Prices

February 9, 2016

SMU Price Ranges & Indices: Sideways 3, Up 1

Written by John Packard

Flat rolled steel prices remained relatively range bound over the past week with only one product, cold rolled, showing any movement other than sideways. While speaking to steel buyers around the country many of the discussions centered on lead times, demand and what will the mills do next regarding steel prices. The consensus of opinion seems to be that most buyers are still taking a very conservative approach to buying steel, demand is a question mark in some arenas and the majority of buyers don’t think the mills will push too hard and risk having another flood of foreign steel should the spread become too wide.

It seems like now is a time to reflect. There are a number of mills that are referencing lead times as “inquire,” at least on cold rolled and coated. Hot rolled continues to be the weakest product and will be for sometime to come. We are still hearing of HRC offers under $400 per ton with the southern mills a little more aggressive than those in the north.

US Steel and AK Steel are essentially out of the spot markets and their spot price offers are the highest out there. We are hearing that Nucor Berkeley and Hickman are inquire on cold rolled and coated as is SDI Butler. We will have more on lead times in Thursday evening’s issue of our newsletter.

In the meantime, here is how we see spot flat rolled prices this week (all prices shown are in net tons which are equal to 2,000 pounds):

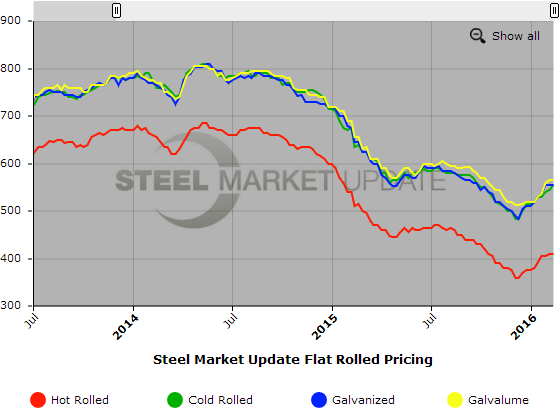

Hot Rolled Coil: SMU Range is $380-$440 per ton ($19.00/cwt- $22.00/cwt) with an average of $410 per ton ($20.50/cwt) FOB mill, east of the Rockies. Both the lower and upper ends of our range remained unchanged compared to one week ago. Our overall average did not change over last week. SMU price momentum for hot rolled steel has prices rising over the next 30 days.

Hot Rolled Lead Times: 2-5 weeks.

Cold Rolled Coil: SMU Range is $540-$570 per ton ($27.00/cwt- $28.50/cwt) with an average of $555 per ton ($27.75/cwt) FOB mill, east of the Rockies. The lower end of our range increased $20 per ton compared to last week while the upper end remained the same. Our overall average is up $10 per ton compared to one week ago. SMU price momentum for cold rolled steel is for prices to increase over the next 30 days.

Cold Rolled Lead Times: 5-8 weeks.

Galvanized Coil: SMU Base Price Range is $27.00/cwt-$28.50/cwt ($540-$570 per ton) with an average of $27.75/cwt ($555 per ton) FOB mill, east of the Rockies. Both the lower and upper ends of our range remained unchanged compared to one week ago. Our overall average remains the same as last week. Our price momentum on galvanized steel is for prices to move higher over the next 30 days.

Galvanized .060” G90 Benchmark: SMU Range is $600-$630 per net ton with an average of $615 per ton FOB mill, east of the Rockies.

Galvanized Lead Times: 4-9 weeks.

Galvalume Coil: SMU Base Price Range is $27.50/cwt-$29.00/cwt ($550-$580 per ton) with an average of $28.25/cwt ($565 per ton) FOB mill, east of the Rockies. Both the lower and upper ends of our range remained unchanged compared to last week. Our overall average is unchanged. Like the other flat rolled products mentioned above our price momentum for Galvalume is currently pointing towards an increase in prices over the next 30 days.

Galvalume .0142” AZ50, Grade 80 Benchmark: SMU Range is $841-$871 per net ton with an average of $856 per ton FOB mill, east of the Rockies.

Galvalume Lead Times: 5-9 weeks.

SMU Note: Below is a graphic showing our hot rolled, cold rolled, galvanized, and Galvalume price history. To use the graphs interactive capabilities, you must view it on our website here. If you need help navigating the website or need to know your login information, contact us at info@SteelMarketUpdate.com or by calling 800-432-3475.