Market Data

April 9, 2017

Net Job Creation by Industry through March 2017

Written by Peter Wright

The Bureau of Labor Statistics (BLS) employment report released Friday was another example of why we should not be fixated on a single month’s result. Month on month this was a dismal report with a net increase of only 98,000 jobs, well below analyst’s expectations. To make matters worse, January and February were revised down by a total of 38,000 jobs. Using a three month moving average (3MMA), the result for March was 178,000, down only 20,000 from February and exactly the same as January. The average monthly increase in the six months of Q4 2016 and Q1 2017 was 177,000. Moody’s concluded that the spring weather played a significant role in the last three months and commented, “March payroll gains came in with a thud. A weaker pace was expected following two strong months that were pumped up by the mild winter weather, but the downshift in March was greater than forecast. The shift forward to the beginning of the year of hiring that would have occurred in March was compounded by March’s unusually harsh weather, which further depressed weather-dependent industries.”

Figure 1 shows the 3MMA of the number of jobs created monthly as the brown bars since 2000. These numbers are seasonally adjusted by the BLS.

In order to examine if any seasonality is left in the data after adjustment we have developed Figure 2. In the seven years since and including 2011, job creation in March has been up by 2.0 percent. This year March was down by 55.0 percent which is another way of expressing how far out of line this result was.

Total non-farm payrolls are now 7,493,000 more than they were at the pre-recession high of March 2008. November 2014 was the first month for total non-farm employment to exceed 140 million. In March employment was almost 146 million. The BLS reported that the average workweek for all employees on private non-farm payrolls was unchanged at 34.3 hours in March. In manufacturing, the workweek edged down by 0.2 hour to 40.6 hours, and overtime declined by 0.1 hour to 3.2 hours. The average workweek for production and non-supervisory employees on private non-farm payrolls edged down by 0.1 hour to 33.5 hours. In March, average hourly earnings for all employees on private non-farm payrolls increased by 5 cents to $26.14, following a 7-cent increase in February. Over the year, average hourly earnings have risen by 68 cents, or 2.7 percent. In manufacturing, the workweek was unchanged at 40.8 hours, and overtime remained at 3.3 hours.

Table 1 slices total employment into service and goods producing industries and then into private and government employees.

Total employment equals the sum of private and government employees; it also equals the sum of goods producing and service employees. Most of the goods producing employees work in manufacturing and construction and the components of these two sectors that we consider to be of most relevance to steel people are broken out in Table 1. In March, 89,000 jobs were created in the private sector and government gained 9,000. The Federal government lost 1,000 as local governments gained 9,000 and state governments gained 1,000. Since March 2010, the employment low point, private employers have added 16,283,000 jobs as government has shed 158,000. In March service industries expanded by 70,000 as goods producing industries driven by both construction and manufacturing expanded by 28,000. Since March 2010, service industries have added 13,783,000 and goods producing 2,342,000 positions. This is part of the reason why wage growth has been slow since the recession as service industries on average pay less than goods producing such as manufacturing. As total employment was revised down by 38,000 jobs in January and February, goods producing was revised up by 4,000 jobs.

In March, manufacturing gained 11,000 positions for a total of 49,000 in the first quarter and was 0.3 percent higher than the same month in 2016 and 0.6 percent higher than in March 2015. Table 1 shows that primary metals had positive growth of almost 1 percent in the last three months. Transportation equipment including motor vehicles lost jobs in February but picked back up in March. Trucking was very strong in both February and March. Oil and gas extraction gained 1,800 jobs in the preliminary March result which was 1.0 percent. Note the subcomponents of both manufacturing and construction shown in Table 1 don’t add up to the total because we have only included those that we think have most relevance to the steel industry.

Construction was reported to have gained 6,000 jobs in March and is up by 177,000 in the last 12 months or 2.6 percent. Some of the major construction sub categories are routinely reported one month in arrears which distorts the data in Table 1. These include, industrial buildings, commercial buildings and highways and streets. Construction has added 1,382,000 jobs and manufacturing 939,000 since the recessionary employment low point in February 2010 (Figure 3).

