Prices

March 1, 2016

SMU Price Ranges & Indices: Prices Adjusted Higher

Written by John Packard

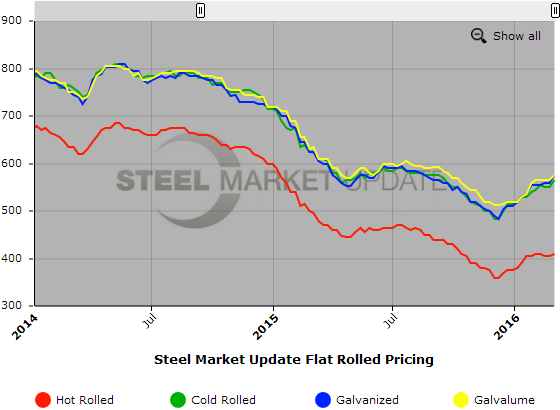

Spot flat rolled steel prices were adjusted higher by Steel Market Update based on the data being collected out of our ongoing flat rolled steel survey as well as through direct contact with steel buyers. We found a tight cluster of hot rolled offers in the $400 to $410 range. Our average increased due to an adjustment on the lower end of the range and our HRC index is now at $410 per ton. However, as we just mentioned if we were to produce our index on a weighted average it probably would have been closer to $405 than $410.

We will watch where prices go from here as SSAB and ArcelorMittal USA have come out with $30 per ton price increases on plate and sheet products. This includes hot rolled, cold rolled and coated products out of ArcelorMittal (plate and HR out of SSAB). We also expect the AD ruling on cold rolled to provide a shot in the arm for the domestic industry. Our Price Momentum Indicator continues to point toward higher prices over the next 30 days.

At this moment here is how we see spot flat rolled prices this week (all prices shown are in net tons which are equal to 2,000 pounds):

Hot Rolled Coil: SMU Range is $390-$430 per ton ($19.50/cwt- $21.50/cwt) with an average of $410 per ton ($20.50/cwt) FOB mill, east of the Rockies. The lower end of our range increased $10 per ton compared to one week ago while the upper end remained the same. Our overall average is up $5 per ton over last week. SMU price momentum for hot rolled steel has prices rising over the next 30 days.

Hot Rolled Lead Times: 2-5 weeks.

Cold Rolled Coil: SMU Range is $550-$580 per ton ($27.50/cwt- $29.00/cwt) with an average of $565 per ton ($28.25/cwt) FOB mill, east of the Rockies. The lower end of our range increased $30 per ton compared to last week while the upper end remained unchanged. Our overall average increased $15 per ton over one week ago. SMU price momentum for cold rolled steel is for prices to increase over the next 30 days.

Cold Rolled Lead Times: 5-8 weeks.

Galvanized Coil: SMU Base Price Range is $28.00/cwt-$29.50/cwt ($560-$590 per ton) with an average of $28.75/cwt ($575 per ton) FOB mill, east of the Rockies. The lower end of our range increased $20 per ton compared to one week ago while the upper end increased $10 per ton. Our overall average is up $15 per ton over last week. Our price momentum on galvanized steel is for prices to move higher over the next 30 days.

Galvanized .060” G90 Benchmark: SMU Range is $620-$650 per net ton with an average of $635 per ton FOB mill, east of the Rockies.

Galvanized Lead Times: 4-9 weeks.

Galvalume Coil: SMU Base Price Range is $28.00/cwt-$29.50/cwt ($560-$590 per ton) with an average of $28.75/cwt ($575 per ton) FOB mill, east of the Rockies. The lower end of our range increased $10 per ton compared to last week as did the upper end remained of our range. Our overall average increased $10 per ton over one week ago. Like the other flat rolled products mentioned above our price momentum for Galvalume is currently pointing towards an increase in prices over the next 30 days.

Galvalume .0142” AZ50, Grade 80 Benchmark: SMU Range is $851-$881 per net ton with an average of $866 per ton FOB mill, east of the Rockies.

Galvalume Lead Times: 5-9 weeks.

SMU Note: Below is a graphic showing our hot rolled, cold rolled, galvanized, and Galvalume price history. To use the graphs interactive capabilities, you must view it on our website here. If you need help navigating the website or need to know your login information, contact us at info@SteelMarketUpdate.com or by calling 800-432-3475.