Market Data

October 2, 2018

When's the Right Time to Sell? At the Top of Your Game, Say ASD Presenters

Written by Sandy Williams

In the cyclic environment of the steel industry, the best time to sell your company is when you are at the top of your game, said Vincent Pappalardo and Justin Wolfort of advisory firm Brown, Gibbons Lang & Co. Addressing service center executives at the Association of Steel Distributors regional meeting last week in Cleveland, the pair offered advice on how to prepare a company for a merger or acquisition.

Pappalardo and Wolfort laid out a strategy that focuses on M&A and private capital investments in middle market manufacturing. Private equity buyers are flush with cash in the current economy and closed over 4,000 deals representing $600 billion of deal value in 2017, they reported. In 2018, the metals industry outlook is positive but challenging. Industry-supportive initiatives by the Trump administration such as infrastructure spending and import protection will help keep steel prices healthy over the next five years, but the industry will also face commodity price volatility, a strong U.S. dollar and rising interest rates.

Because of the current strength of steel producers in the U.S, smaller players and more fragmented sectors are moving to restructure and consolidate to regain negotiating leverage with mills. Consolidation helps mitigate volatile operating expenses and create a more stable supply/demand dynamic with an added benefit of reducing volatility in pricing, said Pappalardo and Wolfort.

The decision to sell one’s company is deeply personal, added Pappalardo. Some owners want to perpetuate their legacy while others look for new beginnings. Market timing, company performance and shareholder objectives should be examined when deciding if it is the right time to sell.

A range of transaction alternatives are available for the seller from debt recapitalization, in which all equity is retained, to a full-scale sale of 100 percent of equity.

After determining the right timing, the seller must understand shareholder objectives, engage advisors, conduct an assessment of the company, identify potential buyers or partners, and develop an investment strategy to execute the transaction.

The buyer wants to know how the seller’s strategic goals and assets will fit his own company’s strategy, whether key stakeholders are prepared and aligned with a sale and if any synergies or savings will result from a completed transaction. The buyer will assess the seller’s operations from materials to market including product offerings and capabilities, market position, reputation, and customer and supplier relationships. Are margins sustainable? What is the state of the balance sheet, inventory and condition of equipment and facilities? Are any near-term capital expenditures needed? What level of working capital is necessary to operate the business and are there any hidden liabilities?

A buyer will want to know the profit forecast and if it realistic. There is no more important time to meet your forecast, said Pappalardo and Wolfort. Miss it and there are real concerns for the buyer. Bad news hurts much more than good news helps, they added.

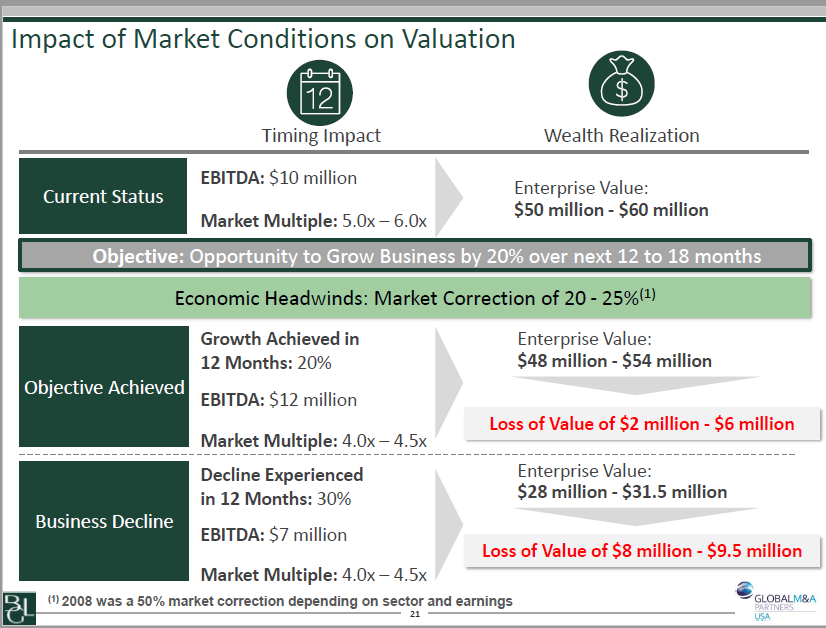

Pappalardo and Wolfort noted that market conditions can affect valuation. Most buyers hope to grow the business by 20 percent in 12 to 18 months. A market correction of 20-25 percent can create economic headwinds that cause enterprise value to plummet.

When it comes to making a deal, a targeted strategic sales process limited to 10-20 high-probability buyers can close in approximately 5-6 months. A more comprehensive sales process soliciting a diverse assortment of 100+ strategic and private equity buyers can take 6-7 months to close.

The M&A process is a personal, intensive and disruptive procedure that will go more smoothly with proper planning. And in the meantime, said the presenters, you still have a company to run.