Analysis

May 20, 2014

US Vehicle Sales and NAFTA Vehicle Production in April 2014

Written by Peter Wright

Light vehicle sales in the US declined to an annual rate of 16 million units in April following March’s torrid pace of 16.4 million. Even so, April was third only to November 2013 and March 2014 in the last eight months. Light vehicles are cars and light trucks (GVW Classes 1-3, under 14,001 lbs.). The increase in light truck sales continues to outpace autos partly a result of demand from contractors.

The mix was 8.5 million and 7.5 million for light trucks and autos respectively in April. The light truck share of sales exceeded 53 percent for the first time since mid-2011. Moody’s reported in Economy.com: “Sales growth is expected to accelerate throughout the remainder of the year and reach 17 million units SAAR by the end of the year. Sales will climb even higher in 2015 before receding to a more sustainable pace below 16 million units.”

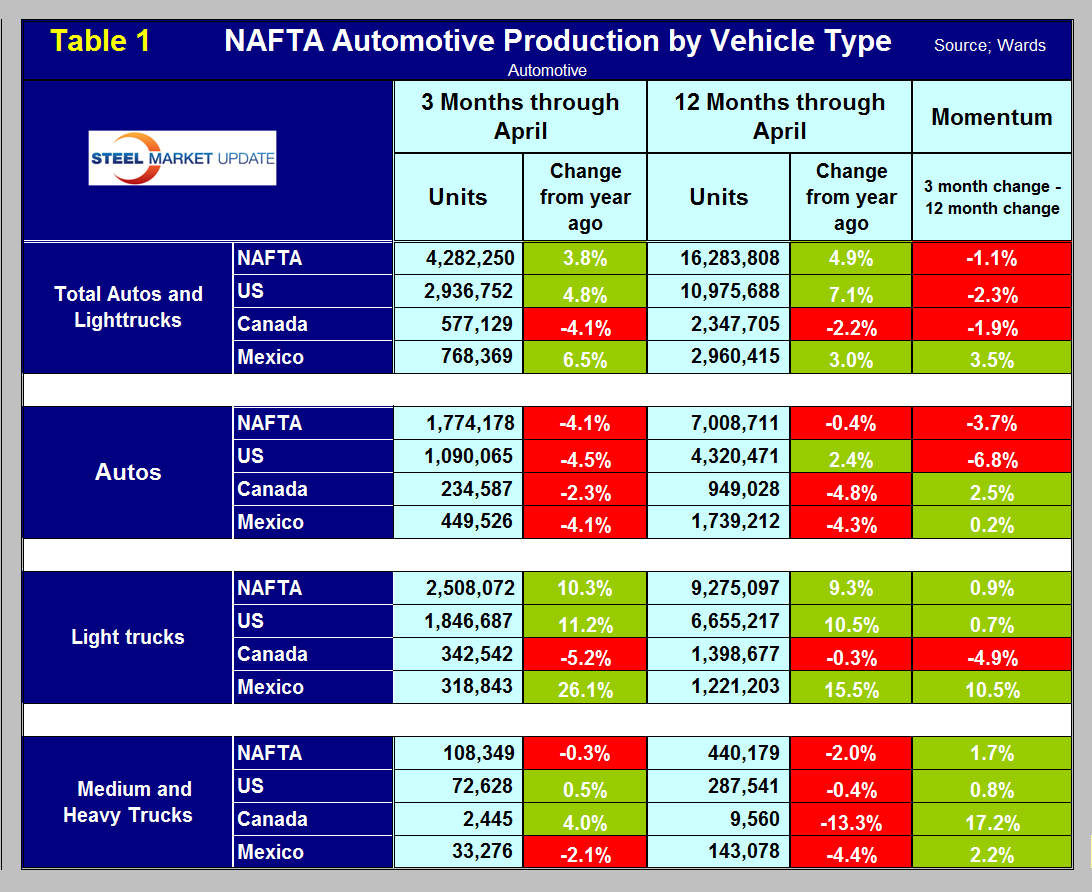

Total light vehicle production in NAFTA in April was at an annual rate of 16,966,644 units. Medium and heavy truck production was at an annual rate of 445,236 units. Light vehicle production in NAFTA declined by 68,936 units in April to 1,483,887 million units. However the rolling three months increased by 3.8 percent from 4,165,434 units to 4,282,250 units. On a rolling 3 months basis the US, Canada and Mexico grew by 4.8 percent, negative 4.1 percent and 6.5 percent respectively. Table 1 shows the growth of autos, light trucks and medium and heavy trucks on a rolling 3 and a rolling 12 months year over year.

