Market Data

August 27, 2017

China’s Still Driving Global Steel Production

Written by Peter Wright

In June and July, China registered its highest share of global steel production ever, according to World Steel Association data with analysis by Steel Market Update.

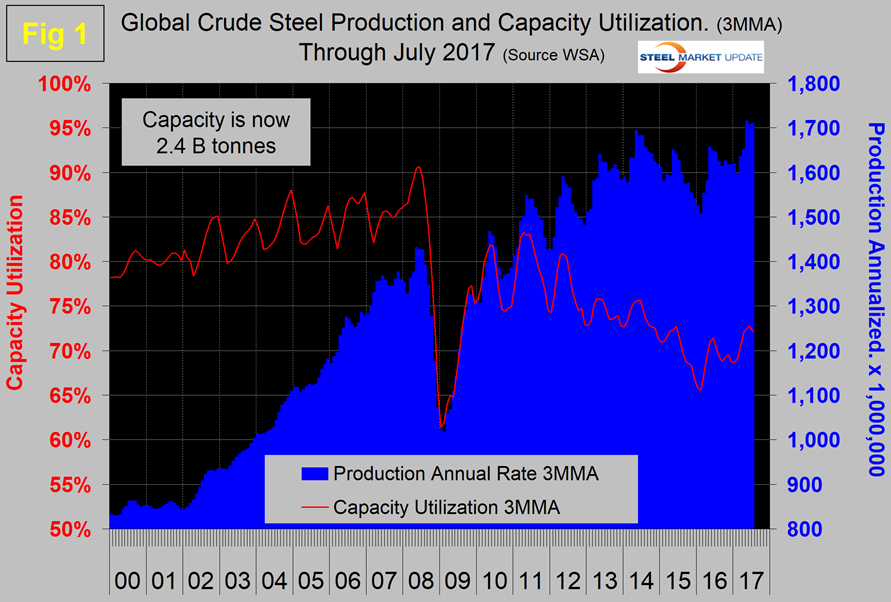

Global crude steel production in the month of July totaled 143,245,000 metric tons, up from 141,331,000 metric tons in June. Capacity utilization was 71.7 percent, down from 73.0 percent in June. Capacity utilization went down as production went up because there was one more day in July and tons per day production declined slightly in July. The three-month moving averages (3MMA) that we prefer to use were 142,584,000 metric tons and 72.1 percent, respectively. Capacity is 2.4 billion metric tons per year. Figure 1 shows monthly production and capacity utilization since January 2000.

On a tons-per-day basis, production in July was 4.621 million metric tons with a 3MMA of 4.650 million metric tons, which was down slightly from the all-time high in June of 4.690 million metric tons. In three months through July, production increased by 3.9 percent year over year. On a 3MMA basis, capacity utilization had an erratically downward trajectory from mid-2011 through early 2016 when it bottomed out at 65.5 percent in February. A turnaround seems to be developing as the June and July capacity utilization rates were the highest since early 2015. Last October, the OECD’s steel committee estimated that global capacity would increase by almost 58 million metric tons per year between 2016 and 2018, bringing the total to 2.43 billion tons.

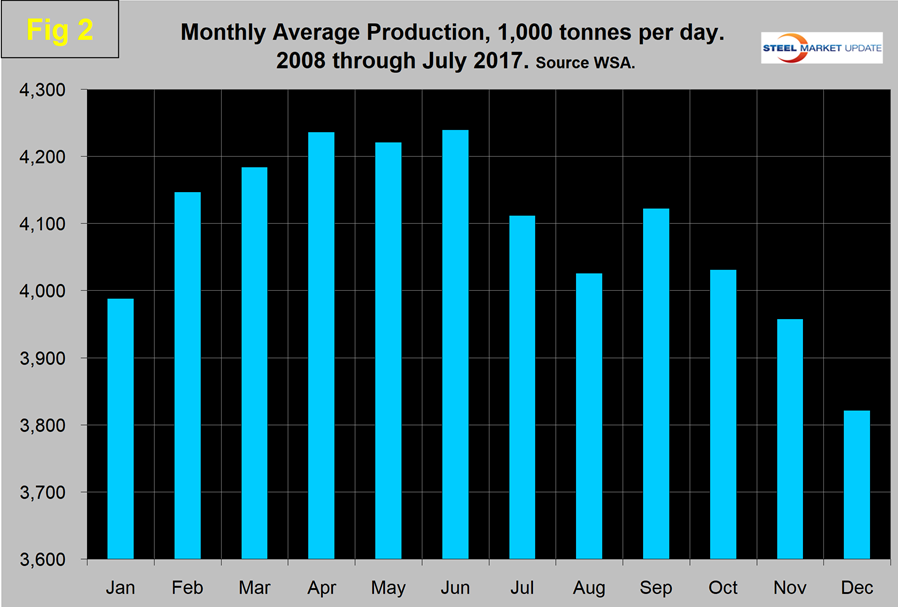

As we dig deeper into what is going on, we start with seasonality. Global production has peaked in the early summer for the last seven years with April and June on average having the highest volume. Figure 2 shows the average metric tons per day production for each month since 2008.

