Market Data

March 3, 2022

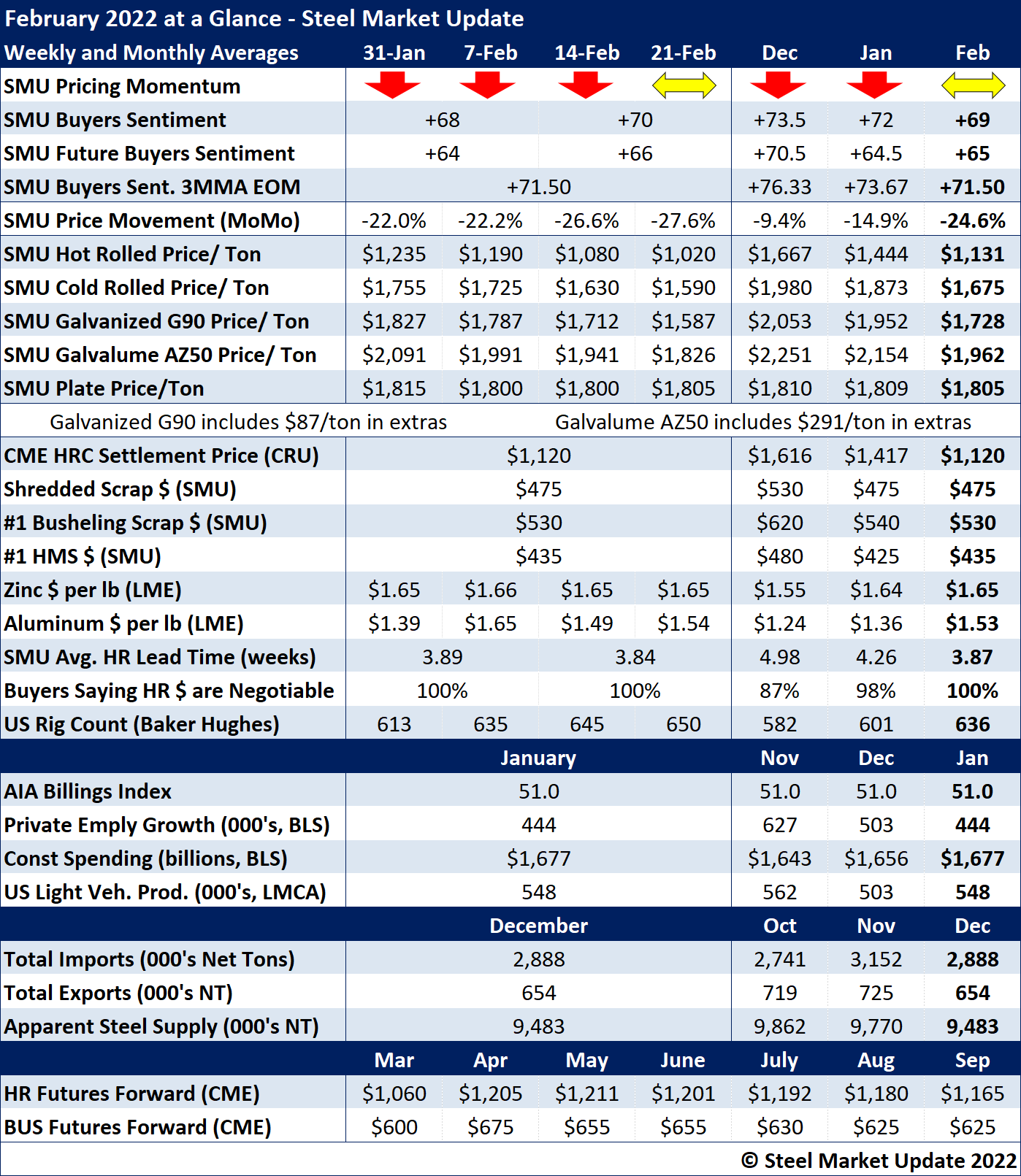

SMU's February at a Glance

Written by Brett Linton

February marked month six of declining steel prices, following a 12-month streak of continuous price increases. Hot rolled prices declined $215 per ton throughout the month, with the SMU index averaging $1,020 per ton at the end of February (recall our HR average this week declined another $20 to $1,000 per ton). The SMU Price Momentum Indicator for sheet products was adjusted to Neutral in the fourth week of February, which had previously been pointing Lower since mid-October. Plate price momentum remains at Neutral, as has been the case since Septemer last year.

February scrap prices were relatively stable, within $10 per ton of January prices. Click here to view and compare prices using our interactive pricing tool.

Zinc spot prices remained elevated yet stable in February, while aluminum prices climbed higher throughout the month. As of Feb. 28, the Kitco spot price for zinc was $1.67 per pound and aluminum was $1.58 per pound. As of the time of this writing, both zinc and aluminum prices have risen further, with zinc jumping to $1.77 per pound and aluminum up to $1.64 as of March 2.

The SMU Buyers Sentiment Index remained at a high level of optimism, ranging from +68 to +70 during the month. Viewed as a three-month moving average, buyers’ sentiment declined slightly to +71.50 in late-February. Future sentiment readings remain optimistic, as they have been for over a year and a half.

Hot-rolled coil lead times have remained steady for the past six weeks, currently at 3.84 weeks as of late-February (territory last seen in the summer of 2020). The percentage of buyers reporting that mills are willing to negotiate on hot-rolled coil prices has been rising for the past six months, with both February datapoints indicating mills are willing to talk price to secure an order. A history of HRC lead times can been seen within our interactive pricing tool.

Key indicators of steel demand remain positive; the AIA Billings Index indicated that construction activity has recovered for over a year now. The energy sector continues to improve, as do total U.S. steel imports, exports and apparent steel supply.

See the chart below for other key metrics in the month of February:

By Brett Linton, Brett@SteelMarketUpdate.com