Market Data

May 4, 2020

Pandemic Devastates Global Manufacturing in April

Written by Sandy Williams

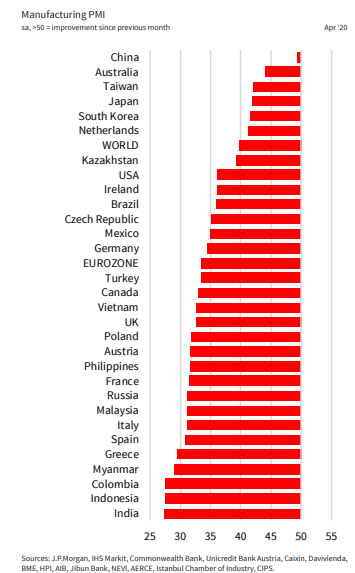

The COVID-19 crisis devastated manufacturing across the globe in April. The pandemic laid low virtually all economies, plunging the J.P. Morgan Global PMI to 39.8 for the steepest contraction since the financial crisis of 2008/2009. China, although still in contraction, fared the best of the nations surveyed and helped to soften the downturn. Excluding China, the global PMI was 35.8, down from 46.2 in March. Production and new orders plummeted, international trade was nearly at a standstill, supply chains were severely disrupted and employment levels fell at the quickest pace in 11 years.

Olya Borichevska, global economist at J.P. Morgan, commented: “The continued impact of the global COVID-19 pandemic caused significant disruption to industrial activity during April. Output and new orders contracted at near survey record rates as demand, international trade flows and economic sentiment were all constrained by restrictions to stop the virus spreading, company closures and shortages of material and labor. Only time will tell how permanent the damage to global supply chains is, although moves in many nations to loosen lockdowns may provide a guide over the coming weeks and months.”

Olya Borichevska, global economist at J.P. Morgan, commented: “The continued impact of the global COVID-19 pandemic caused significant disruption to industrial activity during April. Output and new orders contracted at near survey record rates as demand, international trade flows and economic sentiment were all constrained by restrictions to stop the virus spreading, company closures and shortages of material and labor. Only time will tell how permanent the damage to global supply chains is, although moves in many nations to loosen lockdowns may provide a guide over the coming weeks and months.”

Manufacturing conditions in the Eurozone plunged to a record low in April as COVID 19 impacted the region causing factory closures, weak demand and supply shortages. The PMI fell 11.1 points from March to register 44.5 and the lowest result since the series began in June 1997. Restricted economic activity and social distancing measures led to a sharp drop in production, new orders and backlogs. Delays in transportation added to supply disruptions causing lead times to deteriorate at an unprecedented rate, said IHS Markit. Purchasing activity was slashed as firms used existing inventory to cut costs. As the pandemic curve flattens across the region, business is expected to pick up. “However, the PMI is indicating an industrial sector that has collapsed at a quarterly rate of decline measured in double digits, and any recovery will be frustratingly slow,” commented IHS Markit Chief Economist Chris Williamson.

China, first to be hit by the pandemic, has started its comeback, albeit at a slow pace. After stabilizing in March at 50.1, April’s PMI slid back into contraction to 49.4. Production rose as more firms reopened and capacity increased. New orders, however, fell for a third month as export orders plunged at its steepest rate since December 2008 as the rest of the world continued to struggle with the COVID-19 crisis. Raw material prices declined, particularly for glass and steel, as inventories accumulated due to limited demand.

“Both the gauges for business confidence and employment dropped. Unlike in February and March, manufacturers’ confidence was not high in April as the coronavirus’ hard hit on external demand forced them to reassess the pandemic’s impact; the economic shock may be greater than previously thought, and it may take longer for the economy to recover,” commented Dr. Zhengsheng Zhong, chairman and chief economist at CEBM Group.

Manufacturers in Russia saw substantial declines in production and new orders as public health orders closed businesses and reduced workforce. The IHS Markit Russia PMI plummeted to 31.3 in April from 47.5 in March. Demand was weak at home and across Europe causing new orders to fall at an unprecedented rate and backlogs to fall sharply. A depreciating ruble drove imported input prices higher resulting in a significant increase in output charges. Optimism was at a record low as firms worried about how long the lockdowns will last and what the recovery will look like. IHS Markit is expecting industrial production to decline 3.8 percent in 2020.

In North America, U.S., Canada and Mexico manufacturing conditions continue to reel while the pandemic rages.

The Canada manufacturing PMI slid to 33.0 in April from 46.1 in March. Record declines were noted in output, new orders and employment—all at index readings in the low to mid-20s. Sales were severely impacted in the automotive and energy sectors. Longer lead times reflected distressed supply chains and delays at international borders. Cash-strapped businesses lowered purchasing activity resulting in survey-record declines of finished goods and input inventories.

“Business sentiment worsened to a considerable degree in April, with the largest fall seen across the investment goods category,” said IHS Markit Economics Director Tim Moore. “Manufacturers widely commented on concerns about the outlook for capital spending in the energy sector, as well as uncertainty about the length of customer closures and worries about a protracted downturn in global economic conditions.”

Mexico experienced its sharpest decline in business conditions in nine years. The April PMI fell to 35.0 from 47.9 in March as pandemic-related lockdowns and factory closures were imposed. Production and new orders plummeted and lead times lengthened sharply. Widespread supply-chain disruption was reported. Employment levels fell to record lows as demand weakened. “Looking forward, firms were immensely pessimistic towards the business outlook as a global economic recession looms and there remains little clarity over when this crisis might end,” commented IHS Markit Economist Eliot Kerr.

The IHS Markit U.S. Manufacturing PMI in April posted its lowest reading in 11 years at 36.1, down from 48.5 in March. Output declined at the steepest rate in the survey’s history as factories and businesses closed in response to COVID-19 health measures. New orders, domestic and abroad, plummeted and customers reported existing orders cancelled or postponed. The unemployment rate soared as more than 30 million Americans filed unemployment claims from mid-March through the end of April. Backlogs fell sharply and buying activity plunged as firms shed existing pre- and post-production inventory.

IHS Market’s Williamson said: “April saw the manufacturing sector struck hard by the COVID-19 pandemic, with output falling to an extent surpassing that seen even at the height of the global financial crisis. With orders collapsing at a rate not seen for over a decade, supply chains disrupted to a record degree and pessimism about the outlook hitting a new survey high, rising numbers of firms are culling payroll numbers.

“Consumer-facing businesses are being hit by slumping demand from households as April saw widespread lockdowns, but business spending on inputs and equipment has also tumbled as companies slash production and investment. Smaller firms are being hit the hardest, and also reporting the highest job losses, but large firms are also seeing the sharpest downturn on record.

“With infection curves showing signs of flattening, it is naturally hoped that the economic downturn will also bottom out. As restrictions are lifted, demand should gradually revive, but the tradeoff between risking a second wave of infections and bringing the economy back to life looks set to be one of the greatest challenges faced by policy- and lawmakers in recent history. The process will inevitably be led by caution, meaning recovery will also be frustratingly slow.”