Prices

November 13, 2020

September Apparent Steel Supply Steady at 7.2 Million Tons

Written by Brett Linton

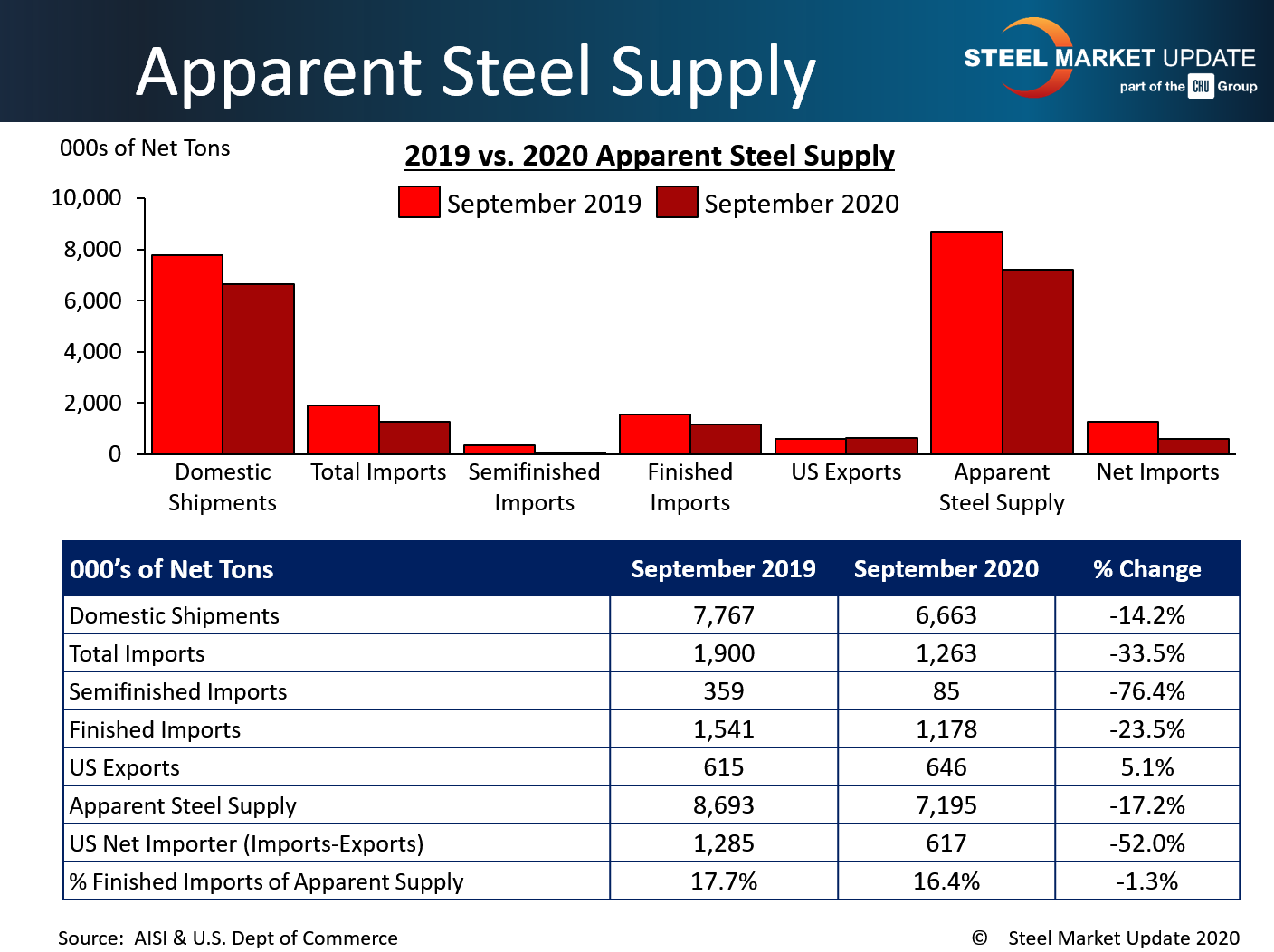

U.S. apparent steel supply remained flat from August to September, up 0.4 percent to 7.19 million net tons, according to the latest U.S. Department of Commerce and American Iron and Steel Institute data. While supply levels have improved each month since May, recall that April and May were the two lowest levels seen in the last 10 years at 6.54 million tons and 6.61 million tons, respectively. Apparent steel supply, a proxy for demand, is determined by combining domestic steel mill shipments and finished U.S. steel imports, then deducting total U.S. steel exports.

September apparent supply was down 1.50 million tons (17.2 percent) compared to the same month one year ago when supply was 8.69 million tons. This change was primarily due to a 1.10 million ton decline in domestic shipments, combined with a 360,000 ton decrease in finished imports and a 31,000 ton increase in total exports.

The net trade balance between U.S. steel imports and exports was a surplus of 620,000 tons imported in September, down 17.1 percent from the previous month, and down 52.0 percent from one year prior. Finished steel imports accounted for 16.4 percent of apparent steel supply in September, down from 16.6 percent in August and down from 17.7 percent one year ago.

Compared to the prior month when apparent steel supply was 7.17 million tons, September supply rose 26,000 tons or 0.4 percent. This change was due to a 130,000 ton increase in domestic shipments, mostly negated by a 95,000 ton increase in total exports and a 10,000 ton decline in finished imports.