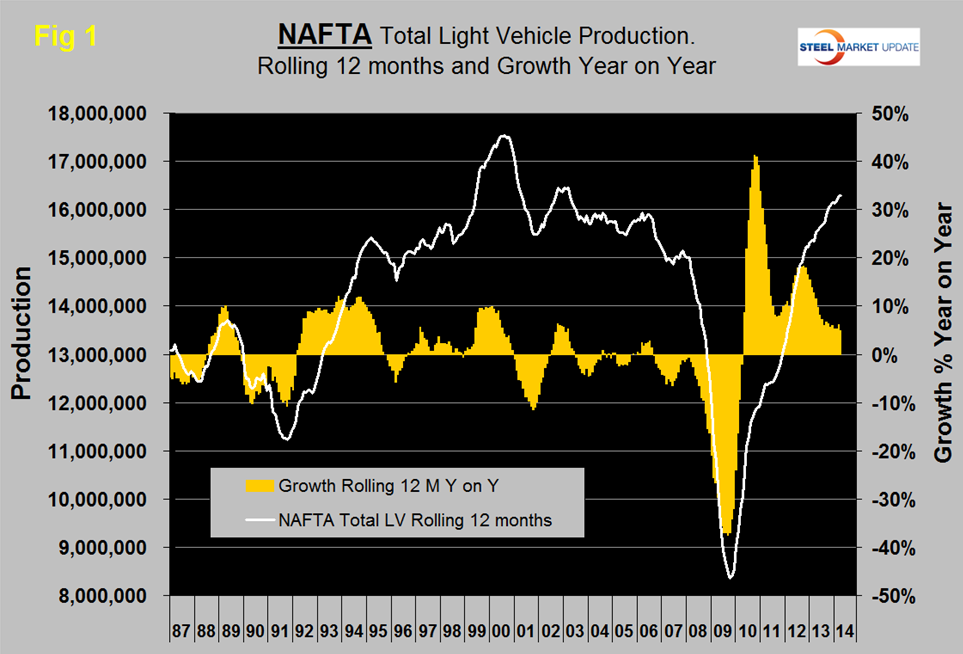

Compared to Feb – April 2013, the production of autos declined in all three countries. The production of light trucks declined in only Canada and medium and heavy trucks declined only in Mexico. Total light vehicle production in NAFTA is now 4.1 percent higher than it was in the pre-recessionary peak of Q2 2006, (Figure 1).

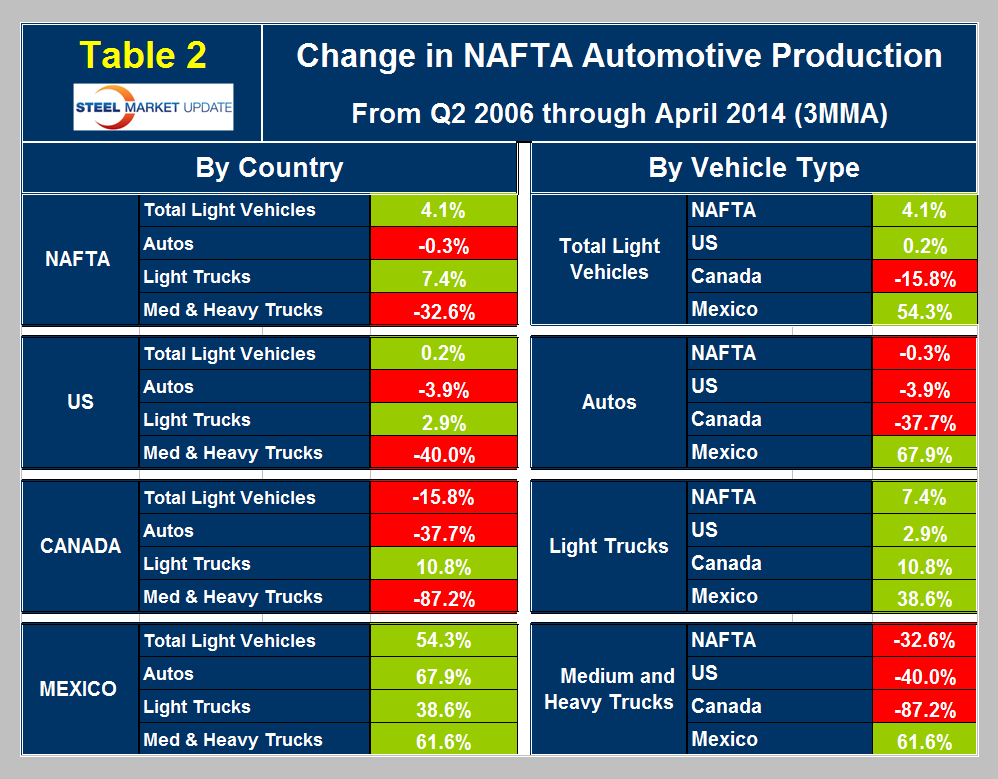

However there is a big difference between the recoveries of the three nations, (Table 2).

