Prices

March 19, 2019

CRU: Iron Ore High on Supply Cuts

Written by Tim Triplett

By CRU Senior Analyst Erik Hedborg

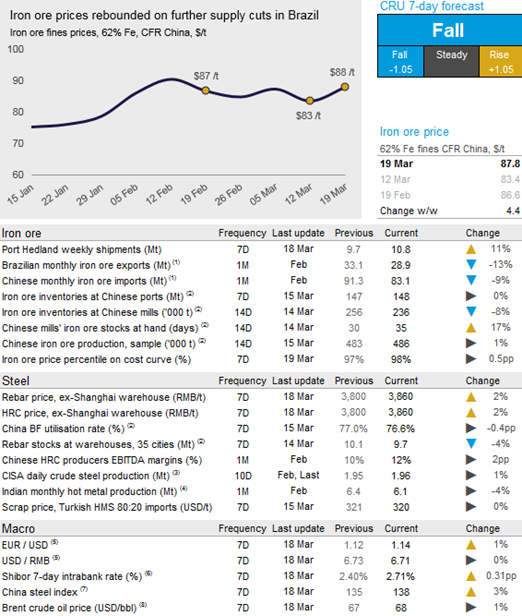

Further suspensions in Brazil lifted the iron ore market at the start of the week. Meanwhile, demand has yet to pick up in China after the National People’s Congress (NPC). On Tuesday, March 19, CRU assessed the 62% Fe fines price at $87.80 /t, up $4.40 /t w/w. This is the largest w/w price gain since the Vale accident occurred on Jan. 25.

The big news in the market is the suspension of operations at Vale’s Timbopeba site, part of the Mariana complex in Vale’s Southeastern System. The Timbopeba mine is no longer operating, but the site has a beneficiation plant that receives iron ore from Vale’s Fábrica Nova mine. Nearly half of the total output at the Mariana complex, 12.8 Mt/y of iron ore, was processed at the site. At the same time, Vale’s operations at the Guaiba port, which were suspended last week, have now resumed. The suspension lasted almost a week, considerably longer than the 24-hour suspension last January.

Shipments from Port Hedland continue to be volatile. In line with BHP’s guidance, their shipments have remained high for most of Q1. CRU estimates that the company has shipped at an annualized rate of 281 Mt/y for the first 2.5 months of the year. FMG’s supply, however, has been very volatile in the past month, which is contributing to the high volatility of Port Hedland shipments.

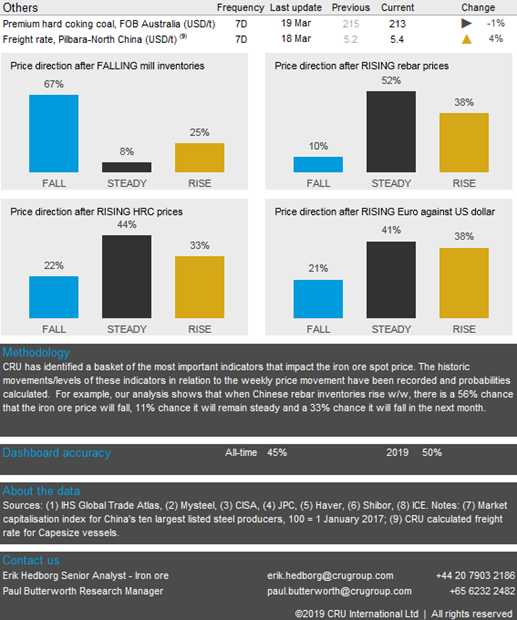

There is much uncertainty regarding the price direction in the coming week. Weak Chinese demand and high inventories, together with strong Australian supply, will limit the upside to prices. Therefore, we expect prices to fall from the current elevated level. However, there is a risk of further production cuts in Brazil in coming weeks and there is a cyclone forming east of Port Hedland, although the most recent forecast indicates it’s not expected to disrupt shipments.