Prices

March 15, 2020

What Will the Coronavirus Do to Steel Prices?

Written by Tim Triplett

Steel prices are as unpredictable as the spread of a rogue virus, but one symptom of COVID-19 is likely to be lower steel prices.

As of this writing on March 13, the price of flat rolled steel products had yet to see much effect from the global panic over the coronavirus. Steel Market Update’s latest canvass of the market showed an average spot price for hot rolled coil of $580 per ton ($29.00/cwt), FOB the mill east of the Rockies. Cold rolled and galvanized were around $770 per ton ($38.50/cwt). These numbers moved up and down within a small range in the first two and a half months of the year and saw only a small uptick from the price hike announced by the mills in late February. The average price of steel plate delivered to the customer’s facility was $650 per ton ($32.50/cwt), down from $700 ($35.00/cwt) at the beginning of the year.

SMU’s Flat Rolled Price Momentum Indicator remains at Neutral as the market struggles to establish a clear direction amid all the turmoil caused by the spread of COVID-19. Momentum for plate is pointing Lower.

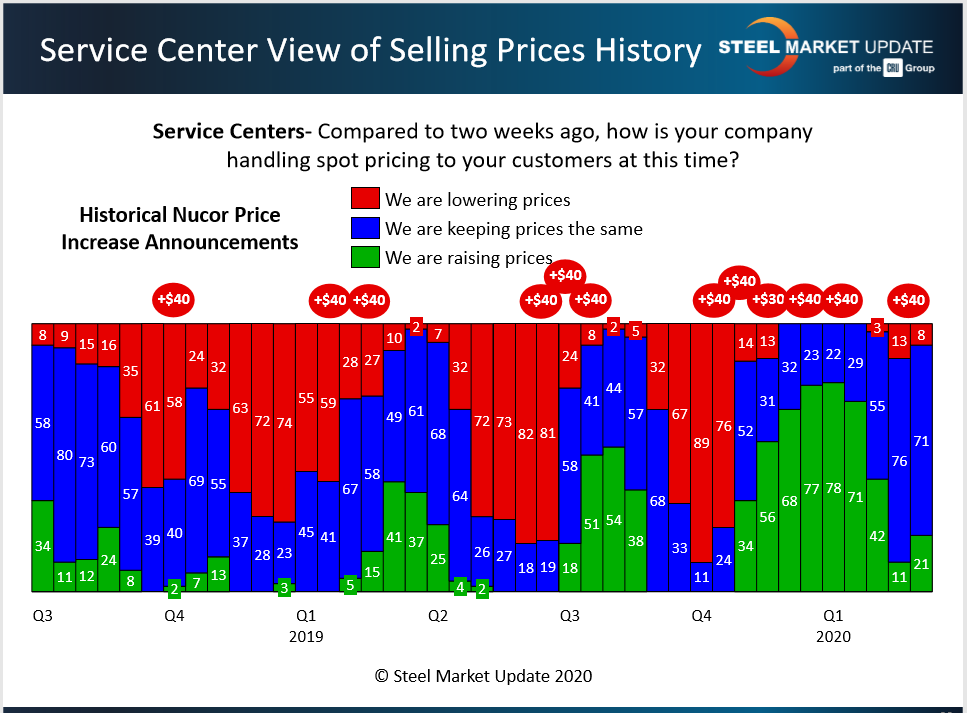

The last price hike by the mills received limited support from the service centers, as shown in the bars on the right in the chart below. Only 21 percent of those responding to SMU’s poll said they were raising prices to their customers. The vast majority were holding the line or even lowering prices given the uncertain market conditions.

Analysts at SMU’s sister company CRU predict the virus will deliver a serious blow to global industrial production and economic growth. Their forecast calls for a GDP decline of at least 0.2 percent, and possibly as high as 1.0 percent, which would take world growth into recessionary territory.

Even as China closed factories and quarantined millions of its citizens to stop the spread of the virus, its mills continued to produce steel. So much steel, in fact, that they reportedly have run out of space to store it and have resorted to leaving rebar and coils on the ground out in the weather. As its steel-consuming industries struggle to get back on their feet, China has an enormous incentive to export this excess production, at whatever cost, which will be a threat to global steel prices for many months to come.