Construction has leapt ahead of manufacturing as a job creator but the growth of construction productivity is very low (or non-existent), in contrast to manufacturing where it is very high. The difference is the difficulty of automating construction jobs.

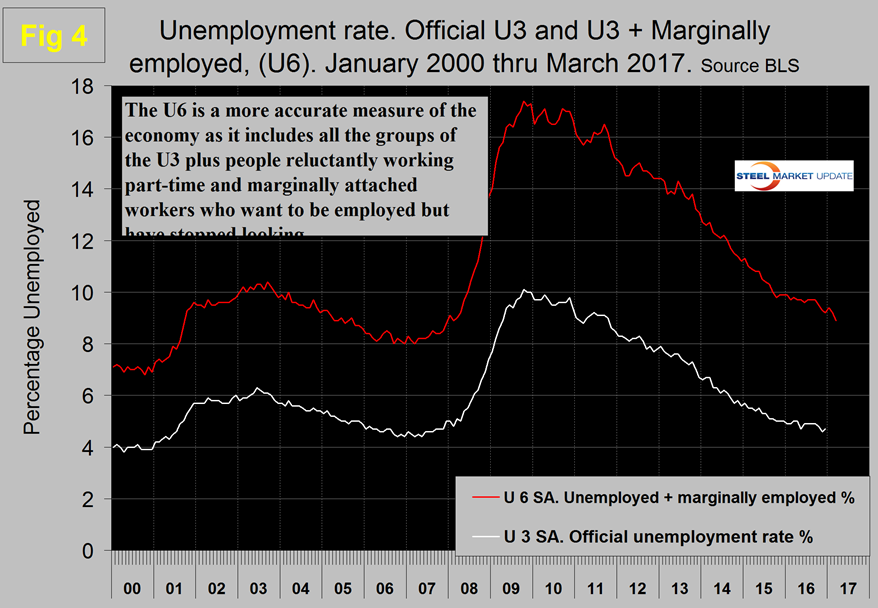

The official unemployment rate, U3, reported in the BLS’s Household survey (see explanation below) came in at 4.5 percent which was down from 5.0 percent in March last year. This number doesn’t take into account those who have stopped looking. The more comprehensive U6 unemployment rate was down from 9.8 percent in March last year to 8.9 percent in this latest report (Figure 4).

