Market Data

October 3, 2015

Global Manufacturing Flat in September

Written by Sandy Williams

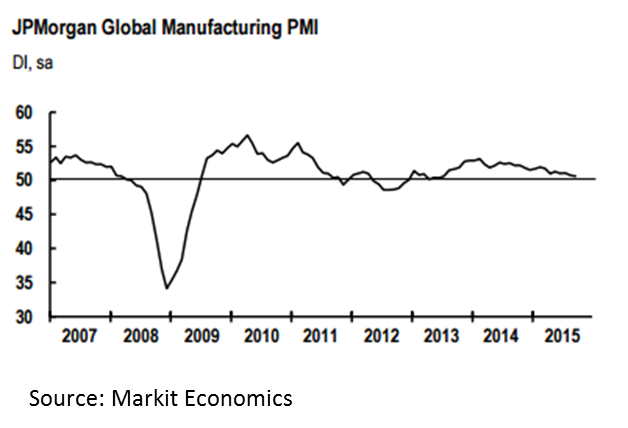

Global manufacturing has been trending flat to downward for most of 2015. The JP Morgan Global Manufacturing PMI continued that trend in September with a posting of 50.6 from 50.7 in August. The PMI was the lowest it has been since July and has averaged 50.8 for third quarter. Any reading over 50.0 is considered expansion.

The U.S. and European Union were the strongest contributors to PMI growth in September while Asian countries weakened. All nations in the Eurozone, except Greece, reported expansion last month. Greece and Brazil remain in severe contraction as third quarter closes.

Commenting on the survey, David Hensley, Director of Global Economic Coordination at J.P. Morgan, said: “The global PMI indicates the manufacturing sector remained in very low gear in September, due to sluggish final demand and ongoing inventory adjustments. These impacts are also starting to crossover into the labor market, leading global employment PMI to fall below 50 for the first time in over two years.”

North America

Markit’s U.S. Manufacturing PMI was at its second lowest level since October 2013 with a reading of 53.1 indicating a slower rate of expansion. Our North American neighbors, Canada and Mexico also registered slower manufacturing conditions in September. The Canadian PMI fell to 48.6, a moderate slip from 49.4 in August but the lowest reading in five-years. Canadian output, new business and employment all fell during September as weaker demand caused businesses to cut inventories and input buying. Mexico’s reading inched down 0.3 points to 52.4 as business conditions continued to be sluggish and higher input prices pressured margins.

Eurozone

The Eurozone manufacturing sector expansion slowed to a five month low as central bank stimulus and currency depreciation failed to spur growth momentum. The Eurozone PMI registered 52.0 from 52.3 in August and has averaged 52.3 for the past two quarters. Export orders continued to rise but at a slower rate due to weaker demand in emerging markets and uncertain global political and economic conditions. The Greece downturn is still severe but showing signs of easing.

Asia

The Caixin China General Manufacturing PMI registered 47.2 in September down fractionally from 47.3 in August. Operating conditions deteriorated at the quickest rate since March 2009. Production and new orders fell, driven by a steeper fall in new export business. Reduced production led firms to lower purchasing activity. Disappointing sales, said Caixin, led “to the strongest increase in stocks of finished goods for over three years.” Input costs and output charges both fell at sharper rates in September. “The industry has reached a crucial stage in its structural transformation. Tepid demand is a main factor behind the oversupply of manufacturing and why it has not recovered,” commented Dr. He Fan, Chief Economist at Caixin Insight Group.

Export orders fell in Vietnam, South Korea and Taiwan. Japan exports declined for the first time in 15 months with survey respondents citing lower trade volumes with China as the main factor behind the decrease. Japan continued expansion for the fifth consecutive month with a PMI of 51.0, down from 51.7 in August (the highest reading since January). Input prices continue to be challenged by weakness of the yen against the dollar.

Russia

The Russian manufacturing sector showed signs of stabilizing with a PMI of 49.1 up from 47.9 in August. Levels of output and new orders picked up in September as domestic demand firmed. Export orders, however, continued to fall for the 25th consecutive month. Input costs rose on the weakness of the rouble causing manufacturers to increase output charges.