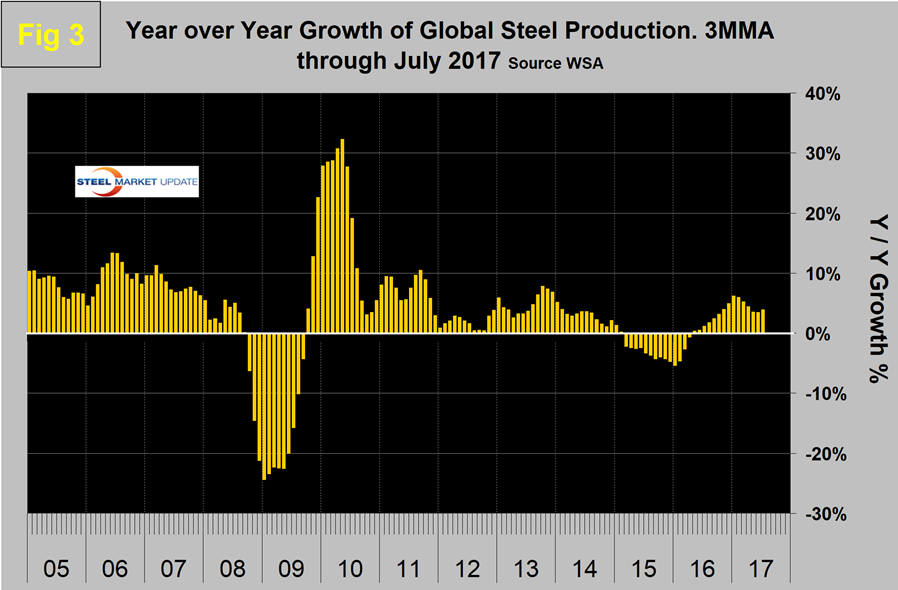

In those 10 years, on average, July has been down by 3.02 percent; this year July was down by 1.92 percent. Figure 3 shows the monthly year-over-year growth rate on a 3MMA basis since January 2005.

Production began to contract in March 2015, and the contraction accelerated through January 2016 when it reached negative 5.6 percent. Growth improved every month through January this year when it reached positive 6.2 percent. Growth slowed to 3.5 percent in May and June, then recovered slightly to 3.9 percent in July. In the 13 months through April, China’s growth rate was lower than the rest of the world. That changed in the three months through July when China began to pull away again. In July, China expanded by 6.0 percent, the world as a whole grew by 3.9 percent, and the world excluding China expanded by only 1.8 percent. In June, China produced 51.8 percent of the global total and 51.7 percent in July. These were the highest ever values for China’s global production share.