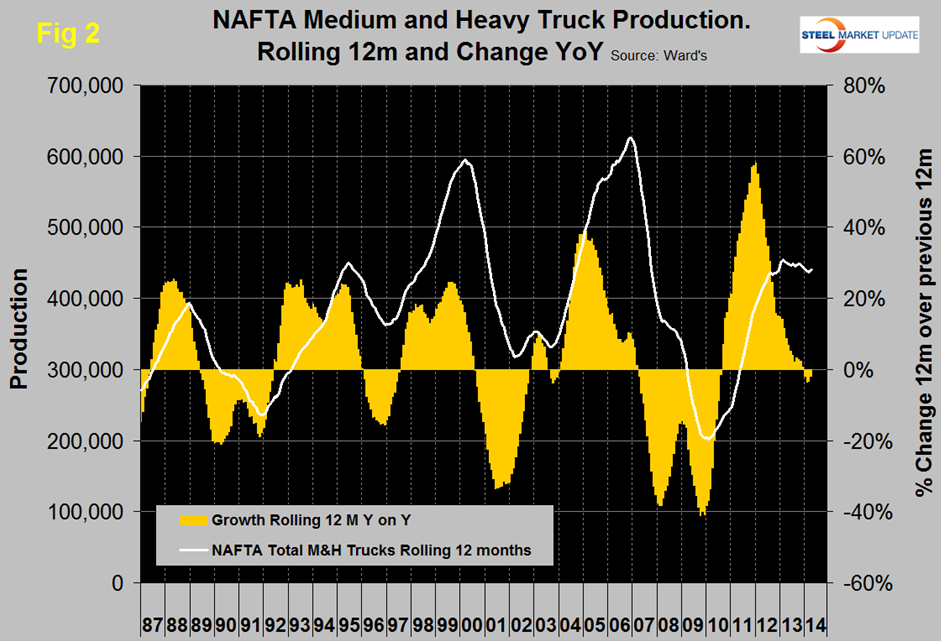

In April the US went over the 2006 threshold for the first time since the recession and is up by 0.2 percent. Canada is still down by 15.8 percent and Mexico is now up by 54.3 percent. The 12 month rolling production of medium and heavy trucks has had a negative growth rate every month this year, (Figure 2).

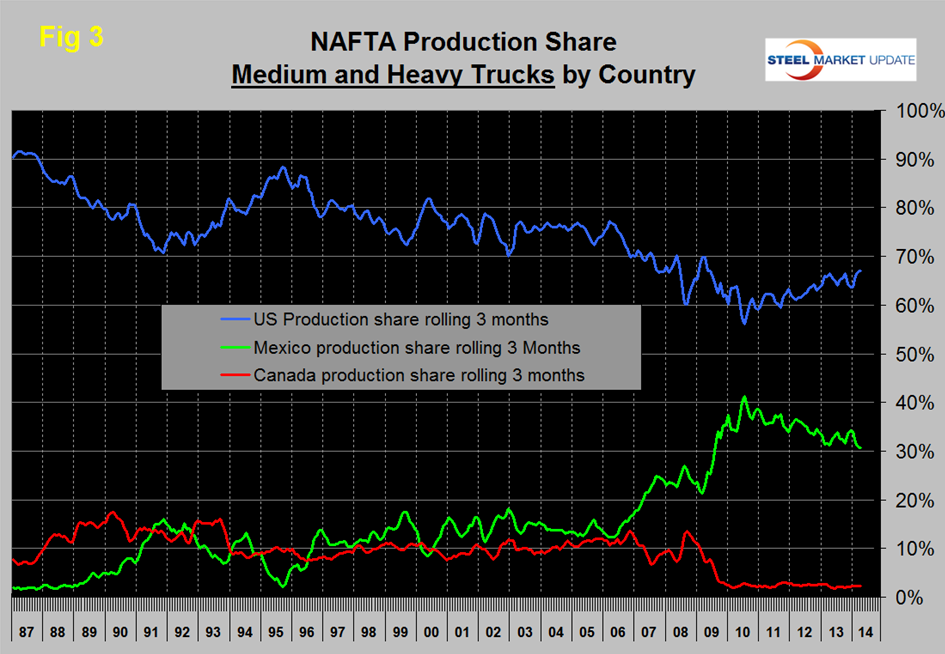

We have reported in the SMU in earlier months that the production share of autos in NAFTA has been trending in favor of the US for over three years. This trend is also very strong for medium and heavy trucks, (Figure 3). It looks as though Canada, with a production share of only 2.3 percent of medium and heavy trucks has been more or less written off by the OEMs as an assembly region.

Ward’s Automotive reported last week that light vehicle inventories grew by 7 days of supply in April to 69 days. Inventories of the Detroit 3 grew by 4 from 66 days at the end of March to 80 days at the end of April.