Prices

June 23, 2015

SMU Analysis: Iron Ore, Metallurgical Coal & Zinc

Written by Peter Wright

This piece, written by Peter Wright, combines our own data analysis with recently published opinions about the iron ore, metallurgical coal and zinc markets that we find credible.

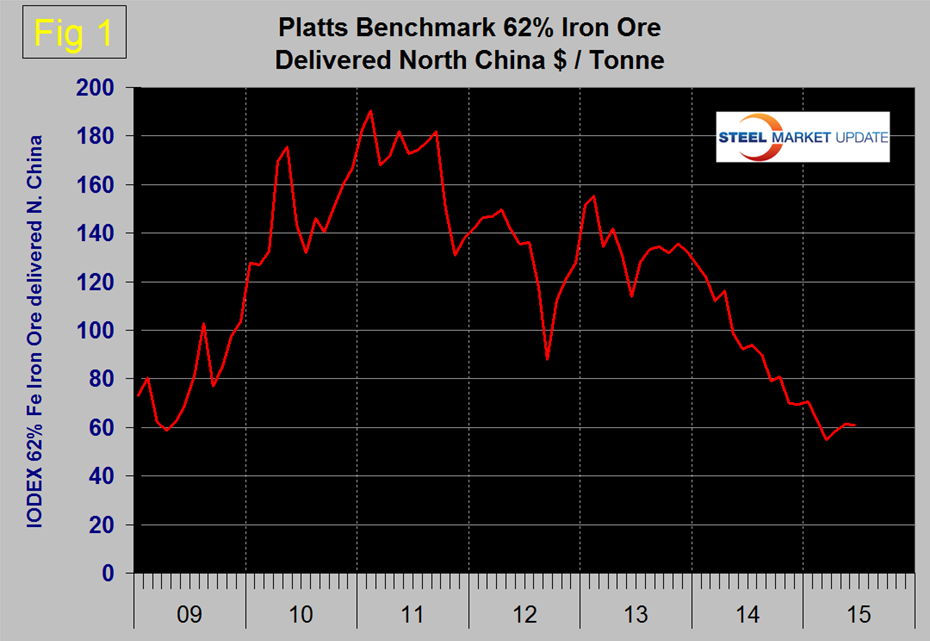

Iron Ore: The Platts IODEX of 62 percent Fe delivered North China recovered to $61.25 on March 22nd, continued its upward trend in June then on June 19th fell back to $61.00 per dry metric ton (dmt), (Figure 1).

