labor force participation rate was unchanged at 63.0 percent in February. Over the year, the labor force participation rate has declined by 0.5 percentage point. The employment-population ratio, at 58.8 percent, was unchanged in February and has shown little movement, on net, over the past 12 months.

Nonfarm business sector labor productivity increased at a 1.8 percent annual rate during the fourth quarter of 2013. The increase in productivity reflects increases of 3.4 percent in output and 1.6 percent in hours worked. From the fourth quarter of 2012 to the fourth quarter of 2013, productivity increased 1.3 percent as output and hours worked rose 2.9 percent and 1.7 percent, respectively. BLS defines unit labor costs as the ratio of hourly compensation to labor productivity.

Manufacturing sector productivity increased 1.3 percent in the fourth quarter of 2013, as output increased 5.0 percent and hours worked increased 3.6 percent. Over the last four quarters, manufacturing productivity increased 1.9 percent, as output increased 3.0 percent and hours increased 1.1 percent. Unit labor costs in manufacturing decreased 0.1 percent in the fourth quarter of 2013 and declined 1.0 percent from the same quarter a year ago. In the manufacturing sector, annual average productivity growth was revised down to 1.8 percent in 2013, the same rate as in 2012. Manufacturing unit labor costs fell 0.9 percent in 2013 as the 1.8 percent increase in productivity was greater than the 0.9 percent increase in compensation per hour. The gain in hourly compensation was the smallest in the annual series which extends back to 1988.

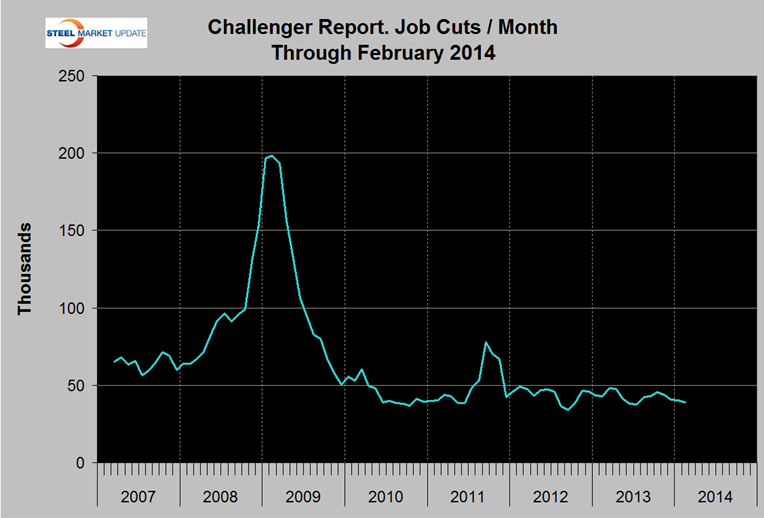

The Challenger Job-Cut Report, released monthly, provides information on the number of announced corporate layoffs. It is produced by Challenger, Grey & Christmas and tracks layoffs by industry and region. The report is an indicator used by investors to determine the strength of the labor market. U.S.-based employers announced plans to shed 41,835 workers from payrolls in February. Job cuts have been trending down for the last two years (Figure 2). The three month moving average (3MMA) of cuts on a year / year basis has been declining for the last four months and in February was down by 8.5 percent. The 3MMA is well below the pre-recessionary level. Construction, susceptible to weather-related disruptions, has only announced 218 job cuts so far this year.

SMU Comment: employment is one of the key foundation stones of future steel demand as it drives consumer confidence and spending. We are not depressed about the December through February results as the long term fundamentals are still strong. Moody’s Analytics expects that in the spring monthly payroll gains will rise to > 200,000 per month in line with the strong addition of 274,000 added in November.