Prices

June 10, 2018

Service Centers Once Again Supporting Higher Spot Prices

Written by John Packard

Both manufacturing companies and steel service centers reported a rebound in support for higher spot prices out of the distributors to their end customers. Respondents to our inquiries on the subject reported to SMU that the elimination of the exclusion status for Canada, Mexico and the European Union was the main culprit impacting flat rolled and plate steel spot pricing.

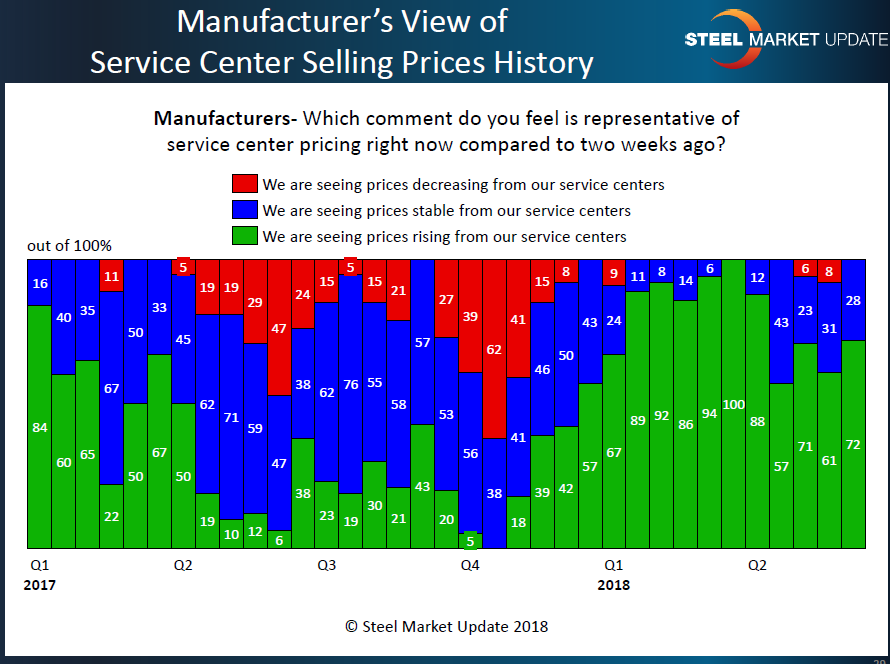

The number of manufacturing companies reporting distributors as decreasing spot pricing went from 8 percent to zero. Seventy-two percent of the manufacturing companies responding reported service centers as increasing spot prices compared to what they saw from their suppliers two weeks earlier.

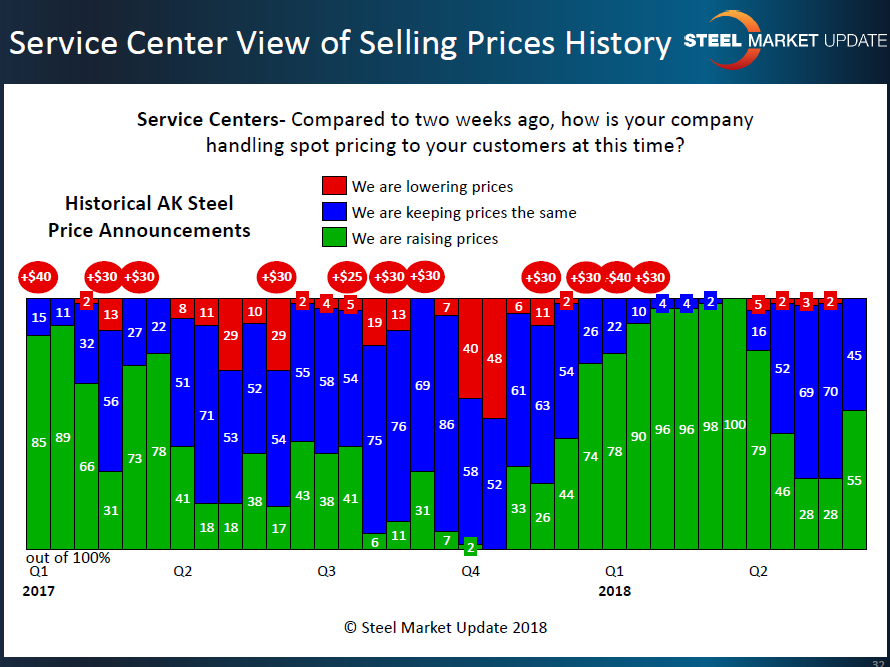

The service center response to our inquiry was even more dramatic as 55 percent reported rising spot prices. This is an increase of 27 percentage points compared to both our early and mid-May analyses. None of the steel distributors advised that their company was lowering spot prices to their end customers last week.

SMU Note: Just because a majority of service centers are reporting higher spot prices to their customers does not mean spot prices are higher than replacement cost.

In the chart above, we show the service centers’ responses in the main body of the graphic (green = higher spot prices). The red ovals above the graph represent AK Steel price announcements. It is Steel Market Update’s opinion that when service centers are raising spot prices, they are in effect supporting higher prices out of the steel mills. This is clearly seen at the beginning of the “up” price cycle that began during fourth-quarter 2017.

What is a little different about this market is the domestic steel mills are foregoing their price increase announcements. The lack of red ovals does not mean prices peaked during first-quarter 2018.

SMU will watch service center pricing activity very closely as any changes to the support (or lack thereof) of spot prices in the market will ultimately end with an erosion of pricing coming out of the domestic steel mills.