Market Data

November 9, 2015

Federal Reserve Senior Loan Officer Opinion Survey on Bank Lending Practices

Written by Peter Wright

The Q4 2015 Senior Loan Officer Opinion Survey on Bank Lending Practices was released on November 2nd. This survey addresses changes in the standards and terms on, and demand for, bank loans to businesses and households on a quarterly basis and is based on the responses from 69 domestic banks and 23 U.S. branches and agencies of foreign banks. The Federal Reserve generally times the quarterly survey so that results are available for the January/February, April/May, August, and October/November meetings of the Federal Open Market Committee. The following is an abridged version of the Federal Reserve report followed by SMU comments and graphs.

![]()

Lending to Businesses

The October survey results indicated that, on balance, banks reported little change in lending standards for Commercial and Industrial (C&I) loans to firms of all sizes over the past three months. Among the modest number of banks that indicated they had changed their C&I lending standards, reports of tightening were more frequent, especially for large and middle-market borrowers. Banks continued to report having reduced costs of credit lines and narrowed loan spreads for both large and middle-market firms and smaller firms on net. A modest net fraction of banks also reported having eased the maturities on loans and credit lines for firms of all sizes. However, banks also reported that they increased premiums charged on riskier loans for large and middle-market firms on net. Meanwhile, all foreign respondents indicated that their C&I lending standards had remained basically unchanged. The domestic respondents that tightened either standards or terms on C&I loans over the past three months cited a less-favorable or more-uncertain economic outlook as well as worsening of industry specific problems as important reasons. Modest numbers of banks also attributed the tightening of loan terms to reduced tolerance for risk, decreased liquidity in the secondary market for these loans, and increased concerns about the effects of legislative changes, supervisory actions, or changes in accounting standards. In addition, the few banks that reported having eased either their standards or terms on C&I loans predominantly pointed to more-aggressive competition from other banks or nonbank lenders as an important reason.

On balance, demand for C&I loans was little changed during the third quarter. Those banks that reported having seen stronger demand cited as reasons for the strengthening a wide range of customers’ financing needs, particularly those related to accounts receivable, mergers or acquisitions, investment in plant or equipment, or inventories. Foreign bank respondents also reported that demand for C&I loans was little changed during the third quarter of 2015.

Commercial Real Estate (CRE) Lending: The majority of survey respondents indicated that their lending standards for CRE loans of all types had essentially remained unchanged relative to the second quarter. Regarding changes in demand, banks indicated that they had experienced stronger demand for all three types of CRE loans during the third quarter of 2015 on net. Similar to their domestic counterparts, foreign banks reported little change in their CRE lending standards, while they also indicated having experienced stronger demand for such loans on net.

Lending to Households

Residential Real Estate Lending: Modest net fractions of banks indicated that they had eased underwriting standards on loans eligible for purchase by the government-sponsored enterprises (known as GSE-eligible mortgage loans) and on “qualified” but not GSE-eligible mortgage loans. Meanwhile, the vast majority of banks continued to report that they do not extend home-purchase loans to subprime borrowers. On the demand side, modest net fractions of banks reported weaker demand across most categories of home-purchase loans. On balance, lending standards were reportedly little changed for home equity lines of credit, and demand for such loans strengthened.

Consumer Lending: A small net fraction of banks indicated that they were more willing to make consumer installment loans over the past three months. A few large banks reported having eased their standards for credit card loans, and several large banks indicated that they had eased standards for approving applications for auto loans. A modest net fractions of banks reported having eased lending standards on other types of consumer loans. Regarding loan terms on consumer loans, some large banks reported that, on net, they had increased credit card limits on new or existing credit card accounts. On balance, several survey respondents lengthened the maximum maturity of auto loans but left the remaining terms on such loans about unchanged. Very few banks reported changes on any of the terms on other consumer loans. Regarding demand for consumer loans, a modest net fractions of banks reported stronger demand for credit card loans and other consumer loans over the past three months. In contrast, demand for auto loans was reported to have remained about unchanged on net.

There is a huge amount of valuable data in this report which can be accessed here by those wishing to dig deeper.