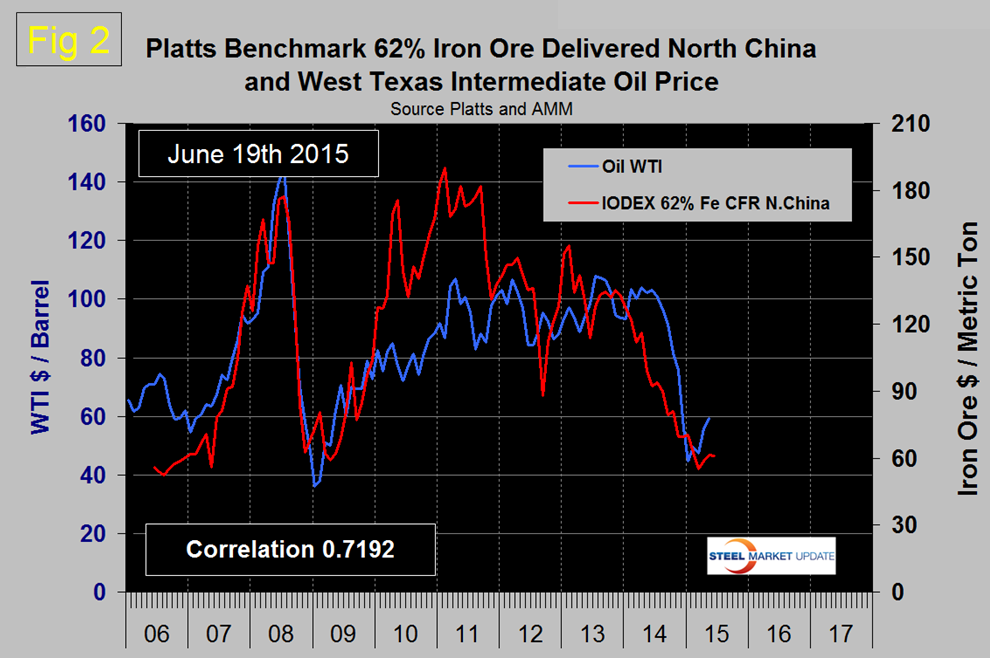

In these reports we will try to describe where we think the price of ore seems to be headed. There is a relationship between the price of ore and the price of oil. Both are international commodities driven by the state of the global economy and the value of the US dollar. However, the international global trade in oil is over 10 x more than the blue water trade in iron ore in dollar terms. Since 2006 there has been a correlation of 0.7192 between the IODEX and West Texas Intermediate crude which we don’t consider to be particularly close. However, the correlation in the three years between 2007 and 2009 was 0.9182 which we do consider to be a very close though non-causal relationship. The correlation was upset in 2010 and 2011 by the activities of the big 3 ore cartel to limit the availability of long term contracts. Since then the relationship has come back in line. The point is that since the global oil market is so much larger than the global ore marke,t we believe we can get some insight into whether ore is currently priced high or low relative to the oil benchmark. Figure 2 shows the ore/oil relationship since 2005.

Last month, in the first of these reports, we reported that ore had some upside potential and this is still the case though market interference is an issue. See below.

The following was written by Alpha world, published in Seeking Alpha on May 27th The sharp pullback in iron ore prices due to a supply glut in the seaborne iron ore market has hurt Australia’s finances. The reason for the supply glut has been the strategy adopted by the two Australian miners, Rio Tinto and BHP Billiton, along with Brazil’s Vale, to continue to ramp up production despite a slowdown in demand from China. This strategy seems to be working as several high-cost miners in Australia, and elsewhere, have been feeling the heat. However, the strategy was recently questioned by Australian politicians, with Prime Minister Tony Abbott even backing a parliamentary inquiry.

Rio Tinto and BHP have been ramping up production, although recently BHP did announce that it is slowing down its iron ore expansion plan. The two companies, along with Vale, have boosted production even as demand for the steelmaking ingredient has slowed down amid weakness in China. The idea behind this strategy is to drive out high cost miners and increase market share. Once the market has fundamentally balanced, the top three believe they can generate significant value for shareholders. However, not everyone agrees with this strategy. Fortescue, the fourth-largest iron ore miner, has been critical. In March, Fortescue’s Andrew Forrest even called for a cap on iron ore production. Not surprisingly, Forrest’s call for forming, essentially, a cartel was rejected by majors, with Rio chief Sam Walsh saying that his company will not collude with other miners to boost prices.

That did not stop Forrest from putting pressure on majors. He had been lobbying for an inquiry into the drop in iron ore prices. Along with some other high-cost miners, Forrest even formed Our Iron Ore campaign. Forrest’s concerns are understandable. Among the major miners, Fortescue is by far the weakest, with a significant debt on its balance sheet. In April, the company was forced to offer higher yields to refinance part of its debt.

Last week, it looked like Fortescue’s efforts were going to pay-off as the Australian Prime Minister backed a parliamentary inquiry into tactics adopted by majors. Andrew Mackenzie, CEO of BHP Billiton, called any such inquiry “a ridiculous waste of taxpayers’ money.” And it seems following lobbying from Rio Tinto and BHP Billiton, the Australian government has rejected an inquiry.

But does Rio Tinto and BHP Billiton’s strategy merit an inquiry? The answer would depend on whether the two companies have been involved in predatory pricing as has been alleged. In my opinion, their strategy is legitimate. According to Economics Help blog, predatory pricing occurs when a company sells a product or service at a price below cost. Neither Rio Tinto nor BHP Billiton can be accused of doing that. Their costs, even after including transportation costs, are below the market price. Even Vale’s costs, including transportation costs, are below this level. Going by the exact definition of predatory pricing, BHP Billiton and Rio Tinto are doing nothing wrong here. In predatory pricing, a company’s goal is to drive others out of business and establish a monopoly. The strategy adopted by majors will drive out some high-cost miners and the top three will indeed gain some market share, but that does not mean that they will be in a position to create a monopoly.

