Prices

February 6, 2020

CRU: Chinese Zinc Market Feels the Impact of Novel Coronavirus

Written by Dina Yu

By CRU Senior Analysts Dina Yu and Helen O’Cleary, from CRU’s Zinc Monitor

The outbreak of novel coronavirus (2019-nCoV) in Wuhan has delayed the post-New Year restart in most Chinese mainland provinces, with the exception of Tibet, Xinjiang and Gansu. Sadly, the death toll and infection rate continue to rise, so restrictions remain in place in a bid to contain the spread. While businesses in Jinlin and Qinghai restarted on Feb. 3, the shutdown in most provinces will continue until Feb. 10. Businesses in Tianjin remain closed and a restart date has yet to be set, while in Hubei, where the outbreak originated, businesses have been told to remain closed until Feb. 14.

Zinc’s Price Plunges as Demand Falters

The restart of trading on the SHFE on Feb. 3 saw zinc’s price plunge by RMB790 /t ($110 /t) to RMB17,370 /t. Given that the LME price had lost more than $260 /t since Jan. 23, when the scale of the outbreak began to dent market sentiment, the price reaction on the SHFE was relatively modest. Although zinc’s price fell to a recent low of $2,187.5 /t on Feb. 3, the less steep falls on the SHFE have since helped lift it to $2,230 /t at the time of this writing.

After a stronger than expected 2019 H2 for Chinese demand, in part due to stimulus measures and in part due to mild winter weather allowing construction activity to continue for longer than normal, we were expecting to see growth momentum continue into 2020 Q1, especially given the relatively early Chinese New Year. However, the disruption to business as a result of the 2019-nCoV outbreak has at best postponed the expected uptick in refined demand and at worst could lead to actual losses.

• Consumption of all kinds of goods has been dampened by the outbreak, as a large part of the population has remained at home for the past two weeks, either under official or self-imposed quarantine. Sales of vehicles, white goods and property are all expected to be weak in late January and February.

• Hubei, the epicenter of the outbreak, is China’s sixth largest steel-making province and home to Baowu (Baosteel and Wuhan Steel), China’s single largest auto galvanized sheet manufacturer. All businesses here will remain closed until Feb. 14.

• Shanghai, Jiangsu, Zhejiang, Guangdong, home to many die casters and galvanizers, have postponed the post-holiday restart until Feb. 10, while in Tianjin, a major port city in northeastern China, close to Beijing, businesses have yet to be given a restart date.

• Public transport has been suspended in Tangshan, Hebei, China’s largest steel-making province to the east of Beijing, although at the time of this writing no restrictions have been imposed on businesses.

• Construction-related activities were unlikely to restart immediately after the New Year holiday as the weather is too cold, but even so there are restrictions in place. We currently expect construction-related galvanizing demand to pick up in late-February/early-March in the run-up to the peak construction season.

• In the short-term, disruption to transport will inhibit the movement of goods, and internal markets as well as export markets for zinc products and products related to zinc are expected to decline in the short-term.

• The extended holiday will increase operating costs for all sectors in the short term, and some small manufacturers in particular could face great financial pressure. However, the government is likely to help mitigate the strain on businesses by increasing financial sector liquidity and temporarily lowering some taxes.

• Assuming that normal activity is resumed relatively quickly, we expect this to lead to pent-up demand and a rebound in activity in subsequent quarters, leading to volatility in growth rates rather than outright losses.

• While downside risk to demand has increased (our Economics team estimates that 2020 IP could slow by 1.0 percent), it is too early for us to consider lowering our current refined demand growth forecast for this year of 1.2 percent. That said, the hit to China’s 2020 Q1 GDP and IP growth is likely to dampen market sentiment in the short-term.

