Overseas

April 2, 2020

CRU: Steel Prices Down as China Tries to Rebalance

Written by George Pearson

By CRU Prices Analyst George Pearson, from the CRU Steel Monitor

As expected, sheet prices in the U.S. Midwest market have fallen. Prices today, reflective of transactions booked last week, fell by $13-26 /s.ton w/w. For all sheet prices, we continue to hear of lower priced offers and expect that transaction prices will continue to fall over the near term. HR coil prices fell $13 /s.ton to $548 /s.ton. Overall volume reported to us was just under the prior week, yet with data coming through from multiple buyers and mills, the market remains liquid. If we come across a week where liquidity is truly limited, we have provisions in our methodology to continue to assess a price.

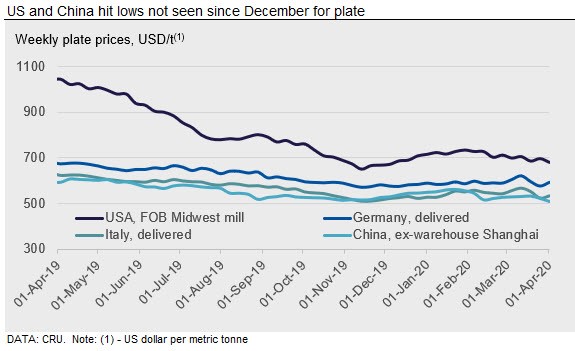

We continue to expect lower scrap prices for April, which will pressure finished steel prices alongside the overall curtailment of demand due to Covid-19. Plate prices turned lower again after a brief respite last week. Prices here fell to a new cycle low, losing $15 /s.ton w/w. Our price assessment for plate was based on higher volume than last week and while some data providers were steady and others higher w/w, the majority were lower.

European prices showed another gradual decrease this week. Spot business has dried up and so although the market expects lower prices, and those in the regions around Europe have fallen significantly, sellers see no advantage in quoting lower prices when buyers are unlikely to purchase. The absence of several companies in Italy—normally Europe’s prime mover for price—is also part of the reason for lack of downward movement in prices as there is less liquidity. German HR coil stood at €472 /t this week, down €3 /t w/w. Italian HR coil was unchanged at €443 /t but other products there fell €4–5 /t. The Italian plate price is now at its lowest since Jan. 8 and €22 /t above the low point it reached last year. The Italian government has extended the shutdown of schools and non-strategic businesses until mid-April.

The Chinese HR coil price fell by RMB120 /t to RMB3280 /t w/w, while rebar decreased by RMB100 /t. Flat prices took a heavier hit for a few reasons. Although domestic demand during March improved, it was still at a low level. The Caixin China manufacturing PMI rose to 50.1 in March from 40.3 in February. This figure implies that business only grew slightly compared to February, when the economy was largely at a halt. Flats-intensive end-use sectors such as automotive and manufacturing were especially impacted. In addition to this, some steel export orders were cancelled, and exports of manufactured products were lower.

As for the longs, although the market was less impacted by overseas demand, domestic demand recovery was lower than expected. Specifically, the “new infrastructure” projects put forward to offset the economic impact of Covid-19 offered limited support to steel consumption, because these projects were focused on innovation initiatives such as big data, artificial intelligence, driverless cars and quantum computing. Therefore, the earlier enthusiasm driven by these projects started to fade.

The total inventory at the mills and traders decreased for the first time in the year in mid-March and continued to drop by 5 percent this week. Weekly output had increased by 2 percent w/w, but is still at low levels compared to same time last year. Looking ahead, steel prices remain under pressure but the improved demand expected in April will limit sharp price falls.

Request more information about this topic.

Learn more about CRU’s services at www.crugroup.com