Market Data

July 31, 2018

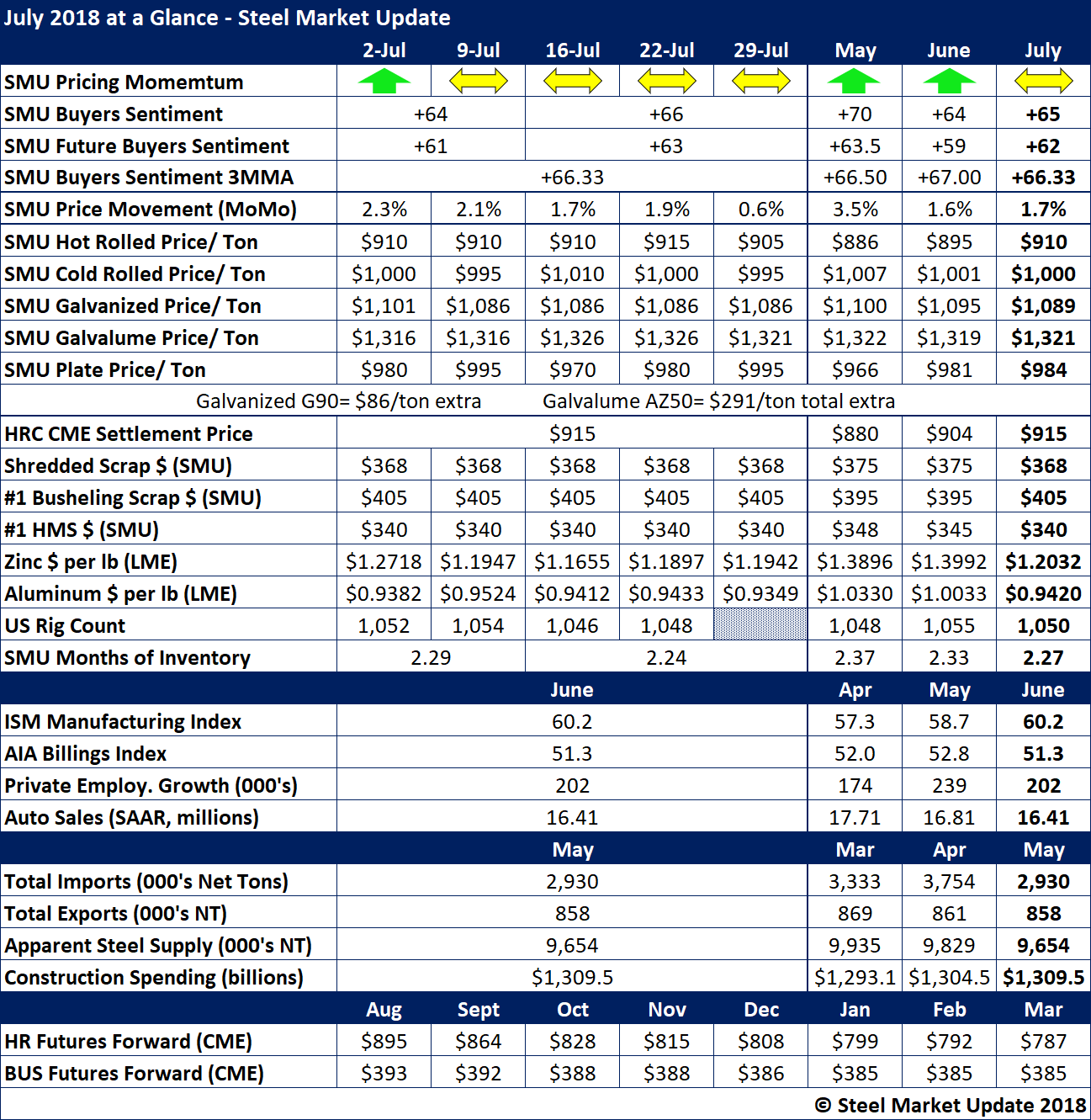

July 2018 at a Glance: Numbers Remain Positive

Written by Tim Triplett

July saw rising steel prices leveling out, prompting Steel Market Update to move its Price Momentum Indicator to Neutral. The price of hot rolled averaged around $910 and cold rolled around $1,000 a ton for the month. With prices for scrap seeing only modest changes from week to week, it’s difficult to predict what steel prices will do in August.

Sentiment among steel buyers remains at fairly high levels, in the mid 60s on SMU’s indexes, despite all the uncertainty on the trade front. The market is just starting to feel the effects of the Trump administration tariffs, and retaliatory tariffs imposed by U.S. trading partners, so the coming quarter should be telling about the prospects for the steel market moving forward.

Steel stands to benefit from positive news on the economy as GDP for the second quarter topped 4 percent. Strong hiring is keeping unemployment at near-record low levels. U.S. manufacturing continues to grow as evidenced by a 60.2 reading in the Institute for Supply Management’s latest Manufacturing Index. Automotive leads the way as carmakers continue to sell vehicles at a pace well in excess of 16 million per year.

For more information on current conditions impacting the flat rolled steel market, refer to the table below.

To see a history of our monthly review tables, visit our website.