Chinese Smelters May Take Maintenance or Reduce Output Due to Falling Demand

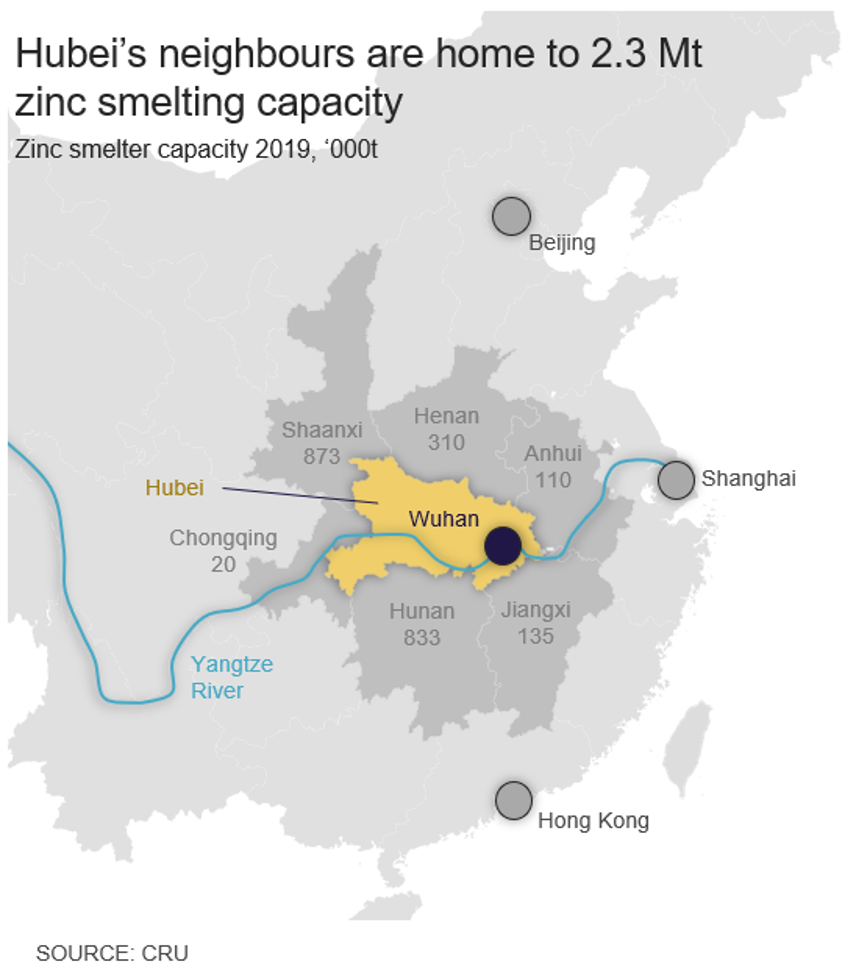

There are no zinc mines or smelters in Hubei, the epicenter of the outbreak, and of the neighboring provinces Hunan is the only significant miner, but smelters are beginning to feel the effects of weak demand.

• Hunan produced an estimated 302,000 t in 2019, while total mined production from the six neighboring provinces was around 440,000 t, equivalent to 10 percent of total Chinese mine production.

• Smelting capacity is significant in both Hunan (833,000 t in 2019) and Shaanxi (873,000 t in 2019) and total refined nameplate capacity in the six neighboring provinces was 2.3 Mt last year, equivalent to 32 percent of total Chinese capacity.

• Although the 2019-nCoV outbreak has had a limited direct impact on smelter production, which remained relatively stable during the holiday, some smelters had already cut production and more are planning to this month due to weak demand for refined metal and sulphuric acid.

• Sulphuric acid is difficult to store, so if restarts are postponed further, more smelters may be forced to cut production or carry out maintenance in Q1.

Refined stocks in the Tianjin, Shanghai and Guangdong-based warehouses increased by around 70,000t in the past two weeks. We understand that inventory held by smelters also increased during the holiday due to weak demand and the suspension of trucking.

Request more information about this topic.

Learn more about CRU’s services at www.crugroup.com