Prices

July 7, 2015

US Steel Announcement Starts 3rd Round of Flat Rolled Price Increases

Written by John Packard

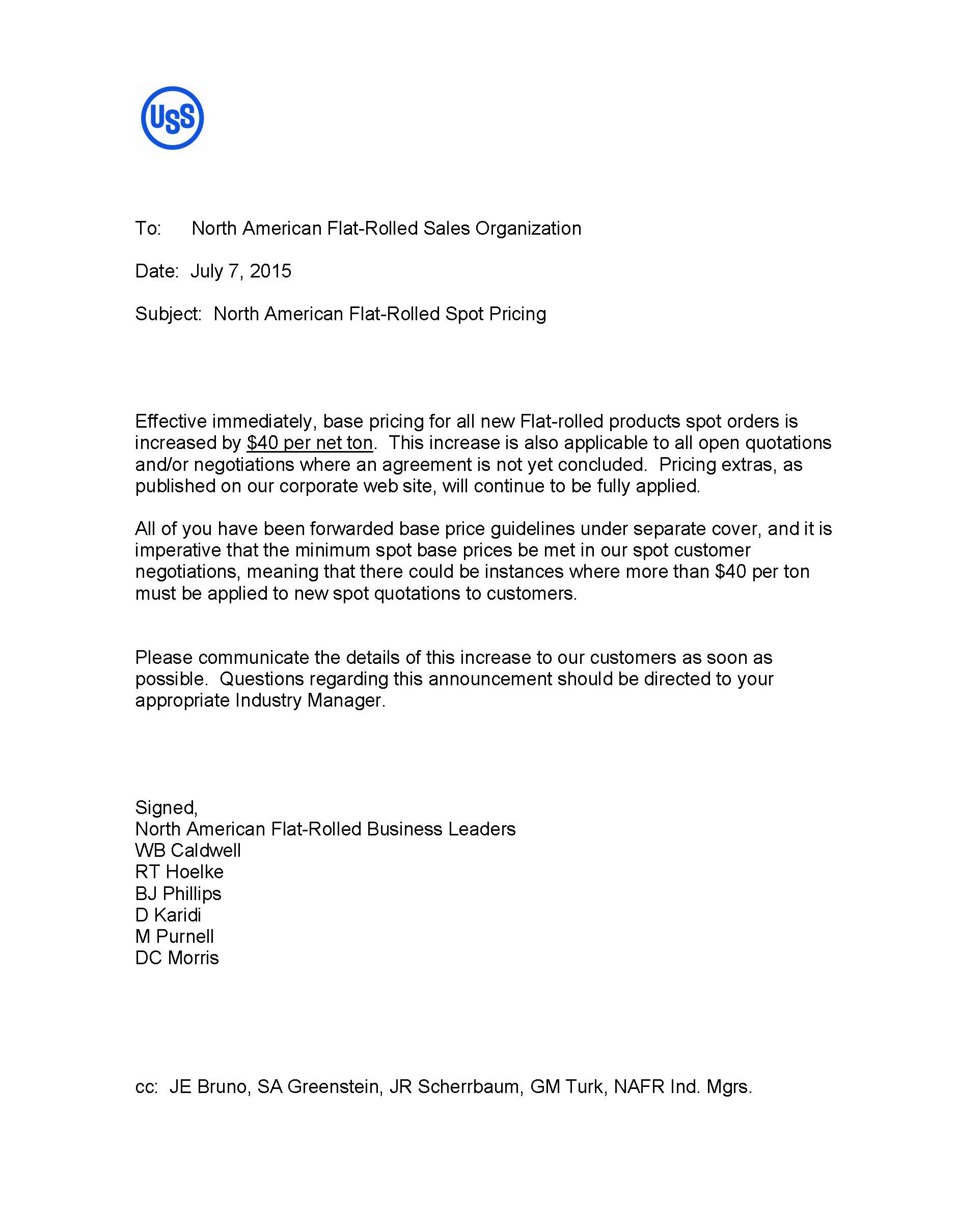

The domestic steel mills are determined to keep pricing momentum on their side as US Steel became the first mill to announce a new round of price increases on flat rolled products. The US Steel announcement, which was made via the use of an internal memo to their sales group leaked to the industry, advises their customers that base prices are being moved up by a minimum of $40 per ton ($2.00/cwt) on all new spot orders.

The mill advised their salespeople, “Effective immediately, base pricing for all new Flat-rolled products spot orders is increased by $40 per net ton. This increase is also applicable to all open quotations and/or negotiations where an agreement is not yet concluded. Pricing extras, as published on our corporate web site, will continue to be fully applied.

The mill advised their salespeople, “Effective immediately, base pricing for all new Flat-rolled products spot orders is increased by $40 per net ton. This increase is also applicable to all open quotations and/or negotiations where an agreement is not yet concluded. Pricing extras, as published on our corporate web site, will continue to be fully applied.

“All of you have been forwarded base price guidelines under separate cover, and it is imperative that the minimum spot base prices be met in our spot customer negotiations, meaning that there could be instances where more than $40 per ton must be applied to new spot quotations to customers.”

This is the third price increase announcement since April 28th when ArcelorMittal took prices up by $20 per ton. NLMK and Nucor at that time tried to set base price levels of $24.00/cwt ($480), $30.00/cwt ($600) and $23.00/cwt ($460) and $29.00/cwt ($580) on hot rolled, cold rolled and coated respectively. Prices tended to settle at the Nucor $460/$580 levels.

On the 10th of June, Nucor came out with a second round of price increases which essentially all of the other mills followed. The increase was for $20 per ton taking the asking minimum base price levels to $480 ($24.00/cwt) on hot rolled and $600 ($30.00/cwt) on cold rolled and coated. As of this past week, the mills had not yet been able to pass through all of the second price increase (although coated was stronger than hot rolled partially due to the antidumping suit filed against China, Taiwan, South Korea, India and Italy).

Customer reaction was muted as many are waiting to see what happens on the trade front and with foreign steel offers.

One end user told us that they didn’t think the full $40 had a chance. However, in the same email they told us, “SDI has short lead time, of course, so they are priciest. Received what I would characterize as a very high offer from Brazil (Usiminas) on HDG. Almost $ 700 all in – trader’s price so probably about 35 all in at a port warehouse. There is activity at Calvert – lead times have moved out and they are funneling orders thru a central AM group – could be coincidental. WN told me that their light gauge galvalume orders were so good, they ran NMLK out of feedstock thru mid-August.”

A service center executive was asked about how the steel mill salespeople were positioning their pricing at this time. We were told, “mostly they see near –term as “steady” but they keep bringing up labor talks and trade suits as their salvation, and thus they are positive US market will go higher. I think they are putting too much hope/emphasis on both issues. If they are successful in creating more anxieties, it may just serve to pull tons ahead, setting up a correction later.”

Another service center told SMU that their steel mill salesperson told him to expect another announcement soon that would help sell the new price increase. Perhaps the long-awaited cold rolled antidumping suite is coming?