Also, the pullback in iron ore prices cannot be entirely blamed on majors ramping up production. Majors had undertaken plans to boost production at a time when iron ore prices were trading at $130 per ton, driven by demand from China. As new production came on line, China saw a sharp slowdown, especially in the construction sector. This has contributed to the supply glut.

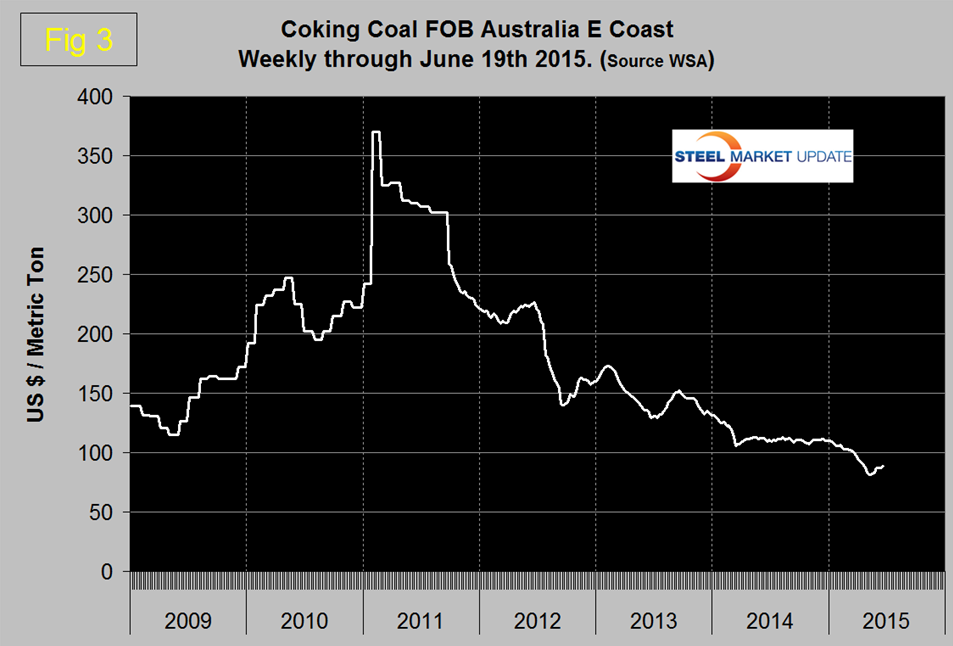

Coking Coal: The price of coking coal FOB East Australian ports declined steadily from $110.00/metric ton on January 2nd and bottomed out on May 15th at $81.65. Since then the price has risen every week to reach $88.70 on June 19th, (Figure 3).

Buyers have expressed interest in additional quantities, but agree to buy only at discounts. In China buying activity has slightly slowed down after local customers restocked in mid-May. However, Australian sellers have faced price headwinds due to strong competition from China’s domestic miners who are in no hurry to revise offers. Indian buyers have taken a wait and see mode intending to source required quantities under quarterly contracts.

