Market Data

August 4, 2015

Lackluster Global PMI in July

Written by Sandy Williams

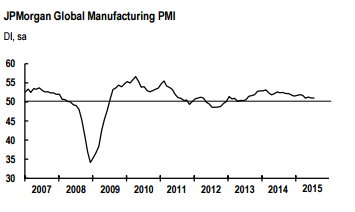

Global manufacturing was relatively flat in July. Increases in the Eurozone, North America and Japan could not offset contractions in Greece and Asia. The JP Morgan Global Manufacturing PMI registered 51.0, unchanged from June and continuing its weakest reading in two years.

Overall manufacturing output remained in the positive, above 50, range for the thirty-second consecutive month, with the strongest rate of growth seen in the Czech Republic, Netherlands, Italy and Poland. New orders continued to grow but at a slower pace as export business dropped off in China, German, France, the UK, Taiwan, South Korea, Turkey, Indonesia, Vietnam, Russia and Brazil.

Input costs were higher in June, with selling prices falling modestly during the month.

Input costs were higher in June, with selling prices falling modestly during the month.

“The global manufacturing sector remained on a subdued growth path at the start of the third quarter, according to the latest PMI surveys,” commented Joseph Lupton, Senior Economist at JP Morgan. “The headline index has tracked at a below long-run trend level in recent months as positive growth contributions from North America, Japan and Western Europe have been offset by the ongoing softness across Asia, Russia and Brazil manufacturing sectors. The lackluster trend in new order suggests the soft growth patch may continue in the coming months. This is also suggested by early signs that growth in consumer goods spending may have lost some steam in June.”

The Eurozone PMI held steady at 52.4 showing continued growth in the region for the past two years. Improved domestic and export kept July output strong. Input prices were higher for the fifth consecutive month due in part to a weakened euro. Selling prices increased only slightly in July. The financial upheaval in Greece drove nation’s PMI reading to a record low of 30.2 but caused little negative affect on manufacturing in the rest of the Eurozone

“Despite holding up well on prior months, the overall rate of growth in the region as a whole remains only modest, pointing to industrial production growing at an annualised rate of around 2%, commented Markit chief economist Chris Williamson. “Policymakers will be reassured by the robust growth rates seen in these countries and the resilience of the manufacturing sector as a whole, especially as growth is likely to pick up again now that Greece has jumped its latest hurdle in the ongoing debt crisis.”

China manufacturing contracted for the fifth consecutive month. Falling domestic and export orders caused manufacturers to cut production at the fastest rate since November 2011. The Caixin China General Manufacturing PMI registered at 47.8 down from 49.4 in June. Interest rate reductions by the Peoples Bank of China and other stimulus measures have, so far, failed to stem the downturn in manufacturing. Economists expect continued slowing in the second half of 2015.

The PMI reading in Japan jumped to its highest reading in five months at 51.2. Production output accelerated in July underpinned by higher order demand domestically and abroad. Raw material costs increased as the yen depreciated against the dollar.

Manufacturing conditions worsened in South Korea in July. Production and new orders both declined during the month. Employment levels fell at the fastest rate since November of 2014 as companies downsized as production waned. The headline PMI was 47.6 in July, still in contraction although up from 46.1 in June. Survey respondents cited “unstable economic conditions, reduced sales volumes and the MERS outbreak” as contributors to the latest contraction. New export orders fell for the fifth month in a row.

The PMI in Russia dropped slightly further into contraction at 48.3 from 48.7 in June. Indexes for production, orders, inventories and employment all declined in July. The only element that showed an increase was a “marked and accelerated” increase in input prices. ““A similar story at the start of the third quarter to the one told earlier in the year: the Russian manufacturing sector continues to broadly stagnate, dragged down by weakness in the capital goods category which is offsetting marginal growth in the consumer and intermediate goods areas,” said Paul Smith, Senior Economist at Markit.

In North America, Mexico saw a sharp rise in new export work that that accelerated output and new order rates. The composite PMI was 52.9 and has been above the 50 “no change” mark every month since October 2013. Employment picked up moderately in July as manufacturers increased operating capacity and capital expenditures. Input cost inflation was at a six month low but output charges rose at the fastest pace since April, reported Markit.

Canada manufacturing activity expanded in July although at a very modest pace. The RBC Canadian Manufacturing PMI dipped from a six month high of 51.3 in June down to 50.8 but still remained in the growth area. Exports picked up slightly with stronger demand from the U.S. due to a weaker exchange rate. Input prices increased contributing to the “most marked rate of factor gate price since February.”

“July’s survey highlights another steady upturn in manufacturing production and new order volumes, which leaves the sector well placed to remain on a recovery footing through the third quarter of 2015” said Cheryl Paradowski, president and chief executive officer, Supply Chain Management Association (SCMA). “Exchange rate depreciation and stronger U.S. consumer spending continue to help shore up demand for Canadian manufactured goods, in turn offsetting some of the momentum lost from weaker energy sector spending patterns.”