Market Data

April 2, 2020

Pandemic Expands Global Downturn for Manufacturing

Written by Sandy Williams

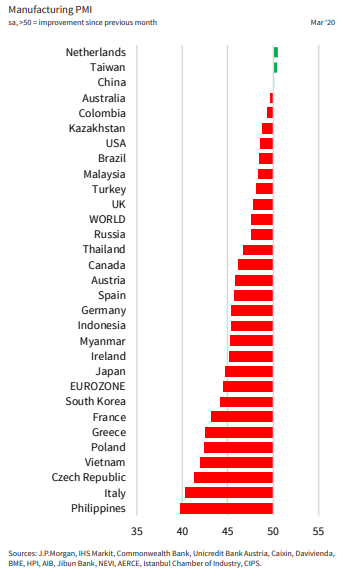

Global manufacturing continued its downturn in March exacerbated by the COVID-19 pandemic. The J.P. Morgan Manufacturing PMI rose to 47.6 from 47.1 in February due to a stabilization of business conditions in China.

China’s PMI jumped from 40.3 in February to 50.1 in March as manufacturing activity returned to more normal conditions after new coronavirus cases began to subside. Excluding China, the global PMI was 46.6 in March, the lowest level since May 2009.

China’s PMI jumped from 40.3 in February to 50.1 in March as manufacturing activity returned to more normal conditions after new coronavirus cases began to subside. Excluding China, the global PMI was 46.6 in March, the lowest level since May 2009.

International trade plummeted as nations closed their borders, and production and new orders plunged at rapid rates. Global supply chain disruption led to the steepest increase in average vendor lead times in the survey’s history. Inventories for both pre- and post-production declined.

The IHS Markit Eurozone Manufacturing PMI dropped to 44.6 in March after a one-year high of 49.2 in February. Only the Netherlands reported a PMI above the neutral mark at 50.5. Manufacturing output and new orders fell to an 11-year low. Exports fell for the 18th successive month and at their fastest rate since March 2009. Supplies were difficult to obtain with lead times deteriorating to a survey near-record. Business confidence fell to the lowest ever recorded by the survey to date.

Chris Williamson, chief business economist at IHS Markit, commented, “The concern is that we are still some way off peak decline for manufacturing. Besides the hit to output from many factories simply closing their doors, the coming weeks will likely see both business and consumer spending on goods decline markedly as measures to contain the coronavirus result in dramatically reduced orders at those factories still operating. Company closures, lockdowns and rising unemployment are likely to have an unprecedented impact on expenditures around the world, crushing demand for a wide array of products. Exceptions will be food manufacturing and pharmaceuticals, but elsewhere large swathes of manufacturing could see downturns of the likes not seen before.”

Manufacturing conditions In China were broadly stable in March with the Caixin China General Manufacturing PMI jumping out of contraction to 50.1. As the first country to complete a coronavirus cycle, easing of company closures and travel restrictions led to an increase in output. Demand is still considered fragile, with firms noting delayed and cancelled orders. Export orders in March dropped significantly as the coronavirus took hold across the world. New orders remained in contraction even as output increased. Post-production inventories accumulated due to continued transportation disruptions. Employment levels were stable and businesses expressed confidence in the 12-month outlook.

Dr. Zhengsheng Zhong, chairman and chief economist at CEBM Group, commented, “To sum up, the manufacturing sector was under double pressure in March; business resumption was insufficient; and worsening external demand and soft domestic consumer demand restricted production from expanding further. Whereas, business confidence was still high and the job market basically returned to the pre-epidemic level, laying a positive foundation for the economy’s rapid recovery after the epidemic.”

Manufacturing in Japan slid further into contraction in March, dropping from a PMI reading of 47.8 in February to 44.8. The COVID-19 pandemic resulted in the sharpest decline in demand in nearly nine years as new orders fell domestically and abroad.

“Japan’s manufacturing downturn deepened in March as a result of the global COVID-19 pandemic, which on top of the international supply chain paralysis caused by shutdowns in China, and now other parts of the world, has also dealt a severe blow to export demand,” said Joe Hayes, economist at IHS Markit. “The consequence was the steepest drop in goods production since the aftermath of the devastating tsunami in April 2011.”

“The likelihood of the manufacturing recession deepening in the coming months is high,” added Hayes. “Overall, the cascading impact of COVID-19 on the global economy is diminishing the chances of a V-shaped recovery.”

The coronavirus began to impact Russia manufacturing in March, weakening domestic and foreign demand. The manufacturing PMI slid to 47.5 from 48.2 in February. New orders fell at the quickest pace in four months, continuing the contraction that began in June 2019. Prices for raw materials jumped and additional costs were passed on to clients. Business confidence sank to a series low as “uncertainty regarding the strength of the global economy and future demand weighed heavily on manufacturers minds,” said IHS Markit economist Sian Jones. IHS Markit expects industrial production in Russia to contract year-over-year in the first quarter and predicts accelerating contraction through the remainder of the year.”

Canada is experiencing its steepest drop in production, new orders, and employment in nearly nine-and-a-half years. The IHS Markit Manufacturing PMI tumbled to 46.1 in March from 51.8 in February. Demand fell sharply as measures to control the COVID-19 outbreak shuttered businesses and stopped production at home and abroad. Firms also cited a sharp drop in demand from the energy sector. Supply shortages were rampant and the suppliers’ delivery index dropped to a record low of 34.6 indicating significantly longer delivery times. Staffing was reduced at the fastest rate since the survey began. A strong U.S. dollar to Canadian pushed up input costs for manufacturers.

Manufacturing in Mexico declined as new orders fell at their quickest pace since April 2011 driven by a decline in domestic and export orders due to the COVID-19 crisis. As a result, staffing was cut and purchasing activity reduced. The IHS Markit Manufacturing PMI fell to 47.9 in March to its second lowest reading in nine years. Production cuts were the sharpest in three months. Input costs rose as supply chain disruptions increased.

“The fall in Mexican factory production in March, though marked, was disproportionate to that seen in new orders and suggests we will see further output reduction as supply is pared back to match the dire demand environment,” said IHS Markit economist Eliot Kerr.

PMI data for the U.S. was worse than expected, said IHS Markit’s Chris Williamson. The PMI dipped to 48.5 in March, below the “flash” figure of 49.2 and February’s posting of 50.7.

“The overall deterioration in the health of the manufacturing sector was the fastest since August 2009, but was buoyed by a marked decline in vendor performance (usually a sign of strengthening demand conditions but currently reflecting widespread supply shortages linked to the COVID-19 pandemic),” said IHS Markit.

Output and new orders dropped at the sharpest pace in more than a decade. Export orders, in particular, were hit hard. Employment levels declined as manufacturers cut production and furloughed or laid off workers due to the pandemic and weakened demand.

“Growing numbers of company closures and lockdowns as the nation fights the COVID-19 outbreak mean business levels have collapsed,” said Williamson. “Orders for capital equipment have deteriorated at a rate not seen since data were first available in 2009 as firms stopped investing in machinery. Companies have meanwhile reined-in spending on inputs and households have pulled back sharply on many forms of spending, especially for non-essential and big ticket items. With export sales also sliding, factories are facing a broad-based slide in demand, which is already resulting in the largest job losses recorded since the global financial crisis. Worse is likely to come as consumer spending falls further in coming months as lockdowns intensify and unemployment spikes higher.”