Analysis

March 18, 2020

Final Thoughts

Written by John Packard

The new normal for me is talking to an industry executive on the phone and listening to the kids playing in the background….

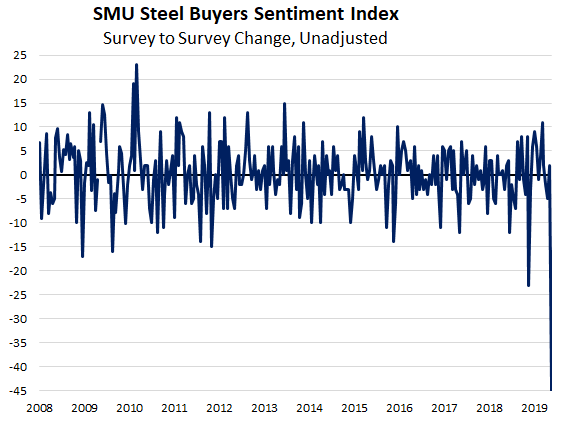

We had a 45-point drop in both the Current and Future SMU Steel Buyers Sentiment Index this week (article is at top of tonight’s issue). This is the largest one-week change in the history of our index, which goes back to 2008 (see graphic below).

Two weeks ago I could sense the resistance to the virus and its impact on the United States. I received some negative comments on articles SMU was writing about what economists were forecasting and the possibility of a dramatic drop in the economy here in the United States. No one wanted to believe that the U.S. could have issues like what happened in China. This week the resistance has dropped, for several reasons: Automotive shutting down in Europe and the United States. People watching what is happening in Italy, and how closely the U.S. is mimicking the Italian trajectory of cases, which is worse than what happened in China. And the destruction of the stock market losing all of the “Trump bump” since he became president. Those who were resistant are now concerned. Those who were concerned two weeks ago are now anxious. Those who were anxious two weeks ago are now hunkered down in their homes, Face-Timing their parents and kids while trying not to listen to the news….

Two weeks ago I could sense the resistance to the virus and its impact on the United States. I received some negative comments on articles SMU was writing about what economists were forecasting and the possibility of a dramatic drop in the economy here in the United States. No one wanted to believe that the U.S. could have issues like what happened in China. This week the resistance has dropped, for several reasons: Automotive shutting down in Europe and the United States. People watching what is happening in Italy, and how closely the U.S. is mimicking the Italian trajectory of cases, which is worse than what happened in China. And the destruction of the stock market losing all of the “Trump bump” since he became president. Those who were resistant are now concerned. Those who were concerned two weeks ago are now anxious. Those who were anxious two weeks ago are now hunkered down in their homes, Face-Timing their parents and kids while trying not to listen to the news….

The problem is there are still many Americans who are in denial. You can see them on the beaches in Florida and elsewhere around the country. It is hard to accept that the world is a different place than it was just a short couple of months back.

I hope our articles on working from home are helpful to you and your company. If there is a subject you would like for us to address, please let me know by sending us an email: info@SteelMarketUpdate.com. We think of SMU as a provider of community information and a way for the industry to stay connected.

I want to thank the manufacturing company executives who responded to my inquiry earlier today regarding how they were preparing their facilities and employees for the fight against the COVID-19 virus, and if there were any plans to cease production. Getting early responses to these key questions is critical to those of you who service these industries, and to the steel-producing community which understands there most likely will be a disruption in their order books in the weeks and months to come.

If you would like information about how to renew, upgrade from Executive to Premium, add more subscribers or become a new subscriber, please contact Paige Mayhair at Paige@SteelMarketUpdate.com or by phone at 724-720-1012.

Our Aug. 24-26, the SMU Steel Summit Conference will have the strongest lineup of any conference we have ever hosted, or of any steel conference held in North America. We continue to take registrations with the knowledge that if we are forced to cancel, we will provide full refunds. You can find more information by clicking here or by going to www.SteelMarketUpdate.com/Events/Steel-Summit

As always, your business is truly appreciated by all of us here at Steel Market Update.

John Packard, President & CEO