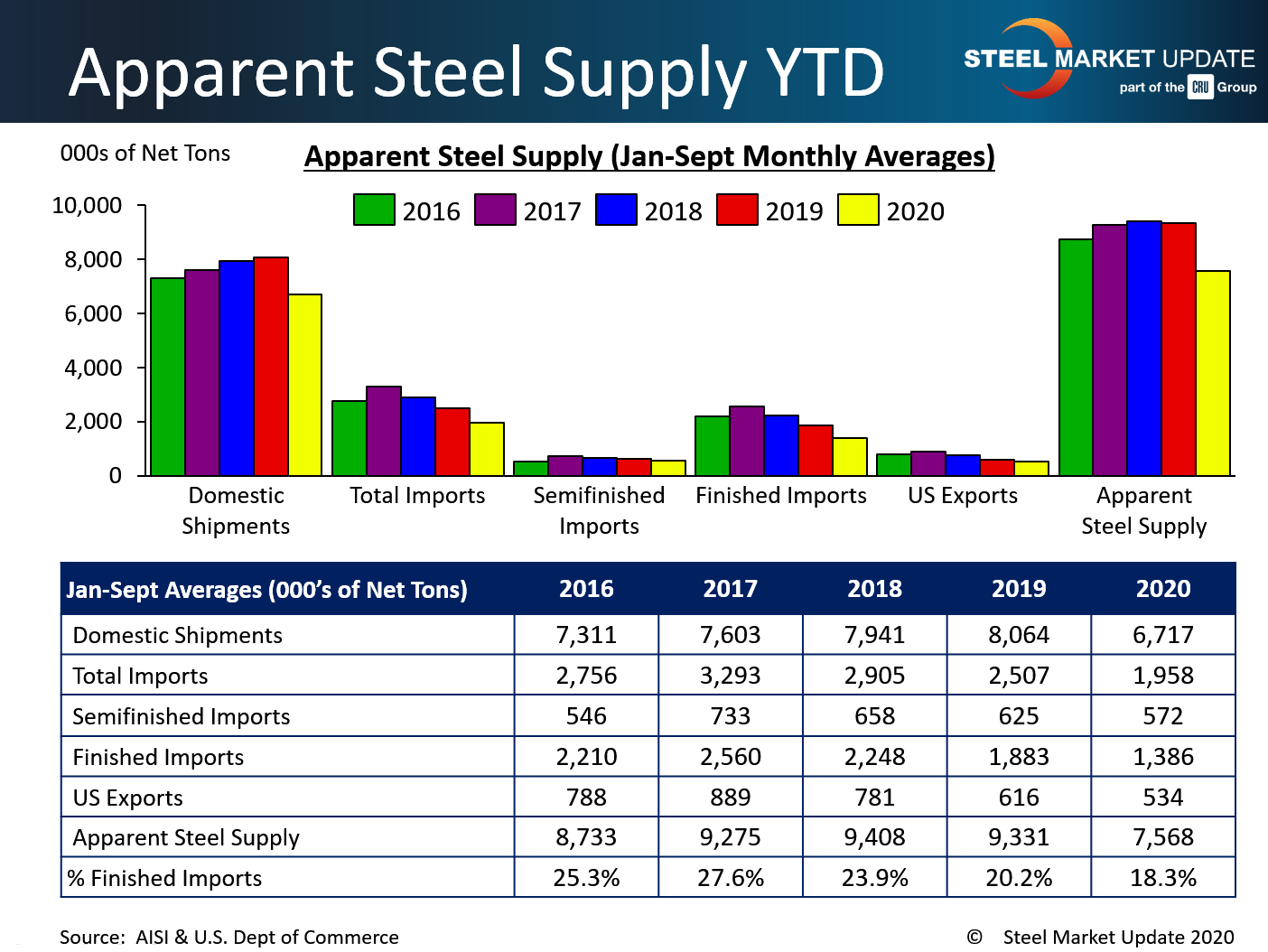

The figure below shows year-to-date averages for each statistic over the last five years. As has been the case for the last few months, 2020 apparent supply remains significantly lower compared to the first nine months of all previous years shown.

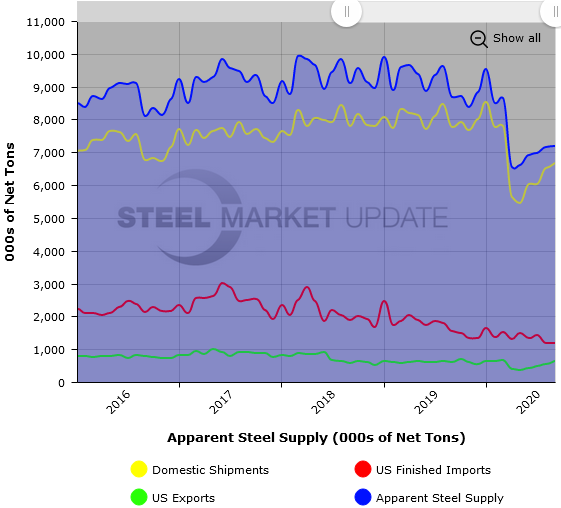

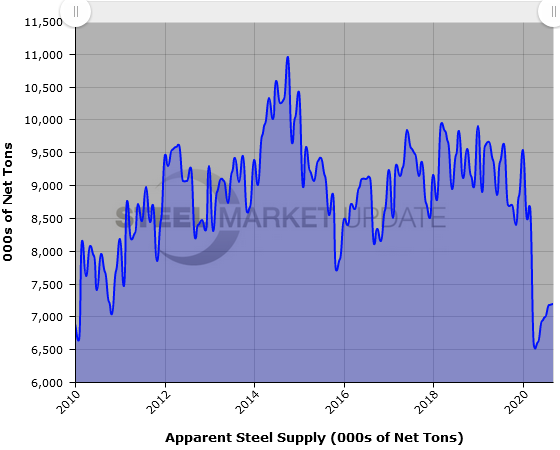

To see an interactive graphic of our Apparent Steel Supply history (example shown below), visit the Apparent Steel Supply page in the Analysis section of the SMU website. If you need any assistance logging into or navigating the website, contact us at info@SteelMarketUpdate.com or 800-432-3475.