Market Segment

May 21, 2015

Threats of Dumping Suits & USW Negotiations

Written by John Packard

There are going to be two main themes which SMU and other steel periodicals will be writing about over the coming months (between now and our Steel Summit Conference at the beginning of September). The two themes are: anti-dumping suits on light flat rolled products and union contract negotiations between U.S. Steel and ArcelorMittal USA (as well as Cliffs Natural Resources whose contract expires after the USS and AM contracts). Both of these issues should be at the forefront of every executives desk as they look at making steel purchasing, inventory and selling decisions. Of course, we encourage everyone to stay tuned to Steel Market Update as we will report on these important issues as we get closer to deadlines or when we see changes on the horizon.

The rumor mill continues to spew out information with no backup documentation regarding potential dumping suits on cold rolled and coated products. Every mill talks about “unfair trade” in just about every public forum and customers are hearing from their mill salespeople that suits are likely soon. The comment we hear consistently regarding the filing of trade suits is, “It is not about if, but rather when suits will be filed.”

Having been burned last year when the rumor mill was also pointing toward a trade suit before the end of the year, we are taking the rumors with a grain of salt (we are not yet believers). However, we don’t buy a pound of steel so our comfort zone is different than those of you who buy and sell steel for a living.

As we hear rumors of a possible trade suit we are also being advised, “There are multiple Chinese CR offers available for late summer arrival priced at $24-25.50 base loaded truck, Houston.” This is about $80-$100 per ton below what most domestic mills are looking for (before taking into consideration freight costs). This same service center source went on to question, “…, it’s quite perplexing. The domestics certainly are seeing increased activity, slightly longer lead-times, and slightly higher spot prices, as evidenced by the various index measures. At the same time, we’re seeing import prices still at attractive and aggressive levels.”

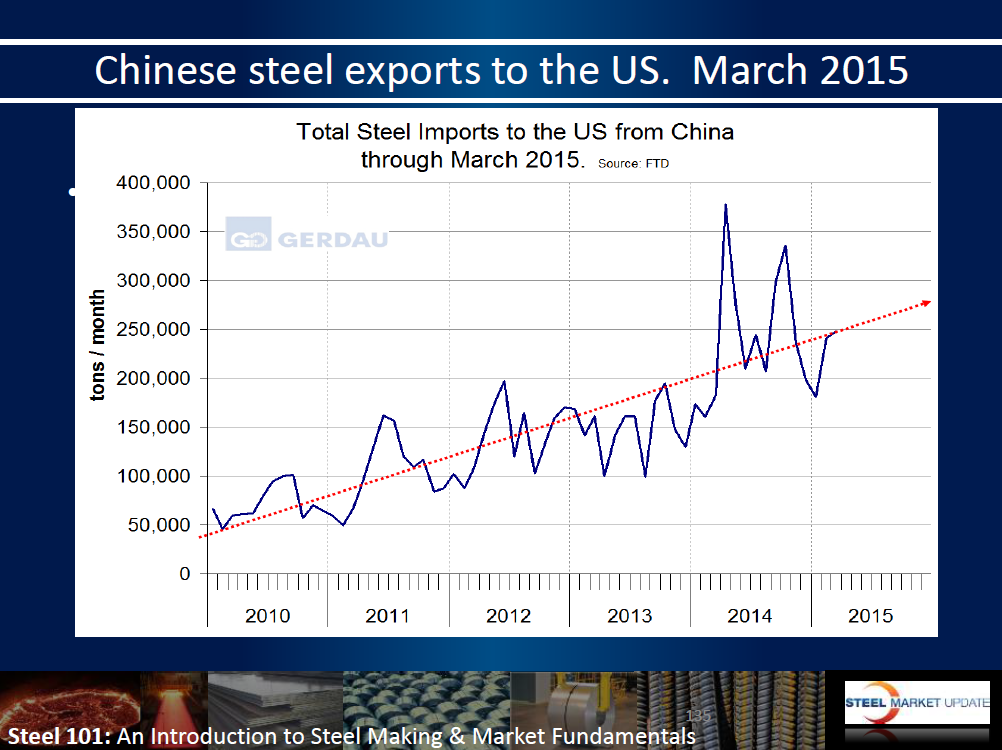

So the threat of dumping suits is not having the desired affect of reducing the amount of foreign tons (especially Chinese) from coming into the country. During the SMU Steel 101 workshop earlier this week, instructor Peter Wright (who is also a contributing writer to SMU) shared the following graphic on Chinese steel exports to the United States (all products):

For the month of March 2015, which is the last month we have Final Census Data on imported cold rolled, the U.S. received 191,723 net tons, of which 57,403 tons was from China (30 percent of the total).

Midnight, August 31, 2015

![]() The second issue are the negotiations between US Steel, ArcelorMittal and the United Steelworkers Union (USW). The contracts for both companies are set to expire at midnight on August 31, 2015. We have learned that none of the U.S. mills for either ArcelorMittal or US Steel have no-strike clauses. One mill, ArcelorMittal, has already begun framing their concerns on their website much as they did the last time negotiations occurred between AM and the USW.

The second issue are the negotiations between US Steel, ArcelorMittal and the United Steelworkers Union (USW). The contracts for both companies are set to expire at midnight on August 31, 2015. We have learned that none of the U.S. mills for either ArcelorMittal or US Steel have no-strike clauses. One mill, ArcelorMittal, has already begun framing their concerns on their website much as they did the last time negotiations occurred between AM and the USW.

Key ArcelorMittal USA findings (copy of full report can be gotten by clicking here):

• Labor accounts for 38 percent of the total conversion cost of steel and influences all major cost categories.

• Total labor costs for ArcelorMittal USA are more than $2.1 billion, with average annual wages per represented employee of $97,946, which are more than double the wages paid by similar size employers.

• Medical costs per ArcelorMittal USA employee continue to go up as the average age of our workforce increases, reaching $244 million in 2014 compared to $180 million in 2008.

• Our represented employees pay no health care premiums while the average employee at a similar size company covers 22 percent of their medical benefits package.

• Post retirement expenses – which include pensions, retiree medical and retiree life insurance – were $485 million in 2014. Although lower than the last three years, these costs are prohibitively expensive for the foreseeable future.

• In 2014, ArcelorMittal USA paid $257 million into pension funding per the legal requirements dictated by pension law.

• Despite retiree premiums holding steady from 2008 through 2014, retiree obligations continue to increase as retirees live longer and health care costs continue to rise. In 2014, our retiree health care cash payments were $123 million and are expected to increase to $184 million by 2019.

The USW has already begun to respond to the references made by ArcelorMittal. SMU saw a report from one USW local president as he shared information with his members, “USW president Leo Gerard said at the union’s Basic Steel Conference in Pittsburgh on May 7 that the union intends to reach a labour agreement that “looks beyond today,” USW Local branch 1011 president Lonnie Asher said in a May newsletter to members.”

Negotiations will begin in earnest a couple of months before the August 31st deadline.