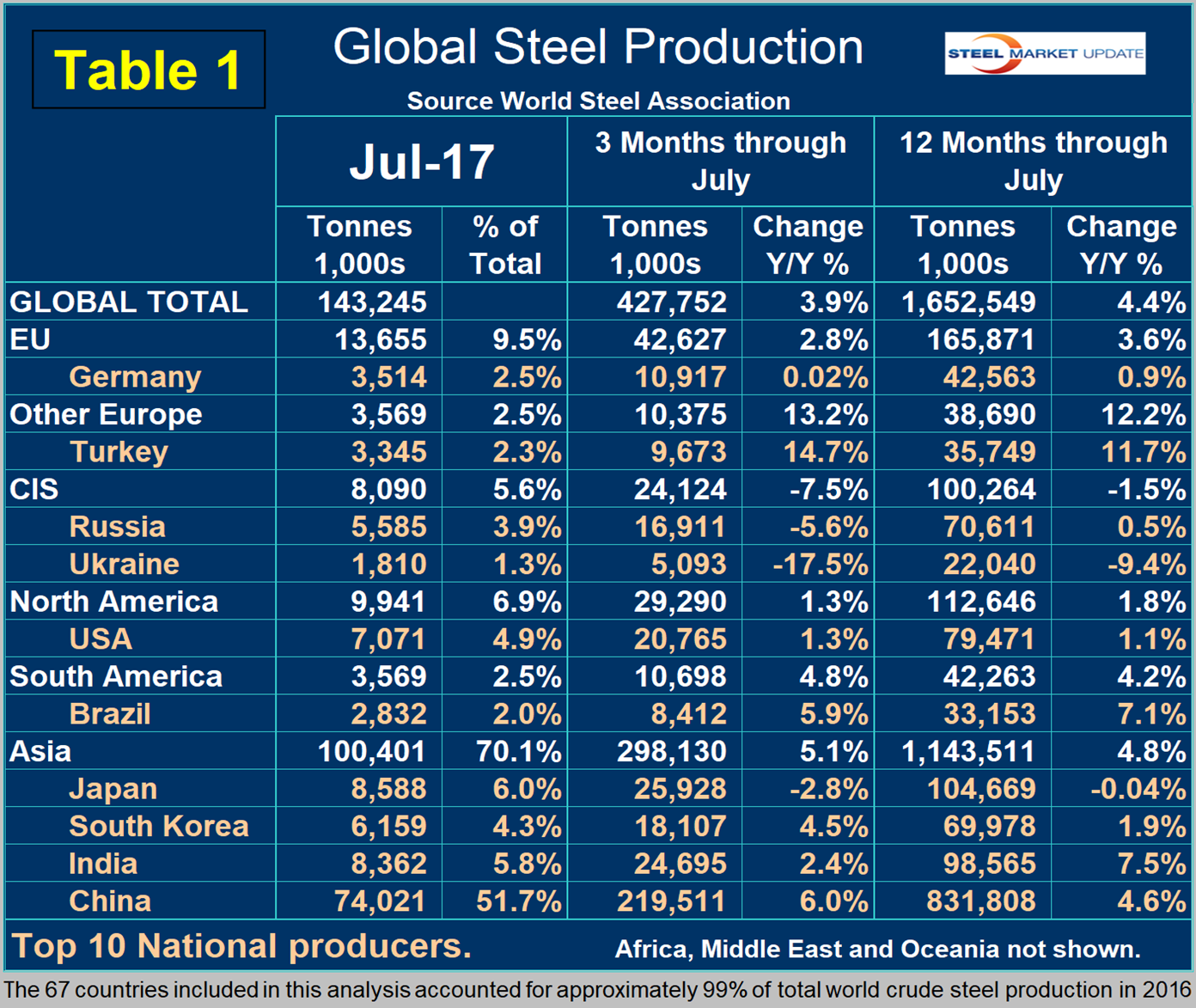

Table 1 shows global production broken down into regions, the production of the top 10 nations in the single month of July and their share of the global total. It also shows the latest three months’ and 12 months’ production through July with year-over-year growth rates for each period. Regions are shown in white font and individual nations in beige.

The world as a whole had positive growth of 3.9 percent in three months and 4.4 percent in 12 months through July. If the three-month growth rate exceeds the 12-month rate, we interpret this to be a sign of positive momentum, which was the case for the 16 months through May. In June and July, momentum for the world as a whole became negative, but for China was positive. Vietnam doesn’t appear in Table 1 and wasn’t even recognized as a producer by the World Steel Association until January 2016. Vietnam has seen its production grow from 407,000 tons in January last year to 888,000 tons in March this year. This may be another piece of the puzzle that describes the re-processing and export of Chinese hot rolled coil. In Q1 this year, Vietnam imported HRC at an annual rate of 11 million tons, which was by far the highest of all importing nations, nearly all from China.

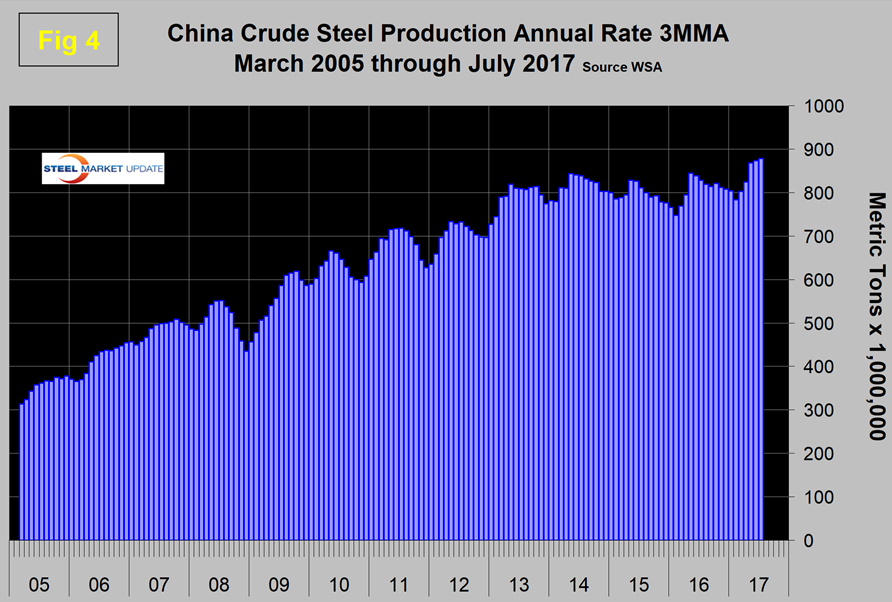

Figure 4 shows China’s production since 2005 and Figure 5 shows the year-over-year growth.