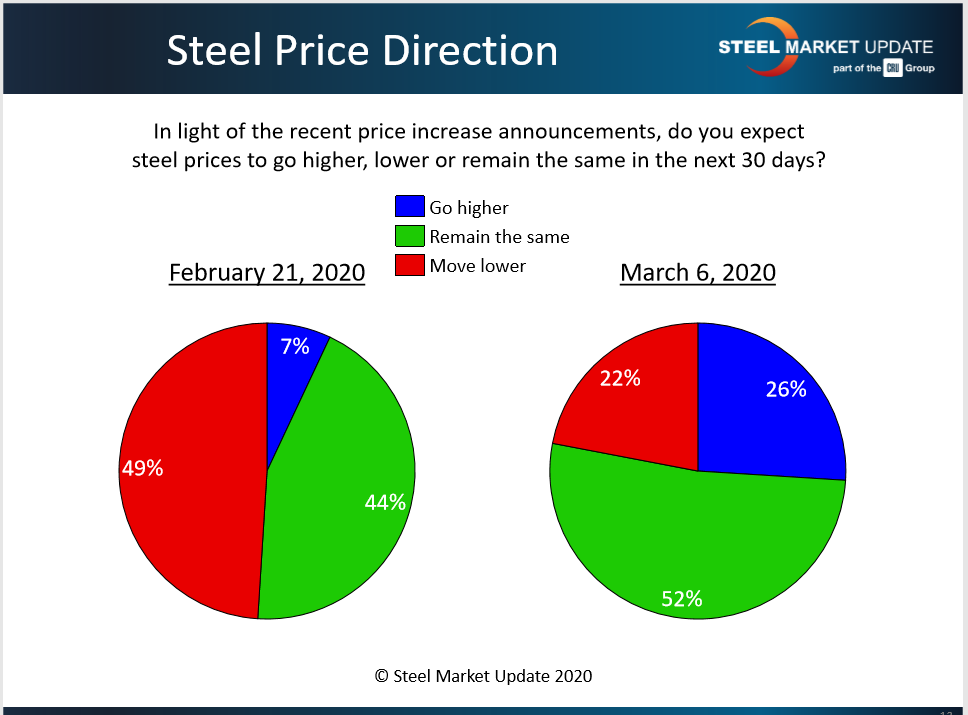

Steel buyers polled by SMU in the first week of March were clearly unsure of what to expect in terms of steel prices. Between the $40 per ton flat rolled increase announced by the mills on Feb. 27 and the doom and gloom predictions of economic disaster from the virus, most were at a loss to predict what would happen next. Around half said prices would remain about the same. Another 22 percent expected prices to move even lower in the coming month, while just 26 percent anticipated higher prices.

Price War in the Energy Market

Since the turn of the year global oil demand has been hit hard by the COVID-19 virus. Crude prices fell by 30 percent in a single day this month. CRU predicts oil prices could remain around $40 per barrel for some time. Oil prices that low offer little incentive for new exploration and will dampen demand for oil country tubular goods, line pipe and other energy-related steel products.

Compounding the problem is the oil price war between Saudi Arabia and Russia. Instead of lowering production in line with the lower demand from COVID-19, Russia refused to cut back. In response, Saudi Arabia increased production and lowered prices, forcing other OPEC members to follow suit. Depending on how long it lasts, this energy price war will challenge shale oil producers in North America, as well as their steel suppliers.

Energy market experts at CRU reported the following: “U.S. crude production has been growing since the shale boom of 2014. The EIA forecasts U.S. crude oil production to average 13.2Mbbl/day in 2020. While production has boomed, so have the debt levels of shale-producing companies. U.S. shale needs the crude oil price to be ~$50/bbl to break even. Companies that have not hedged their revenue against lower oil prices may see investors leave and their companies ultimately go out of business. Those that have hedged their output will be safe for now, but if the price war continues for a prolonged period, they could follow suit. Some U.S. shale companies have seen their share prices drop by more than a third following the decline in oil prices. Speculation is that this is Russia’s aim—to squeeze the U.S. shale companies and push the marginal suppliers to shut down.”

Steel Demand in Flux

Steel prices are a function of steel demand, of course. The extent to which the virus impedes manufacturing in the United States remains to play out. The latest figures from the Institute for Supply Management show their PMI registered 50.1 percent in February, just above the 50.0 level that indicates growth. The PMI was already trending down from 50.9 in January and, given the fallout from the virus, is likely to move into contraction in March. Comments from purchasing managers polled by ISM showed widespread concern about COVID-19. “Coronavirus continues to be front and center as a major supply chain risk to our company. Access to information in China—from our supply base and customers—is slow to come by” said one fabricator. “Coronavirus is wreaking havoc on the electronics industry. Companies are delayed in starting up production, which is resulting in longer lead times, constraints and increased pricing. It’s a mad dash to dual source stateside in case China isn’t back online soon,” said another executive.

Automotive production has been a boon to the global economy for the past decade, but the virus represents a giant speedbump. China’s auto industry, which produces one-third of the world’s vehicles or 26 million cars and trucks per year, has been stalled by the virus. The effect on China’s auto industry has global implications due to the number of Chinese components that are used in auto production in other countries. Supply line disruptions due to plant closures, labor shortages and transportation restrictions will cause problems in auto plants all over the world. The same holds true for agricultural equipment, electronics and most other sectors.

