Market Data

March 3, 2018

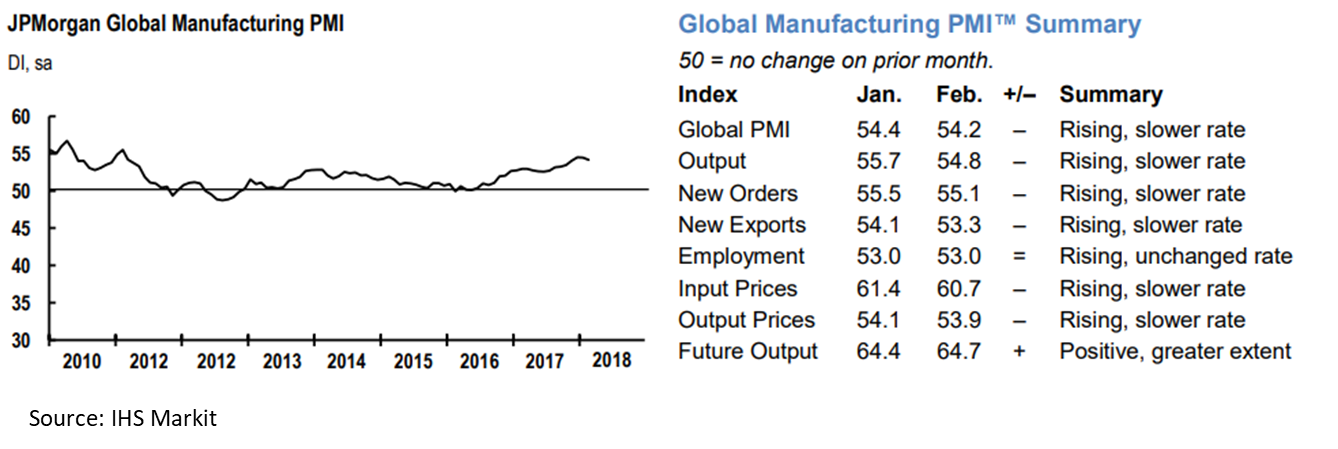

Global Manufacturing PMI: Solid But Slower

Written by Sandy Williams

Global manufacturing expanded at a solid pace in February, according to the J.P.Morgan Global Manufacturing PMI. The composite PMI inched downward for the second month to 54.2, indicating solid but slower growth.

Industrial nations saw growth rates decelerate somewhat in February including the U.S., Eurozone, Japan and the UK. Improvement of manufacturing conditions was brisker in China, Brazil, Australia, and Vietnam.

New orders and manufacturing production rose during the month although at a slower rate. International trade saw an uptick as new export business improved for the 19th consecutive month.

“The global manufacturing sector continued to achieve a solid pace of expansion in February, according to the latest PMI data,” said David Hensley, Director of Global Economic Coordination at J.P.Morgan. “Nonetheless, the PMI, along with the latest data on production and expenditures, indicate that goods-sector expansion is moderating from the red-hot pace of late 2017.”

Eurozone manufacturing continues to expand at a robust pace, says IHS Markit. The IHS Markit Eurozone Manufacturing PMI dipped one point to 58.6 in February. Growth was noted across all sectors. Netherlands led the PMI ratings at a record high 63.4, followed by Germany at 60.6 and Austria at 59.2. All of the nations within the Eurozone were well above the 50 no-change market. Production increased in February, but there are signs that output growth may be easing. New orders and new export business rose, but at a weaker pace last month. Input price inflation eased from the January high, but remained elevated. Output charges rose at the quickest pace in seven years, noted IHS Markit.

“There are signs, however, that growth could cool further in coming months, “said IHS Markit Chief Business Economist Chris Williamson. “ A slowdown in growth of new export order inflows to an 11-month low suggests that the appreciation of the euro may be starting to curb export sales. Job creation, while still among the highest seen in the 20-year survey history, has meanwhile moderated as a result of the slower inflows of orders, adding to suspicions that the manufacturing growth peak is behind us.”

Williamson added that capacity constraints, labor shortages and supply chain pressure may be contributing to the slowdown.

China manufacturing conditions improved in February with new orders and production expanding modestly and backlogs growing. The Caixin China General Manufacturing PMI crept to 51.6 from 51.5 in January. Input prices rose sharply and delivery times for raw materials to manufacturers increased with delays attributed to poor weather. Selling prices increased as a result. Firms were optimistic about future demand and new product launches.

“For now, the durability of the Chinese economy will persist,” commented Dr. Zhengsheng Zhong, Director of Macroeconomic Analysis at CEBM Group. “Looking ahead, whether demand generated from the beginning of work in March will gain strength will be key in determining China’s economic direction for 2018.”

The IHS Markit Russia Manufacturing PMI fell to its lowest level since July 2016, posting a score of 50.2 in February. Demand conditions were described as “fragile” with growth in new orders at the weakest level in eight months. Firms reported an uptick in new export orders, which jumped at the fastest pace since November 2011 giving rise to future optimism. Pricing pressure was subdued in February, but purchasing activity grew only marginally, causing contraction in inventories. Employment levels fell as did backlogs.

The South Korea Nikkei Manufacturing PMI dipped to 50.3 in February from 50.7 in January. New business softened resulting in a clearing of backlogs and higher inventories of finished goods. Raw material shortages, longer delivery times, and higher labor costs contributed to higher input costs, which were passed along in selling prices. New export orders rose in February, particularly from Australia, China and the U.S. Korean firms expressed confidence in future activity, looking forward to new production launches and economic growth.

Canada manufacturing production slowed in February to a PMI reading of 55.6 from January’s six-month peak. Export orders rose at the strongest rate since November 2014 mostly due to sales to U.S. clients, as well as a stronger global economy. Increased demand caused supply chain delays and greater backlogs. Manufacturers reported ELD regulations in the U.S. added to trucking capacity issues. Hiring activity increased as firms sought to meet production demands. Continued elevated input prices and rising wages led to a sharp rise in factory gate charges.

Mexico saw new business and production soften in February. The IHS Markit Mexico Manufacturing PMI dropped a point from January to register 51.6. Exports slowed and most new business was generated domestically. Average lead times lengthened for the seventh month and supplier deliveries slowed. Mexican firms maintained optimism and purchasing activity rose to a six-month high in anticipation of new projects. Currency volatility and higher raw material prices caused input prices to rise further in February, along with output charges. IHS Markit is forecasting easing cost pressures as the government tightens monetary and fiscal policies.

U.S. manufacturing was solid in February, posting an IHS Markit PMI of 55.3 compared to 55.5 in January. Greater client demand and increased order book volumes sustained growth in production. New business was at a 13-month high in part due to increases in export orders. Despite the favorable business conditions, optimism, while sustained, was below the long-run series average.

“The survey’s output index readings for the first two months of 2018 are indicative of the sector growing at an annualized rate of just under 3 percent,” said Williamson. “Capacity is still being stretched, however, as indicated by widespread supply chain delays and the build-up of uncompleted orders at factories. Demand, in other words, is running ahead of supply, meaning pricing power is improving. Factory selling prices are consequently rising at the steepest rate in four years.”