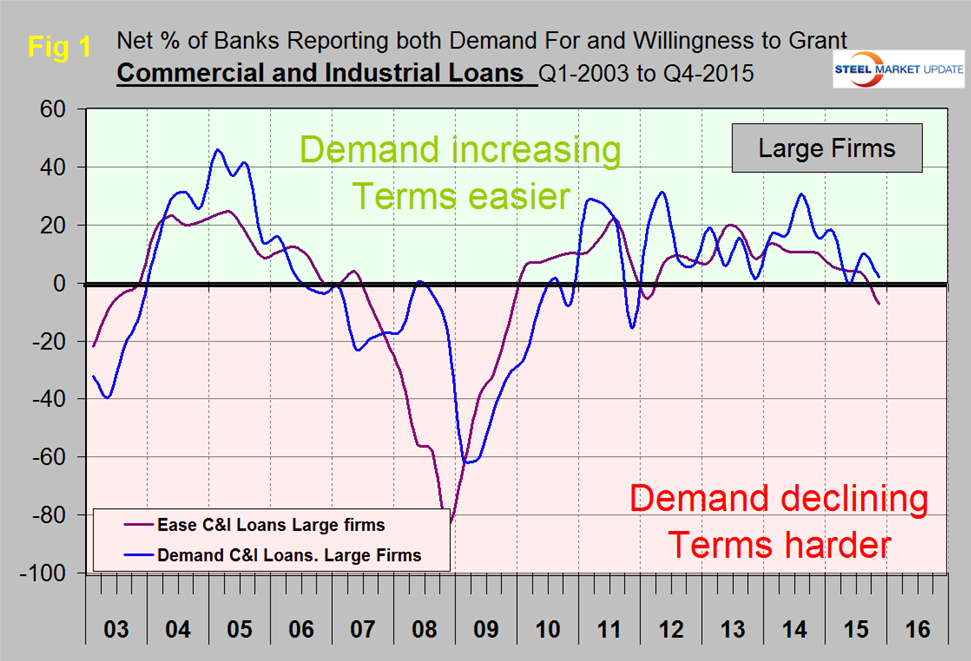

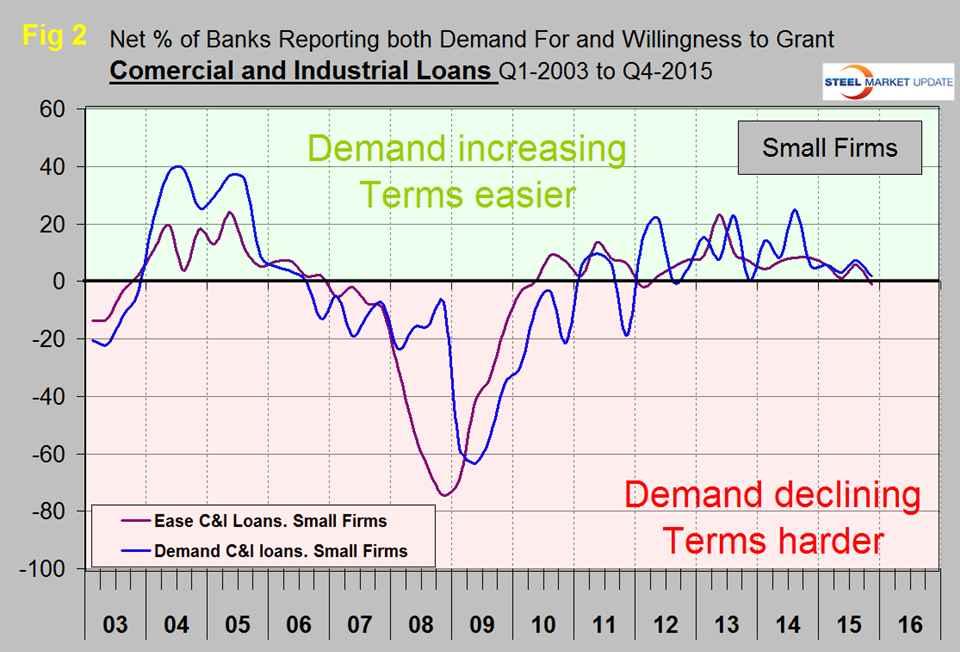

At SMU we extract and graph the major elements in the survey. Regarding loans to businesses, the October survey indicated that there was a small net increase in demand for commercial and industrial (C&I) loans from both large (>$50MM revenue) firms and small firms (<$50MM revenue) but less so than in the previous quarter (Figure 1 and Figure 2).

