CRU

March 16, 2021

CRU: Iron Ore Rising on Weak Australian Supply

Written by Erik Hedborg

By CRU Principal Analyst Erik Hedborg, from CRU’s Steelmaking Raw Materials Monitor

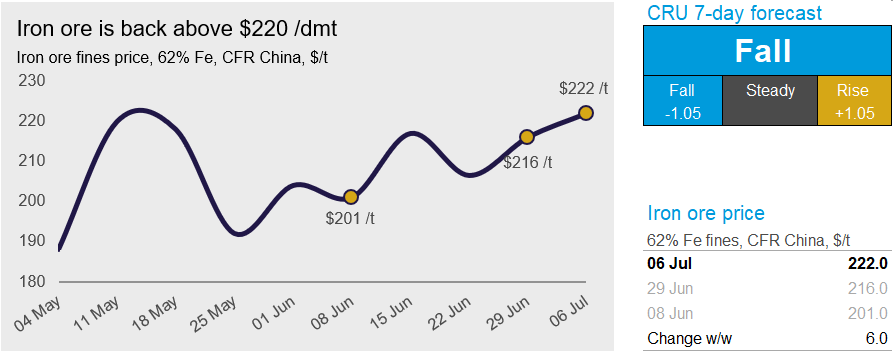

Iron ore prices have continued to rise in the past week as a result of a combination of weaker seaborne supply and rising steel prices following the recent celebrations in China. On Tuesday, July 6, CRU assessed the 62% Fe fines price at $222.0 /dmt, up by $6.0 dmt w/w.

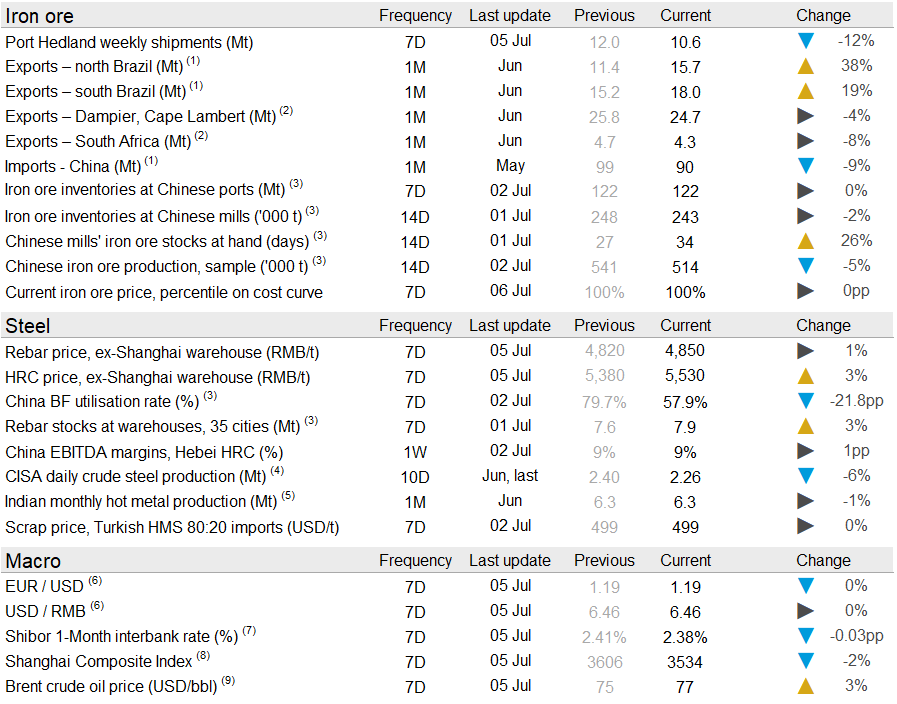

Last week, Chinese domestic steel prices were largely stable due to slower business activity prior to the celebration of the 100th year anniversary of the Chinese Communist Party (CCP) on July 1. To reduce pollution and the risk of accidents, many steelmakers slowed their operations, resulting in lower steel production, but steel inventories continued to rise as underlying demand fell faster. Having said that, on Monday, physical steel prices lifted after futures prices rose due to speculation on government-led production cuts later this year, but transactions were heard thin at higher prices. As many BFs were hot-idled prior to the government’s event, hot metal production dropped, leading to lower iron ore consumption. Iron ore onshore inventories (e.g. at mills and ports) did not rise because port operations also slowed, resulting in a longer vessel queue.

Seaborne supply in June disappointed the market with Rio Tinto and BHP now falling 4% behind last year’s exports for the first six months of the year. For Rio Tinto, the maintenance at Dampier is now completed and exports from the East Intercourse Island berths have resumed, but the production issues in parts of the Pilbara remain, which means lower exports and higher volumes of low-grade material will sustain for some time. Rio Tinto’s June shipments are estimated at 24.7 Mt, lower than in May (25.8 Mt) and June last year (28.6 Mt). CRU estimates that exports from Port Hedland reached just above 50 Mt in June, lower than last year’s record exports of 51.8 Mt.

On a positive note, Brazilian exports recorded a strong month with exports reaching 33.7 Mt in June, up nearly 4 Mt y/y and a big jump from May (26.5 Mt). Our analysis of the trade data shows a strong performance from the Northern Ranges in Vale’s Northern System, high levels of low-grade exports from Brucutu and an increase in pellet feed supply from Vale’s Itabira Complex. Samarco had a good month with 0.9 Mt of exports during the month, mostly DR pellet. This brings the company’s production rate above its nominal capacity of 8 Mt/y.

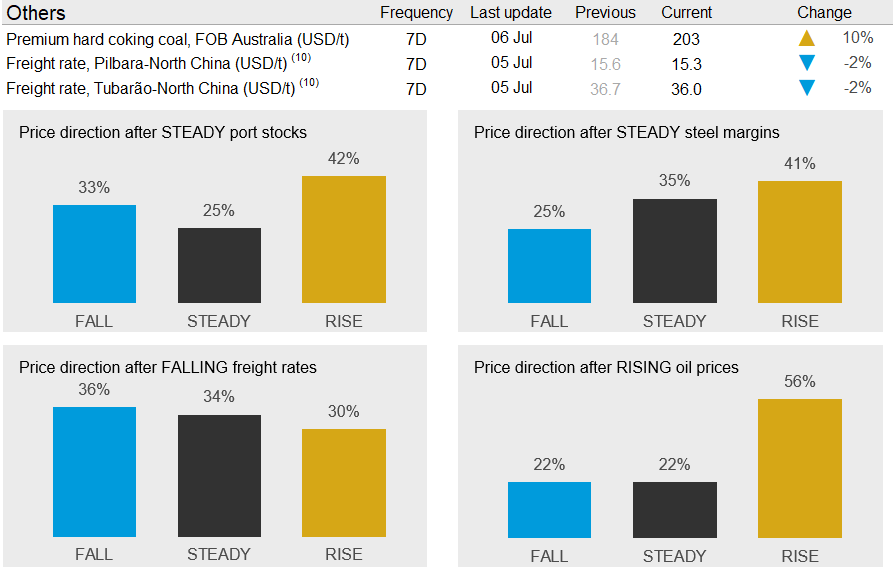

In the next week, we expect iron ore prices to soften. Steel margins in China are still thin and arrivals to China remain high while the vessel queue has grown, meaning there is no shortage of iron ore outside Chinese ports at the moment. Our indicators below point towards a rise, and there is plenty of uncertainty in the market with many rumors circulating in China about the government’s next interventions in the steel market.

Request more information about this topic.

Learn more about CRU’s services at www.crugroup.com