China’s production after slowing for 13 straight months year over year returned to positive growth each month in May 2016 through July this year on a 3MMA basis. The slowdown in Chinese steel production that they have been promising is not happening. However, Platts reported on Aug. 9 that the mandatory closure of induction furnaces in China, together with stronger domestic demand for rebar, had resulted in a 74 percent reduction in exports of long products. Total steel exports in 2017 are tracking at 75 million metric tons per year, down from 110 million last year. That’s 35 million metric tons of steel that the world won’t have to compete with in 2017.

Table 1 shows that in three months through July year over year, every region except the CIS had positive growth. North America was up by 1.3 percent. Within North America the U.S. was also up by 1.3 percent, Canada was down by 1.0 percent and Mexico up by 3.1 percent. In the 1st half of 2017, Mexico produced 54.8 percent more steel than Canada. Other Europe led by Turkey had the highest growth rate in three months through July year over year. Asia as a whole was up by 5.1 percent.

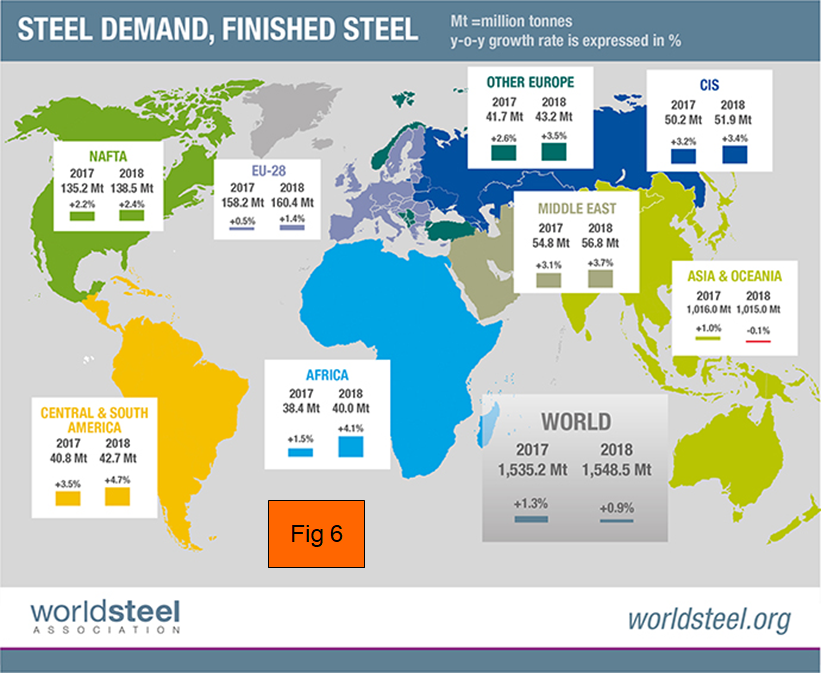

In previous monthly updates, we have included the April 2017 version of the World Steel Association Short Range Outlook for apparent steel consumption in 2017 and 2018, below. We will continue to include this as until the next update is released in October.

The April forecast was for global growth of 1.3 percent and 0.9 percent in 2017 and 2018, respectively. North American steel consumption is forecast to grow by 2.2 percent and 2.4 percent. Surprisingly, Asia is forecast to contract next year. Note this forecast is steel consumption, not crude steel production, which is the main thrust of what you are reading now.

Last month, the IMF took another look at their World Economic Outlook and made the following comments. The WEO will be formally updated in October. “The pickup in global growth anticipated in the April World Economic Outlook remains on track, with global output projected to grow by 3.5 percent in 2017 and 3.6 percent in 2018. The unchanged global growth projections mask somewhat different contributions at the country level. U.S. growth projections are lower than in April, primarily reflecting the assumption that fiscal policy will be less expansionary going forward than previously anticipated. Growth has been revised up for Japan and especially the euro area, where positive surprises to activity in late 2016 and early 2017 point to solid momentum. China’s growth projections have also been revised up, reflecting a strong first quarter of 2017 and expectations of continued fiscal support. Inflation in advanced economies remains subdued and generally below targets; it has also been declining in several emerging economies, such as Brazil, India, and Russia.”

SMU Comment: Spending on transportation infrastructure is projected by the IMF to quadruple by 2035 in India, China and other parts of emerging Asia, as well as in sub-Saharan Africa. This investment is highly steel-intensive, therefore there is a light at the end of the tunnel as far as steelmaking overcapacity is concerned, but it’s a long tunnel. Prior to this July data, it looked as though pressure from China might be abating, but based on the recent results, that situation may be reversing.