Market Data

February 4, 2020

ISM PMI Shows Gains for Manufacturing in January

Written by Sandy Williams

Manufacturing grew in January along with the overall economy, reported the Institute for Supply Management. ISM’s January PMI gained 3.1 points from December to register 50.9, above the crucial no-change mark of 50.

New orders and production pulled from contraction to post respective index readings of 52.0 percent and 54.3 percent for the month, said Timothy R. Fiore, chairman of ISM’s Manufacturing Business Survey Committee.

Supplier deliveries registered 52.9, a 1.7 percent retreat from December. A reading below 50 percent indicates faster deliveries, while readings above 50 indicate slower deliveries.

New orders drew down manufacturer inventories in January while customer inventories, still considered too low, were moving closer to “about right” levels. Current levels will support future production output, said Fiore.

The backlog of orders index remained in contraction at 45.7, but rose 2.4 points for the month.

The prices index rose 1.6 points to 51.7 indicating higher raw material prices. Fiore noted that the January price index was supported by growth in steel and aluminum prices, which registered their highest level since March 2019.

“Suppliers continue to struggle to deliver to panelists’ satisfaction, with many suppliers sluggish to respond after the post-holiday period. Lead times appear to be stabilizing. The index expansion, coupled with price growth, continues to be a positive indicator for the balance of Q1. Supplier capacity remains at satisfactory levels to support near-term production demand,” said Fiore.

Import and export orders both expanded in January. The index for export orders gained 6 points to register 53.3. The import index gained 2.5 points to register 51.3, its best performance since February 2019.

“Global trade remains a cross-industry issue, but many respondents were positive for the first time in several months,” said Fiore. “Overall, sentiment this month is moderately positive regarding near-term growth.”

Comments from survey respondents included:

- “Our business is starting 2020 stronger than we finished 2019, as we saw a dramatic downturn in orders over the last four months of 2019. Orders are up to start the year, but slightly behind where they were one year ago.” (Fabricated Metal Products)

- “Business has picked up considerably. Many of our suppliers are working at or above full capacity. Tariffs are still a concern and are believed to be a factor in short supply and higher prices of electronic parts. Our profit margin has been somewhat negatively affected by high tariffs, particularly on electronic parts from China.” (Computer & Electronic Products)

- “The annual holiday slowdown was slightly more significant compared to the previous three years, heightening concerns over the 2020 first-quarter forecast.” (Electrical Equipment, Appliances & Components)

- “Small signs of increased global demand in the chemical segment.” (Chemical Products)

- “Continued signs of slowdown in manufacturing.” (Transportation Equipment)

- “Our customer slowdown has not reached the bottom.” (Petroleum & Coal Products)

- “The lack of faith in the economy seems to be why we cannot sell capital projects.” (Machinery)

- “Tariffs on injection molds will impact selection of mold builder for future jobs. We are more likely to choose domestic rather than offshore.” (Plastics & Rubber Products)

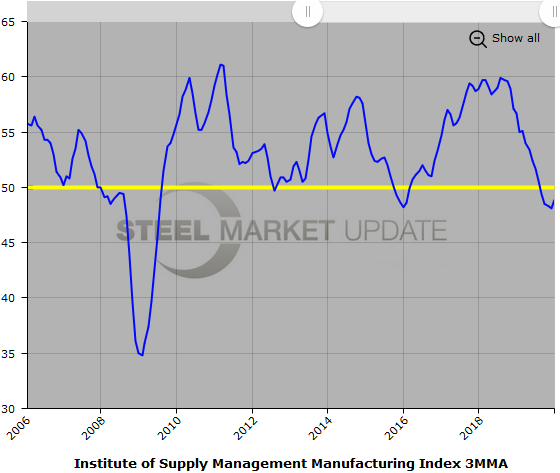

Below is a graph showing the history of the ISM Manufacturing Index. You will need to view the graph on our website to use its interactive features; you can do so by clicking here. If you need assistance logging in to or navigating the website, please contact us at info@SteelMarketUpdate.com.