Market Data

October 2, 2018

PMI Softens Slightly in September

Written by Sandy Williams

Manufacturing expanded in September, according to the latest Manufacturing ISM Report on Business. The headline PMI posted at 59.8 percent, well over the neutral point of 50.0, but fell 1.3 percent from August.

“Export orders expanded, but four major industries are no longer contributing. Price pressure continues, but the index softened for the fourth straight month and dropped below 70 for the first time since December 2017. Demand remains robust, but employment resources and supply chains continue to struggle, but to a lesser degree. Respondents are again overwhelmingly concerned about tariff-related activity, including how reciprocal tariffs will impact company revenue and current manufacturing locations,” says Timothy R. Fiore, chairman of the Institute for Supply Management Manufacturing Business Survey Committee.

Fifteen of the 18 manufacturing industries surveyed reported growth in September with only primary metals reporting contraction.

The new orders index declined 3.3 percentage points to 61.8 percent in September, while production expanded by 0.6 points.

“Production expansion continued in September, surpassing August expansion and resulting in the strongest gains since January 2018 when the index registered 64.5. Labor constraints throughout the supply chain, impacts due to lead-time expansions and transportation difficulties continue to limit full production potential,” said Fiore.

Supplier delivery times improved last month, but raw material inventories declined due to strong production output. Customer inventories were considered too low.

Prices continued a 31-month upward trend for raw materials, but at a slightly slower pace in September.

“The price increases across all industry sectors continue, but at lower expansion levels,” reported ISM. “The Business Survey Committee noted price increases softening in metals (all steels, steel components and aluminum). However, increases continue in various chemicals, corrugated and packaging products, freight, labor, electrical and electronic components, products manufactured primarily from steel, and paper products. Shortages continue in electrical and electronic components, labor and freight.”

Survey comments included:

- “The market is in a state of chaos with the latest round of tariffs. As an electronics original equipment manufacturer, our component prices have been impacted almost across the board. The tariffs have caused a mass rush to buy up inventories of affected products in order to minimize the long-term financial impact. This, in turn, is causing market constraints, which further drive up the cost and increase lead times.” (Computer & Electronic Products)

- “Orders are coming in, but from a limited number of customers. The future looks very promising.” (Primary Metals)

- “Suppliers are impacted by China tariffs, [which is] delaying or cancelling manufacturing transfer projects.” (Miscellaneous Manufacturing)

- “Still extremely strong through November; starting to see a decline in steel prices for December.” (Fabricated Metal Products)

- “General available capacity at suppliers continues to decrease, creating supply issues.” (Machinery)

- “Tariffs are creating a drag on some of our export opportunities.” (Plastics & Rubber Products)

- “Tariffs starting to take a bite out of profitability.” (Chemical Products)

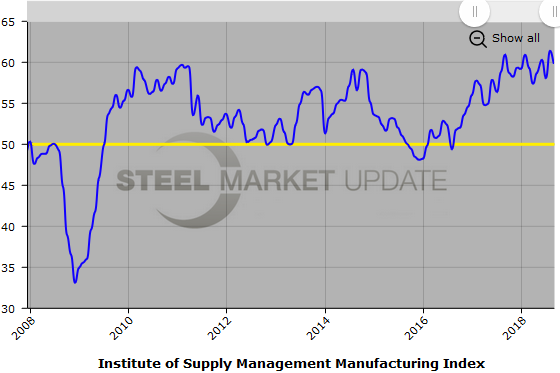

Below is a graph showing the history of the ISM Manufacturing Index. You will need to view the graph on our website to use its interactive features; you can do so by clicking here. If you need assistance logging in to or navigating the website, please contact Brett at Brett@SteelMarketUpdate.com.