Lead Times and Negotiations

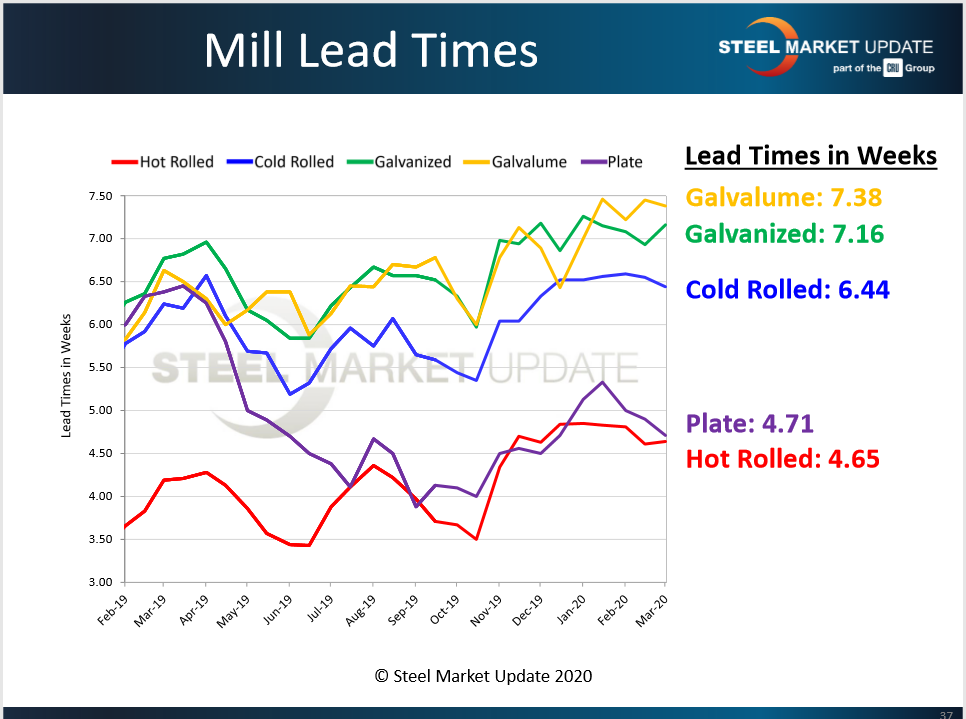

Lead times for steel delivery are an indicator of demand at the mill level. The longer the lead time, the busier the mill and the less likely they are to negotiate on price. In the first week of March, the average lead time for spot orders of hot rolled steel was about 4.6 weeks, while cold rolled was at 6.4 weeks and coated steels were at just over 7 weeks. The current lead times have not fluctuated much this year and are higher than at this time last year, which shows the mills sustaining relatively healthy order levels, at least through mid-March. If the virus proves to be the impediment to commerce that’s predicted, SMU expects lead times to shorten in the coming weeks as activity slows down at the mills.

According to the majority of steel buyers polled by SMU in the first week of March, mills remained open to price negotiations even after announcing their late-February price increase. That points to competitive market conditions and possibly lower steel prices as the threat from the virus take shape.

Ferrous Scrap Prices Surprise

How much the mills must pay for raw materials also factors into the price of steel. The iron ore market relies heavily on Chinese demand, which remains uncertain due to disruptions from the virus. Ferrous scrap prices surprised to the low side in March, trading sideways to up just $10 per ton, well below initial expectations of up $10-30/GT. The mills were anticipating that higher scrap prices would lend support to their $40 increase in finished steel prices.

What Steel Buyers Are Saying

- “The market is struggling for direction on prices, elections and viruses.”

- “Sentiment’s positive but cautious due to the situation in China with the coronavirus.”

- “Due to the threats of the impact of the coronavirus, I believe people will start to pull back. But U.S. construction fundamentals are strong and this will allow steel consumption to continue in the short- and longer-term.”

- “We are still optimistic on the construction market, our core business, over the next six months, but the weather, coronavirus and upcoming election could alter that feeling.”

- “Optimistic but cautious due to the situation in China with the coronavirus.”

- “Too many uncertainties.”

- “Fear of the unknown.”

Many factors will figure into the price of steel in the coming months—the pace of recovery in China, the duration of the Saudi-Russia oil price war, the health of manufacturing in North America, scrap prices, moves by steel producers and distributors—and of course the persistence of the coronavirus. COVID-19 is the very definition of a “black swan event.” Its unexpected and unprecedented nature make its ultimate impact on the global economy and steel prices unknowable. What’s certain is that it has disrupted the lives of millions all over the world, with tragic consequences for thousands, and it is not done yet.