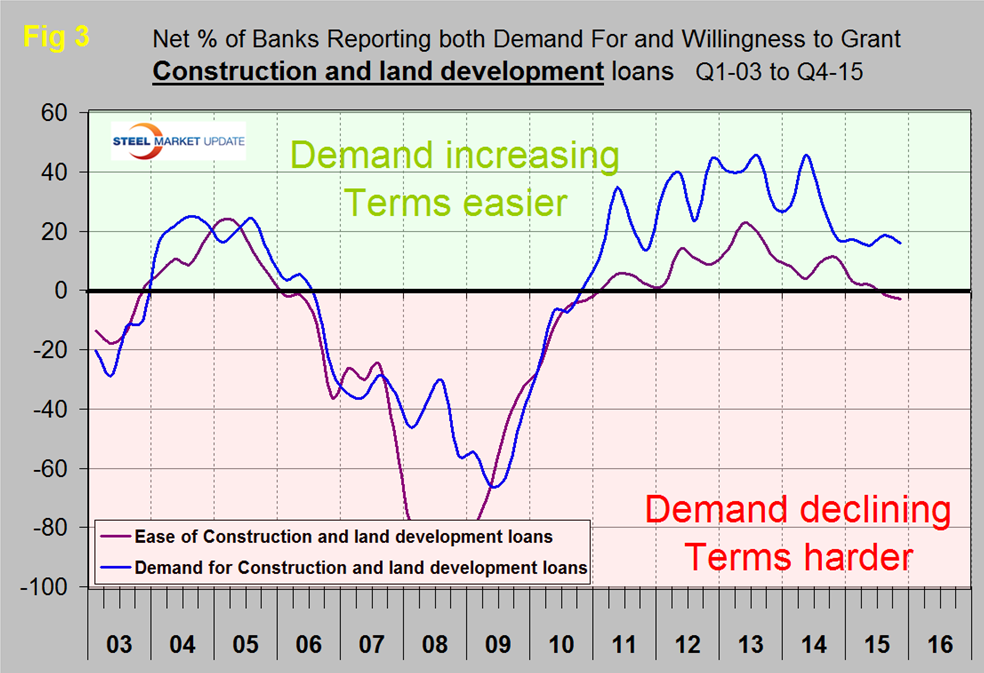

Terms tightened slightly to both large and small firms. What this means for example is that the number of banks reporting a tightening of standards to large and medium firms was 7.3 percent higher than the proportion reporting an easing of standards. In reality most banks are not changing their standards by much. There was almost no change in the number of banks reporting a change in demand for construction and land development loans, demand is at the bottom of the range that has existed since mid-2011. The net percentage of banks reporting a tightening of standards for construction loans increased from 1.4 percent to 3 percent (Figure 3) but again, in reality, most banks had no change.

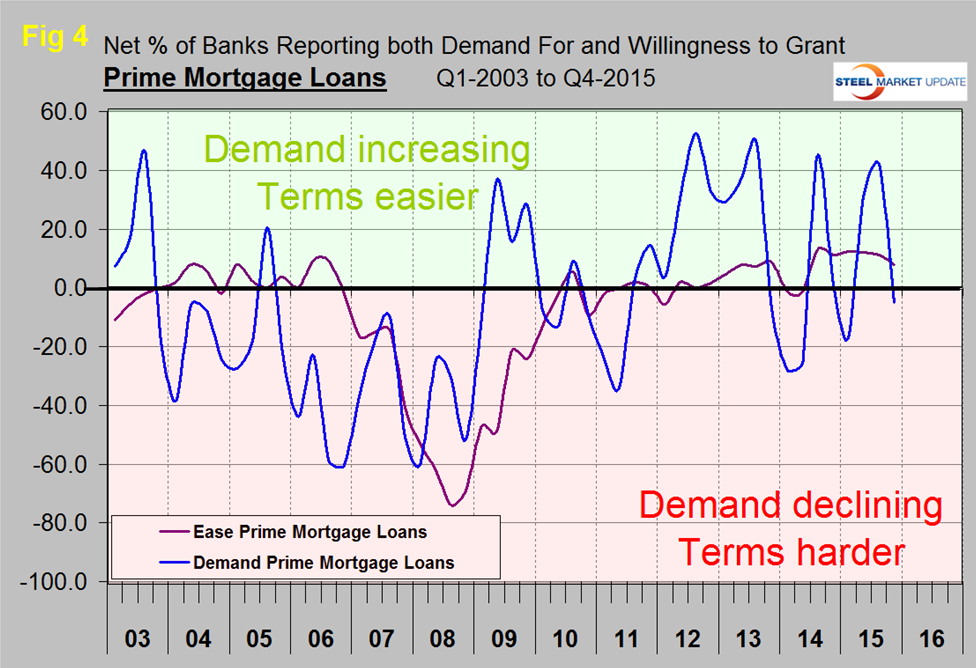

Demand for prime real-estate mortgages has been extremely erratic and seasonal for four years. In Q1 2015 a net 17.1 percent of banks reported a decline in demand, a net 31 percent reported an increase in Q2 2015, a net 41.9 percent reported an increase in demand in Q3 and a net 5.0 percent reported a decline in this latest survey. This level of variability is not mentioned or explained in the official write up by the Fed (Figure 4).

The implications of this report are reasonably good for the steel market. Loan demand is positive for all categories except home mortgages and that is clearly a seasonal effect. There has been a trend for less banks to be easing lending standards for C&I loans to large firms and for construction and land development loans in general but the net is still positive. A net 5.0 percent of banks reported more willingness to make consumer installment loans and a net 8.3 percent of banks have relaxed standards for credit card balances in the last three months. A net 14.0 percent of banks reported an increase in demand for credit card loans in the last quarter and a net 3.3 percent reported an increase in demand for auto loans.