Prices

May 26, 2020

CRU: Iron Ore Declines on “Two Sessions” Disappointment

Written by Erik Hedborg

By CRU Senior Analyst Erik Hedborg, from CRU’s Steelmaking Raw Materials Monitor

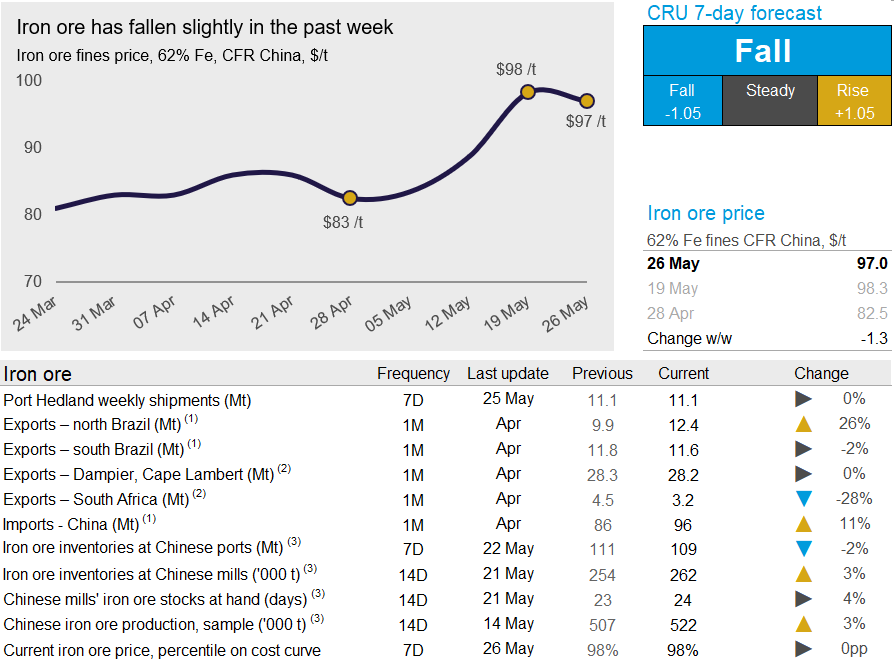

Iron ore prices contracted in the past week as China’s “Two Sessions” concluded with a disappointing outlook while Brazilian exports registered their strongest week of the year. On Tuesday, May 26, CRU assessed the 62% Fe fines price at $97.0, a $1.3 /t decrease w/w.

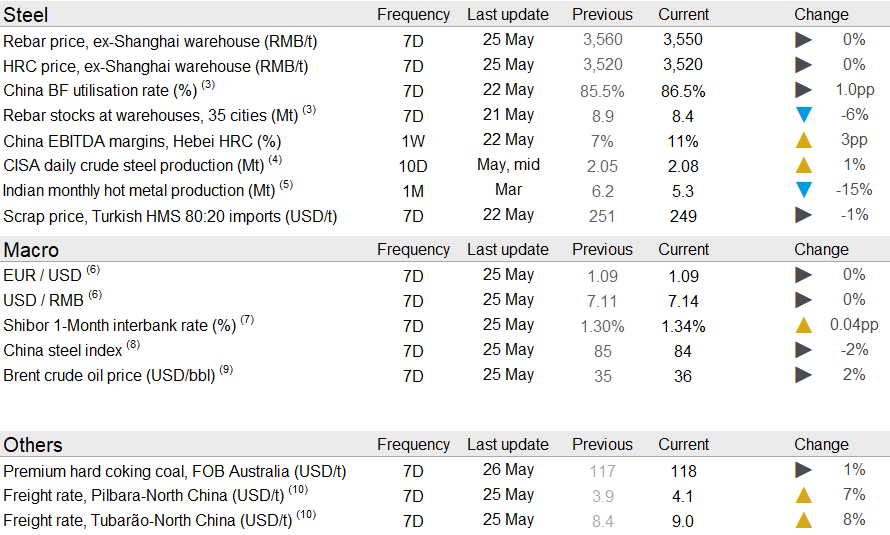

Chinese steel prices fell after the “Two Sessions” last week. No GDP growth target was announced and the sentiment in the steel market has shifted following the announcement. Although stimulus measures targeting infrastructure were announced, much of the spending will be investment in high-tech infrastructure that is less steel intensive. Other measures include an increase in quotas for government special bonds and reduced tax rates. Meanwhile, China’s steel mills continue to operate their BFs at elevated rates while steel inventories, although declining, remain elevated.

In the past week, Port Hedland continued to operate at high levels as the port shipped 11.1 Mt. However, Rio Tinto, which ships from the two ports Dampier and Cape Lambert, closed its ports due to the storm sweeping in over Western Australia and the company lost nearly 2 Mt of shipments as a result. Brazilian exports have also increased as shipments from both the northern parts of the country as well as Minas Gerais rose w/w. The Covid-19 outbreak in the northern parts of the country remains a concern for Vale, and shipments this year are below last year’s level despite S11D ramping up and still performing at a high level.

In Sweden, LKAB is still operating its Kiruna mine at reduced rates while the company carries out inspections in order to estimate the damage of last week’s earthquake. The company is currently operating at nearly half the capacity, but the full extent of the damages are not yet known. LKAB has in a statement mentioned that it has 0.5 Mt of inventory of iron ore at the mine and the company was about to enter a maintenance period, which would have reduced production anyway.

The sentiment in the Chinese steel industry has shifted in the past week and we expect the pessimism to persist. Arrivals to China will increase in the coming week due to recent strong Australian supply and a high chance that port inventories have reached their bottom. We maintain the view that we can see further price falls in the coming week.

Request more information about this topic.

Learn more about CRU’s services at www.crugroup.com