CRU

October 15, 2021

CRU: Downward Pressure Eases on Global Metallics Prices

Written by Ryan McKinley

By CRU Senior Analyst Ryan McKinley from CRU’s Steel Metallics Monitor

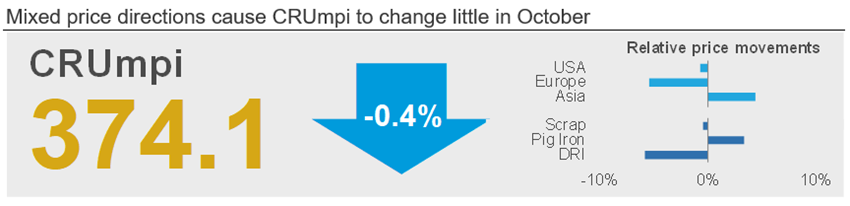

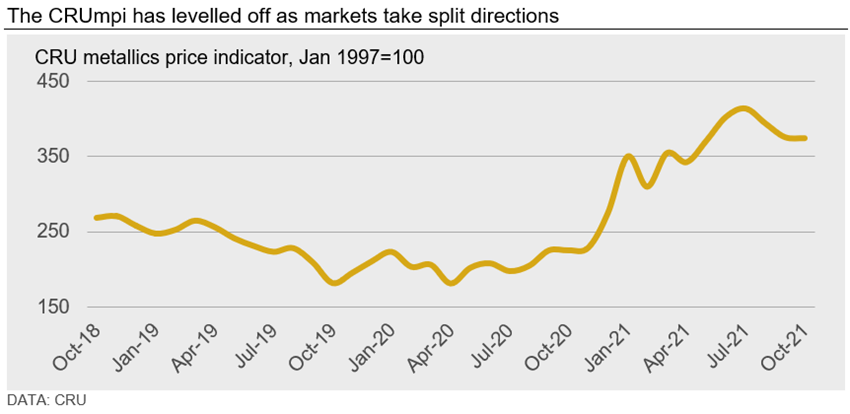

The CRU metallics price indicator (CRUmpi) changed little in October, declining slightly by 0.4% to 374.1. Price directions were mixed but fell by the most for European scrap and DRI while scrap prices in Asia had the largest increases. We expect to see similar market behavior next month, and the CRUmpi will likely stick around its current level.

Demand for metallics around the world was generally stable m/m in October. Scrap traded lower in areas like Europe and Russia, although rising imported prices into Turkey prevented substantial declines. In North America, price trajectories were split between obsolete and prime grades, with the former stable or rising m/m while either stable or falling for the latter. Further south, Brazilian mills managed to push prices lower again m/m, but margins for scrap processors are eroding quickly. Perhaps the most surprising, albeit small, price increase occurred in China, where severe energy shortages have greatly limited steel output—especially at EAFs. Nevertheless, scrap collection was also impacted and offset lower demand. Scrap prices in other areas of Asia also increased on easing Covid-19 restrictions. For pig iron, price movements were unusual in that they fell in exporting nations but rose in importing ones due to high freight costs.

In Europe, scrap supply largely outpaced demand, especially for obsolete grades. Well-stocked mills and seasonally strong collection allowed prices to fall notably for a second month, especially given that long product prices will likely face seasonal pressure as winter approaches and hampers construction activity. Still, Turkish demand for scrap strengthened in the first week of October as long product exporters there found opportunities abroad, and this helped prevent larger scrap price falls in Europe. However, Russian exporters were unable to capitalize on the upward momentum in Turkey due to the export tariffs on scrap. With little material leaving the country, mills had access to plenty of material at lower prices.

In the USA, trade patterns were atypical after one integrated mill announced it would leave prime grade prices unchanged m/m ahead of the usual announcements from EAFs. While dealers sold at unchanged levels to some mills, other mills secured price decreases of $10–20 /l.ton. Obsolete grades were either stable or traded higher m/m due to somewhat crimped supply, transport issues, and because consumers anticipate further price hikes in the coming months.

Mills in Brazil successfully pushed prices lower once again, but consecutive m/m domestic price falls have now caused exports to reach their highest level in over a year. While mills are looking to control input costs as finished steel prices fall, scrap sellers are signaling that their margins are becoming untenable and that this may harshly impact supply in the near future.

Chinese scrap prices were remarkably resilient in October after significant energy shortages caused the government to strongly cut steel output and, by extension, scrap demand. However, power usage controls also impacted scrap collection and processing activity, and after market participants returned from holidays on 7 October, mills were forced to increase bid prices. In other parts of Asia, the easing of Covid-19 restrictions bolstered both finished steel and scrap demand, increasing prices for both.

The pig iron market gave seemingly mixed price signals, with prices falling slightly in exporting nations while rising in importing ones. While Brazilian export prices fell by $10 /t m/m, import prices in the USA moved slightly higher by $5 /t. A more notable disparity occurred in Europe, where Italian import prices rose by $30 /t, but export CIS prices dropped. Both occurrences are attributable to surging freight rates, especially in the Mediterranean Sea area where freight costs now exceed $55 /t, according to market participants.

Outlook: Price Direction to Vary by Region in November

We expect to see some volatility in metallics prices moving into November depending on type, grade, and region. In the USA, market sentiment is growing increasingly bullish as mill outages end and obsolete scrap supply remains lower than in prior months. The outlook is similar in Asia (outside of China), where easing Covid-19 restrictions will boost scrap demand.

Conversely, European price direction will be contingent on soaring energy costs that threaten to disrupt domestic steel production, while demand from Turkey will also likely weaken. Similarly, Chinese scrap prices will be at the mercy of government-led production cuts and energy deficits.

In total, we expect to again see a mixed bag in terms of pricing across the globe in November, with the CRUmpi settling somewhere around where it is now.

Request more information about this topic.

Learn more about CRU’s services at www.crugroup.com