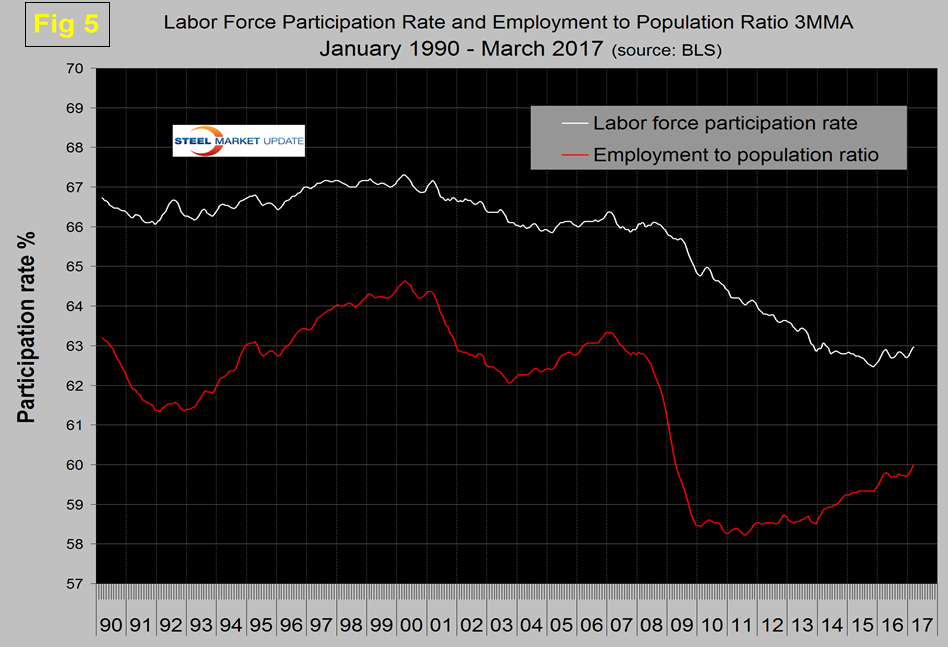

U6 includes workers working part time who desire full time work and people who want to work but are so discouraged that they have stopped looking. The differential between these rates was usually less than 4 percent before the recession but is still 4.4 percent. It has been estimated that the economy needs to create about 150,000 jobs per month to keep up with population growth. In the last five quarters the average monthly job creation has been 185,000 so the impact on unemployment has been about 35,000/month. The employment participation rate at 63 percent in March was exactly the same as March last year and not much better than the 62.7 percent reported for March 2015. We’re not sure what this is a percentage “of” because of the multiple descriptions of the labor pool. Another measure is the number employed as a percentage of the population which we think is much more definitive. In March this measure was 60.1 percent up from 59.9 percent in March last year and from 59.3 percent in March 2015. Until a year ago when it stalled, there was a gradual improvement in employment to population ratio since late 2011. Figure 5 shows both measures on one graph.

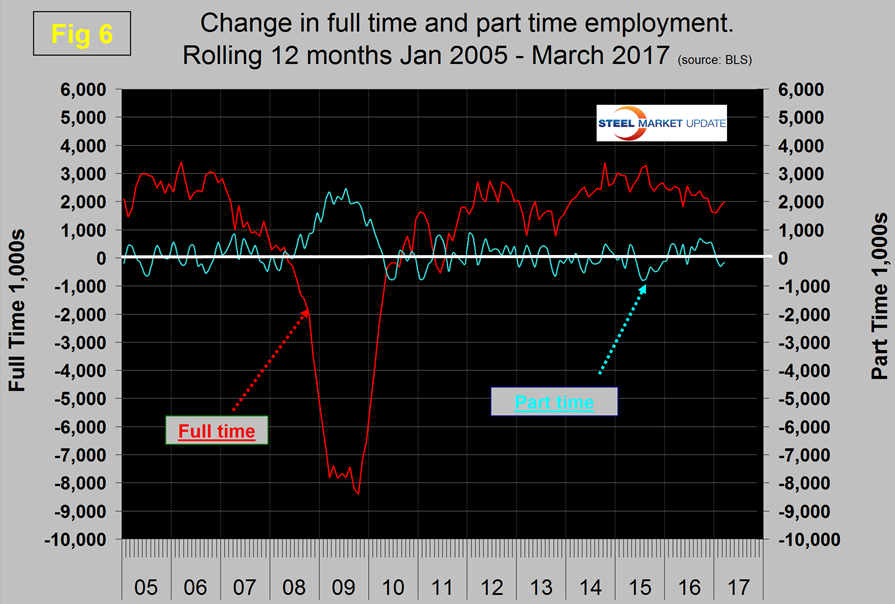

In the 27 months since and including January 2015 there has been an increase of 5,573,000 full time and 97,000 part time jobs. Figure 6 shows the rolling 12 month total change in both part time and full time employment.

Frequently in the press we read that a large part of job creation is in part time employment which in some months is true, but the part time numbers are extremely volatile. This data comes from the Household survey and part time is defined as < 35 hours per week. Because the full time/part time data comes from the Household survey and the headline job creation number comes from the Establishment survey, the two cannot be compared in any particular month. To overcome the volatility in the part time numbers we have to look at longer time periods than a month or even a quarter which is why we look at a rolling 12 months for this component of the employment picture shown in Figure 6.

