Market Data

April 24, 2018

ABI Softens in March as Tariff Worries Escalate

Written by Sandy Williams

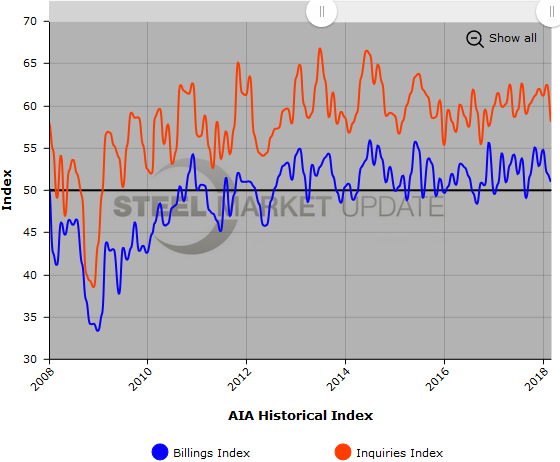

Billings at architecture firms slowed in March but remained in expansion territory at an Architecture Billings Index score of 51.0, down one point from February. Inquiries and value of new design contracts remained generally strong overall, reported the American Institute of Architects, although firms reported concern about planned U.S. tariffs on steel and aluminum. The project inquires index was 58.1 for March and the design contracts index 51.5.

“New project activity coming into architecture firms continues to grow at a solid pace. As a result, project backlogs—in excess of six months at present—are at their highest post-recession level,” said AIA Chief Economist Kermit Baker. “Business remains strong in the South and West, and firms with a residential specialization continue to set the pace.”

Business at firms specializing in multi-family residential construction remained strong in March as did those specializing in commercial and industrial design.

AIA asked firms about the potential impact of steel and aluminum tariffs on the construction sector. Nearly a fourth of respondents reported already seeing consequences from the tariff proposals, especially in the West and Midwest regions and for firms specializing in institutional design.

Almost all respondents (91 percent) expect some impact from the tariffs on their current and future projects. Of that group, 43 percent anticipate a moderate impact and 21 percent are expecting a major impact. Twenty-seven percent of those firms expecting a major impact specialize in institutional planning.

Tariff impacts on future projects include higher construction costs for projects, changes to designs to accommodate materials costs and availability, and substitution of less expensive materials. Most respondents did not think current projects would be significantly altered or canceled due to changing material costs or availability.

Regional averages: West (53.4), Midwest (50.7), South (53.2), Northeast (49.0)

Sector index breakdown: multi-family residential (53.4), institutional (49.7), commercial/industrial (53.1), mixed practice (51.1)

Below is a graph showing the history of the AIA Billings and Inquiries Indexes. You will need to view the graph on our website to use its interactive features; you can do so by clicking here. If you need assistance logging in to or navigating the website, please contact Brett at 706-216-2140 or Brett@SteelMarketUpdate.com.