Market Data

September 21, 2017

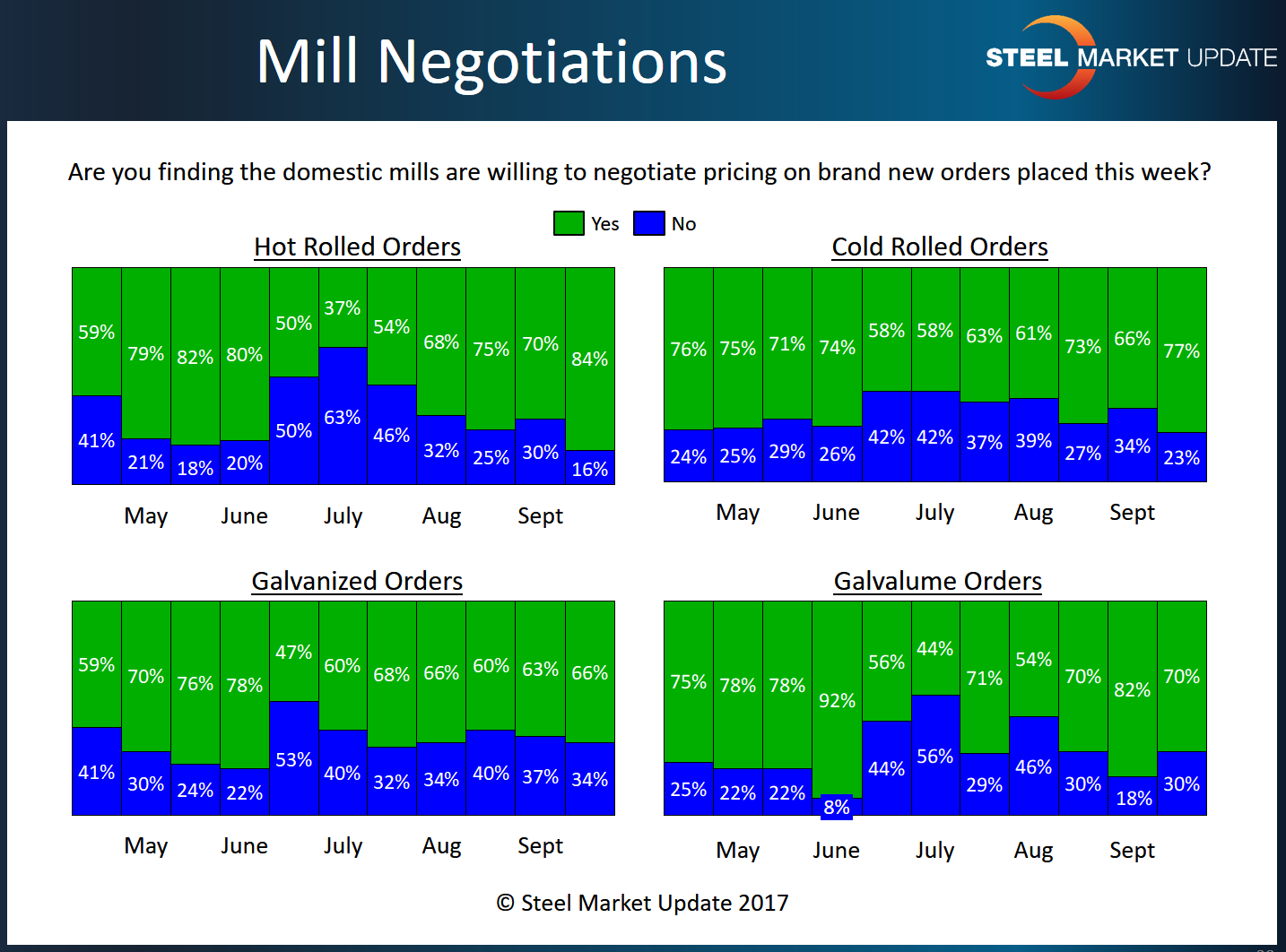

Steel Mill Negotiations: More Willingness to Talk Price

Written by Tim Triplett

Mills are even more open to price discussions than they were a couple weeks ago, report steel buyers and sellers who replied to Steel Market Update’s latest flat rolled market trends questionnaire.

More than 100 executives responded to this week’s questionnaire. Steel buyers’ perceptions of their suppliers’ attitudes offer a snapshot of how steel mills are currently handling price negotiations.

Nearly half the respondents agreed that order books are weaker than expected and mills are open to price discussions. That percentage represents a significant jump from the 41 percent two weeks ago and 33 percent a month ago who found mills willing to negotiate.

Another 46 percent of buyers said some mills are flexible and others are firm, about the usual mix. But two weeks ago, 9 percent of respondents said they found mills unwilling to talk price; that figure declines to just 4 percent in the latest report.

By product category, 84 percent of manufacturing and service center respondents saw mills willing to negotiate hot roll orders, up significantly from 70 percent in the last report. In cold roll, the percentage jumped to 77 percent who found the price negotiable, up markedly from 66 percent two weeks ago. Galvanized saw a slight increase to 66 percent from 63 percent, while Galvalume declined to 70 percent from 82 percent, indicating less willingness to talk price on coated products.

Comments from buyers show no clear consensus: “The mills are reluctant to deal,” said one service center executive. “It depends on the mill,” said a manufacturer. “Lead time is relatively short at around 3 to 4 weeks. The upcoming planned outages should lend support to the mills.” Said a trader: “It seems like the spot market is soft and mill lead times are extremely short for some products, like HRC at West Coast mills.” Added another manufacturer: “I think order books are weak and the mills are controlling the pricing based on the foreign steel situation [import restrictions], as well as the hurricane and floods.”

Note: SMU surveys active steel buyers twice each month to gauge the willingness of their steel suppliers to negotiate pricing. The results reflect current steel demand and changing spot pricing trends. SMU provides our members with a number of ways to interact with current and historical data. To see an interactive history of our Steel Mill Negotiations data, visit our website here.