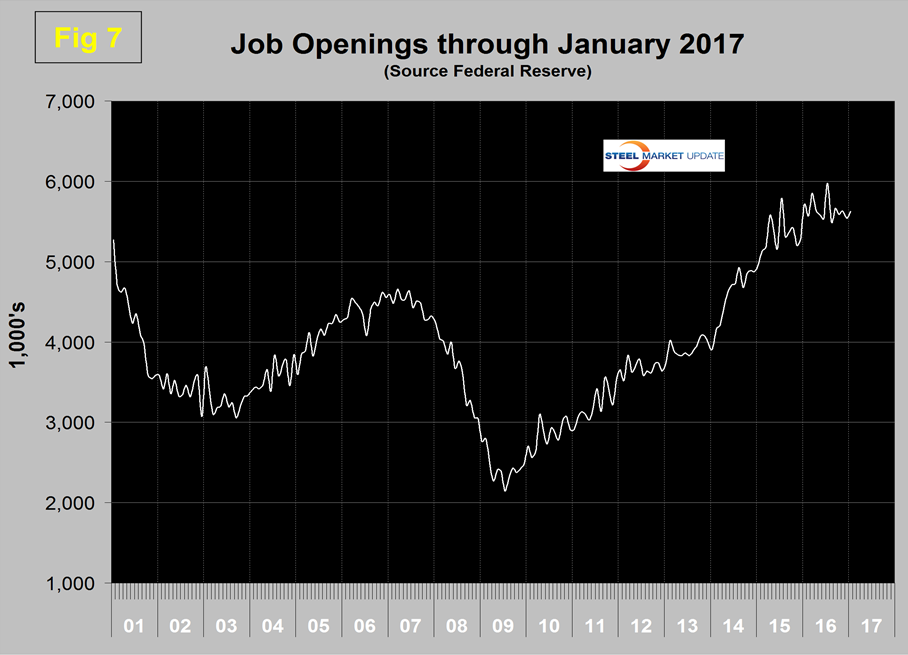

The job openings report known as JOLTS is reported on about the 10th of the month by the Federal Reserve and is over a month in arrears. Figure 7 shows the history of unfilled job openings through January when openings stood at 5,626,000 not far off the all-time high of 5,852,000 in March last year. There has been an improving trend since mid 2009.

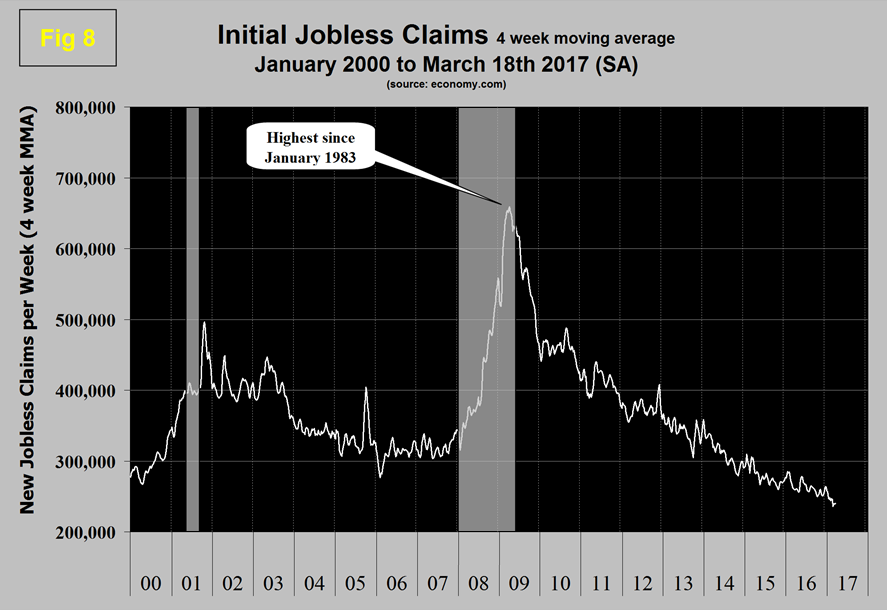

Initial claims for unemployment insurance, reported weekly by the Department of Labor have continued their downward drift this year and in w /e March 18th were 258,000 with a four week moving average of 240,000. This marks the longest streak since 1973 of initial claims below 300,000. (Figure 8). The result for w/e November 12th at 233,000 was the lowest since April 1974.