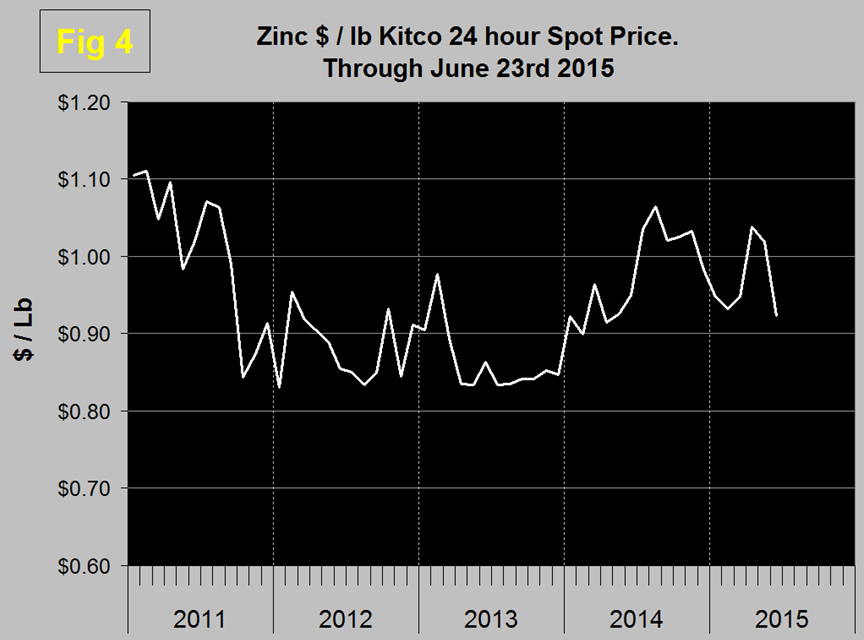

Zinc: According to the International Zinc Association, the major use of zinc is for galvanizing, other significant uses include the alloying of brass and bronze and in zinc-based alloys used in the die-casting industry. Kitco publish a daily spot price of zinc which we have transcribed to Figure 4.

At the end of May the 30 day spot peaked at 1.0105 but in June the price has exhibited an almost uninterrupted slide reaching $0.9237 on June 23rd.

On June 11th Platts Metals Insight reported that galvanized steel sheet production grew rapidly between 2005 and 2014, with only a slight dip in 2009 due to the global economic crisis, notching up an average global growth rate of 5 percent annually, analysts estimate. While there is no definitive production figure, sources point to a fairly strong upwards trend, with the industry driven by the construction sector, which takes 80 percent of output, and by the automotive sector, which takes 20 percent. The World Steel Association put partial global production of coated strip including galvanized at 107.6 million metric tons in 2013, up from 100.2 million mt in 2012 and 93.7 million mt in 2005, noting that growth has been strong in India and South Korea and most dramatic in China, which accounted for 40 percent of the 2013 total. Noble International put galvanized sheet output at 155 million mt in 2014, while Frank Goodwin, technology and market development director of the International Zinc Association has an estimate of 142 million mt.

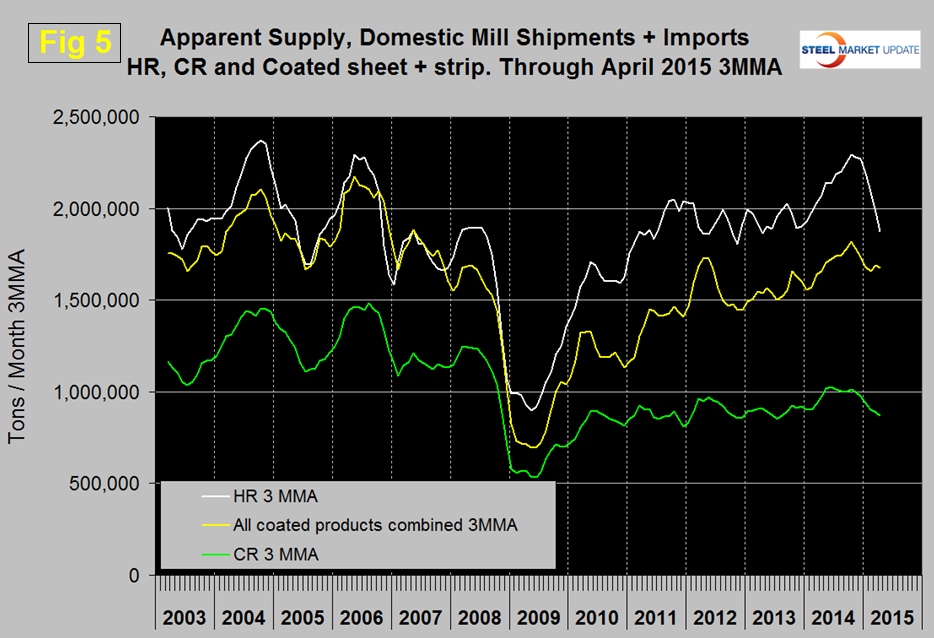

In our SMU analysis of steel supply we see the degree to which coated sheet products are growing much faster than cold rolled since the recession, (Figure 5). As construction continues to recover we see this trend continuing with a resultant increase in the demand for zinc.