Prices

November 15, 2015

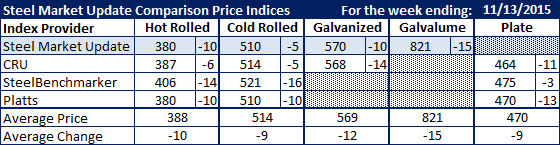

Comparison Price Indices: Never Ending Slide Continues

Written by John Packard

Flat rolled and plate prices continued to erode this past week according to the various steel indexes followed by Steel Market Update. With the exception of SteelBenchmarker (who tends to be behind the other indexes due to it only collecting market price intelligence twice per month), all of the indexes are showing hot rolled prices as being significantly below $400 per ton and moving toward a seven year price low for each of the indexes. Steel Market Update HRC average price is at its 7 year low point, last achieved in June 2009 at the height of the Great Recession.

As the week ended, SMU and Platts both had their HR index at $380 per ton ($19.00/cwt) followed by CRU at $387 per ton and then SteelBenchmarker which reported HR as being $406 per ton.

Cold rolled prices also fell on all four steel indexes as SMU and Platts moved their CR index to $510 per ton, CRU $514 and again SteelBenchmarker was the highest at $521 per ton.

Galvanized dropped to $568 and $570 per ton for .060” G90 on CRU and SMU respectively.

Galvalume .0142” AZ50, Grade 80 dropped $15 per ton to $821 per ton.

Plate prices dropped to $464 on CRU, $470 on Platts and $475 per ton on SteelBenchmarker.

FOB Points for each index:

SMU: Domestic Mill, East of the Rockies.

CRU: Midwest Mill, East of the Rockies.

SteelBenchmarker: Domestic Mill, East of the Mississippi.

Platts: Northern Indiana Domestic Mill.