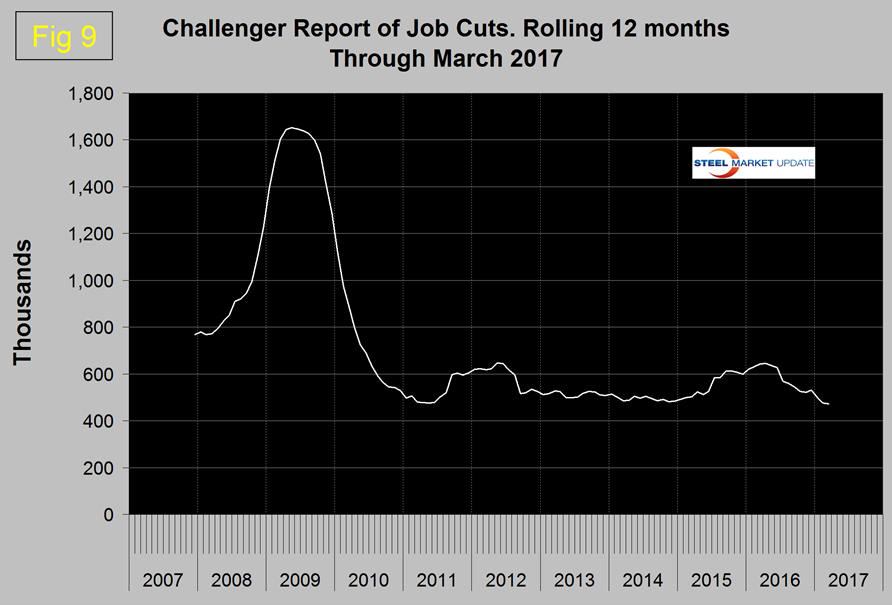

The last piece of the employment puzzle that we examine is the Challenger report which measures job cuts monthly (Figure 9).

This data also tends to be quite erratic therefore again we examine a rolling 12 months and can see that job cuts decreased for most of 2016 and continued their downward trend in 2017.

SMU Comment: Overall we think the employment situation is very good and has been described as “full” by some analysts. March was the 77th consecutive month of job growth and in the last 15 months, 7 have exceeded 200,000 jobs created per month. The road hauling sector has gained 31,500 jobs in the last three quarters which we regard as a general economic indicator. Job losses in the oil fields have halted. The results for manufacturing and construction are sign posts for steel sales activity. In the big picture, layoffs are historically low and job openings are close to all-time highs therefore the year has started off well.

Explanation: On the first Friday of each month the Bureau of Labor Statistics releases the employment data for the previous month. Data is available at www.bls.gov. The BLS reports on the results of two surveys. The Establishment survey reports the actual number employed by industry. The Household survey reports on the unemployment rate, participation rate, earnings, average workweek, the breakout into full time and part time workers and lots more details describing the age breakdown of the unemployed, reasons for and duration of unemployment. At SMU we track the job creation numbers by many different categories. The BLS data base is a reality check for other economic data streams such as manufacturing and construction and we include the net job creation figures for those two sectors in our “Key Indicators” report. It is easy to drill down into the BLS data base to obtain employment data for many sub sectors of the economy. For example, among hundreds of sub-indexes are truck transportation, auto production and primary metals production. The important point about each of these hundreds of data streams is in which direction they are headed. Whenever possible we at SMU try to track three separate data sources for a given steel related sector of the economy. We believe this gives a reasonable picture of market direction. The BLS data is one of the most important sources of fine grained economic data that we use in our analyses. The States also collect their own employment numbers independently of the BLS. The compiled state data compares well with the federal data. Every three months SMU examines the state data and provides a regional report which indicates strength of weakness on a geographic basis. Reports by individual state can be produced on request.